The 5 Business Models of Vertical Software

A Framework for Evaluating vSaaS Value Creation

In the 20 years since the coining of the term Software-as-a-Service, the market for cloud software has grown at a brisk 25% CAGR,1 exploding to a revenue base of hundreds of billions since then. That spend represents the reallocation of corporate budgets from legacy technology, headcount, and services to new SaaS solutions. In other words, it is not just that the demand for software is growing; software is streamlining net-new work streams year by year, often cannibalizing traditionally non-tech market share.

It makes sense, then, that each subsequent wave of breakout cloud software startups have been progressively more specialized. Whereas Salesforce—the original SaaS standard-bearer—was considered a focused software solution when CRM was new, it now has more in common with the monolithic horizontal suites it competes with (e.g., Microsoft, Oracle, SAP) than the increasingly vertical SaaS winners of the last five years (e.g. Procore, Shopify, Toast). As enterprises looked to cloud software to solve new problems, startup infrastructure costs continued to fall, and venture capital proliferated, every sub-vertical of the economy over $10B in revenue became capable of supporting an IPO-able startup.

The corollary of the growth of SaaS, in other words, has been the rise of vertical software. Those industries of the economy with a head start in technology spending and talent—namely, financial services, media, and technology—were the first to shift spend to the cloud and next-generation solutions. Accordingly, software catering to those spaces has seen the highest proliferation of winning exits and venture funding over the last two decades. But that was only the beginning. We believe it is inevitable that every sector of the economy will be powered by its own constellation of at-scale vertical software solutions, each purpose-built to service its unique stakeholders and workflows.

A massive and under-appreciated driver of that secular trend is business model expansion. More specifically, a significant innovation in driving adoption, increasing market share, and producing winners has been an emerging class of vertical software companies that have moved beyond traditional SaaS pricing paradigms, attaching themselves to discrete industry-specific value streams and business outcomes. The significant net result of this shift is an overnight order of magnitude increase in market size for vertical startups and potential venture-scale outcomes. Consider this simple framework: in many traditional industries, technology spending has often plateaued between 2- 5% of overall industry revenues.

Tech Spending by Industry (% of Revenue)2

At the lower end of this spectrum, an industry would need >$75B of gross revenue to reach a potential $1B software TAM. It also strongly limits the number of potential winners in low-spend categories. However, business model expansion has enabled new vertical startups to capture value from the 95% of non-tech spending, including sales & marketing, materials, freight, payment processing, labor, recruiting, training, insurance, banking, and many others. We will be doing a deeper dive in a future post on the implications for market evaluation. Today, we wanted to share our perspective on this shift and how it influences the framework we use to map Vertical Software businesses.

The Archetypes of Vertical SaaS Business Models

Above, we described the scale of opportunity in vertical SaaS startups is undergoing constant growth as software enables them to capture an increasing share of legacy spend—not just from technology budgets, but also from spend traditionally dedicate to personnel and services.

The fastest paths to value growth, however, vary widely based on industry stakeholders, budgets, and norms. The business model a business is using to enter a market can be a helpful way of understanding its future path. Today we wanted to share the basic framework Euclid uses for vSaaS business model evaluation.

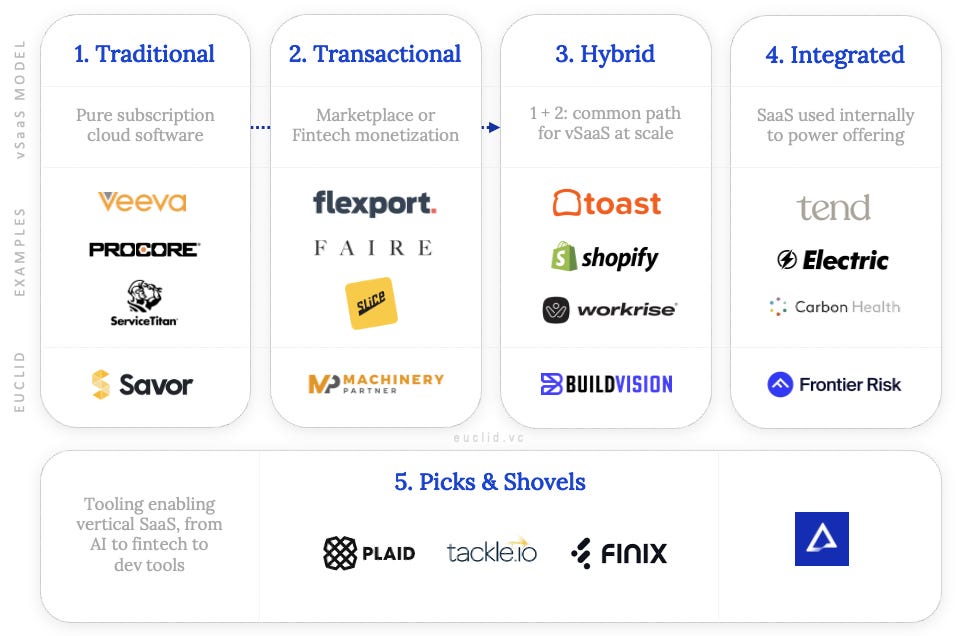

Our paradigm splits the vertical SaaS universe into five core business models—these are best viewed as a spectrum rather than as mutually exclusive groups, and a company can (and often does) shift between them over time.

Traditional SaaS: Classic subscription software business models (e.g. Veeva or Procore).

Transactional: Industry-specific payments, lending, procurement, and/or marketplace businesses monetizing on a non-subscription model (e.g., Faire or Flexport)

Hybrid: Combination of 1 and 2 (e.g., Toast or Shopify) where businesses charge both subscription and transaction fees. At scale, the majority of vertical platforms hybridize in some form.

Vertically Integrated: The startup is the sole “customer” of the vertical software. It aims to win market share through differentiated service powered by proprietary technology, giving it a competitive edge in value, speed, scope, etc. (e.g., Tend or Electric).

Picks & Shovels: Infrastructure powering vertical software. This can be industry-specific (e.g., Plaid for financial services) or embedded software tailored for vertical platforms (e.g., Finix).

At Euclid, we invest across all these archetypes—there is no one-size-fits-all approach. Only the right model for the right team, time, and vertical. In general, our belief is that right approach is the one that can drive adoption quickly and reach product-market fit in a capital-efficient manner. For application-layer businesses, that most often lends itself to SaaS or Transaction-Based models that hybridize into multiple revenue streams with scale. In a future essay on market evaluation, we’ll unpack this in more detail.

While we have and will continue to invest in vertically Integrated businesses, we are highly sensitive to capital-intensive business models. M&A roll-up strategies have emerged in this area (some with novel financing strategies that separate operating companies’ balance sheets). We’ve even seen SaaS / hybrid companies vertically integrate and vice versa. Given our capital limitations as a pre-seed fund—and the desire to invest in capital-efficient companies—we tend to be cautious in evaluating such opportunities. While proprietary software can unlock massive advantages, if the company still faces low margins, high CAC, or multiple compression at the end of the day, a venture-scale outcome may be wishful thinking.

We do hypothesize that the proliferation of roll-up strategies in lower- & mid-markets will lead to a strong season for SaaS / Hybrid plays, as management gains budget and sophistication. Increased competition from PE-backed consolidators, in contrast, could present major headwinds for Integrated vSaaS startups. As with all hypotheses, we’ll continue to evaluate those assumptions over the coming months and years.

As always, we’d love to hear from you on our framework! Shoot us a note or reply in the comments.

Sources

Deloitte (2021). SaaS Industry Outlook: Time to Ride the Wave.

Gartner (2023). IT Key Metrics Data 2023: Industry Measures.

Deloitte report above.

Gartner report above.