Clear Eyes, Full Stack, Can’t Lose?

When Vertical AI founders should own a layer, access it, or commoditize it

After a decade in which venture-backed companies were rewarded for asset-light models, vertical integration is back in vogue.

The argument is as follows: AI is commoditizing an increasing portion of software, leaving proprietary data, context, real-world feedback, trust, and distribution as the remaining scarce assets. As a result, vertical startups are incentivized to own the entire value chain. This ambition now extends beyond traditional technology and business services to include AI-enabled home services, construction firms, senior living, and even hospital systems.

NFX concisely summarizes this view in “The AI Wrapper Is Dead”:

The wrapper generation is dead. The survivors and the next generation of startups will think vertically. ‘How do I own every piece of the value chain?’

No doubt, thin wrappers are vulnerable. However, “own every piece” feels like an oversimplification that describes several very different strategies. A company might expand to multi-product, own physical assets, combine hardware and software, operate as a service provider, or vertically integrate into another part of the market. These are radically different strategies with radically different economics.

Our view is that AI expands the feasible boundary of venture-backed startups without determining the optimal one. AI companies should focus on capturing segments of the value chain where data, workflow position, and high-value outcomes accumulate. Sometimes that requires vertical integration, but it often does not.

The form of vertical integration, moreover, matters as much as the extent of it. A company may own the entire stack yet still gather undifferentiated data, depend on the same models as everyone else, and operate with higher friction and worse economics than focused competitors.

Integration maximalism ignores a long history of dominant vertical application-layer platforms that achieved powerful scale and defensibility without expanding into every possible industry revenue stream. Even in the current era of AI, businesses will thrive — and may even be better off — by focusing on controlling the specific portion of work-to-be-done where learning can accumulate.

In Vertical AI, as with SaaS before it, the objective is simple: own the control point. Naturally, control points are industry-dependent and shift over time as technology differentiates some layers and commoditizes others. But the full-integrationist narrative suggests that LLMs have turned every vertical surface into a control point. This is its fatal flaw. In any B2B landscape, there are always a limited number of consequential loci in the customer’s workflow that can serve as the launching point for systems of records.1

Clay Christensen’s Other Theory

Clay Christensen is best known for The Innovator’s Dilemma. He had another, less famous theory of vertical integration and modularity. Christensen first described it in “Disruption, Disintegration, and the Dissipation of Differentiability.” In a 2006 interview with Bloomberg, he summarized the argument this way:

During the early stages of an industry, when the functionality and reliability of a product isn’t yet adequate to meet customer’s needs, a proprietary solution is almost always the right solution — because it allows you to knit all the pieces together in an optimized way.

But once the technology matures and becomes good enough, industry standards emerge. That leads to the standardization of interfaces, which lets companies specialize on pieces of the overall system, and the product becomes modular. At that point, the competitive advantage of the early leader dissipates, and the ability to make money migrates to whoever controls the performance-defining subsystem.

Put another way, when a market is young, it is by nature experimental:

Buyers are figuring out whether they should buy, build, or wait

Sellers are fragmented and inconsistent, without baked-in economies of scale

In this phase, assuming buyers determine there is value in the new technology, more proprietary approaches look attractive. From the buyer's perspective: given that the current sellers are small and expensive, perhaps we should just control our destiny and grab value ownership in this hot new space. It follows that vertical integration is more interesting for sellers — get consultative, solve the whole problem, own more. In this moment, technology buddies becoming operating businesses even makes sense. Why shouldn’t sellers become what buyers were, owning the fruits of their in-house tech.

As the category matures and standards emerge, however, modular offerings improve. Customers become less willing to pay extra for the integrated solution and begin to value interoperability. At that point, the early integrator is exposed. Low-cost providers assemble products from components, undercutting the integrator’s stack on specialization and price. Open source solutions emerge. And tech businesses who became operating businesses can no longer maintain internal technology autarky — if they want the best tech, they need to become tech buyers themselves. In Christensen’s theory, the long-term market profits are not captured by the integrator, but by whomever owns the “performance-defining subsystem.”

AI makes this theory newly relevant by expanding what a startup can plausibly do in-house. More of the stack can be automated, bundled, or absorbed. That makes integration more tempting, but it does not change where profits ultimately migrate.

In A Guide to Disrupting Incumbents, we shared how this applies to startups disrupting incumbents by commoditizing complements, undercutting pricing power, and using the surplus they create to earn distribution and trust. In that piece, we discussed the canonical example of commoditization with Microsoft and the PC market:

In the early 1980s, software wasn’t even considered a market separate from hardware. When PCs started taking off, IBM was so eager to be a first-mover that it launched its 5150 model with an open architecture: using off-the-shelf hardware, publishing the technical specs, and encouraging expansion cards.3 The PC landscape, including IBM and its fast-followers, would quickly descend into a knife fight, kicking off a race to the bottom on pricing. Meanwhile, Microsoft’s DOS—offering the preferred4 OS, a critical complement to PCs—skyrocketed.

Integration can win early and still lose the market later. The graveyards of once-prominent technology stalwarts bear this out. Vertical integration may be structurally necessary or serve as a temporary bridge to market entry before ecosystem maturation. It might also be a company-killing error. Commoditization will eventually affect the integrator’s stack. Vertical AI founders should focus on owning components with lasting defensibility and profit potential.

NVIDIA is the modern counterexample to integration maximalism. The company tightly integrated GPU architecture, CUDA, networking, and the software ecosystem around accelerated compute. But NVIDIA left semiconductor fabrication to companies such as TSMC. It was integrated, with co-design strengthening its control point and enabling access to the capital-intensive layer, where a specialist had better economics. That position helped make NVIDIA one of the most valuable companies in the world.

The Minimum Sufficient Stack

Integration creates a durable advantage only when it secures something scarce. The argument for capturing more of the value chain centers on defensibility. For example: a product that senses the world, captures first-party data, influences an action, observes the result, and improves. If the company owns the entire loop, competitors cannot access the same context.

However, vertical integration does not guarantee defensibility. A company may own the full stack yet still collect only commodity data. Long-term value depends on the quality and structure of the signal, which must be proprietary, dense, and difficult to replicate. A vertically integrated startup may own sensors that produce undifferentiated data. In such cases, integration increases capital and operational burdens without enhancing defensibility or long-term prospects. The company is committed to eventually competiting with startups taking advantage of falling input costs to undercut. Having made the argument for the necessity of integration, management is often forced to wage a losing battle that saps the strength of its core product.

The traditional lesson from vertical software remains relevant. Leading vertical software companies seldom win by capturing the entire value chain — they win by capturing the workflow control point. And the concept of “owning everything” extends as readily across operating lines as it does technological ones. Toast owns the POS and transaction layer, not the restaurant. Veeva owns critical commercial and regulatory workflows in life sciences, not the drugmaker.

The strength of these platforms lies in their ability to understand and monetize the workflow without inheriting the industry’s full cost structure. Vertical AI raises the bar because software can now do more of the work directly. But the strategic question is the same:

Where does the system need control to compound learning?

Durable AI-native companies succeed by building towards securing control points. In our earlier work on successful Vertical AI playbooks, we recommended that many AI-native companies should begin with an authoring layer — a starting point for a valuable internal workflow that generates revenue and immediate ROI. This was a product strategy argument.

Our view on vertical integration builds on that: at the earliest stage, Vertical startups need to own the minimum sufficient stack to capture the control point: the part of the workflow where that loop compounds.

There are many ways a company can secure a control point, dependent on industry and state of technology: workflow embedding, licensing, integrations, contractual rights, proprietary hardware, and more. What matters is capturing dense and repeatable signals. The rule is simple:

Own an asset only when ownership unlocks access to the control point. Everything else is expensive friction.

Previously, the key question was whether to build or buy. For Vertical AI, the strategic question is own versus access: which parts require direct control, and where is reliable access sufficient?

The shift from on-premise software to SaaS has already demonstrated this lesson. Most SaaS companies rent compute and storage. A SaaS product that offered no unique value beyond generic infrastructure was vulnerable, but the answer was not to buy a data center. The answer was to capture the layer with data and workflow gravity and ultimately outsource the rest to cloud infrastructure providers.

Vertical integration, in itself, confers no specific market advantage. Sensors, models, integrations, services, and hardware matter when they enable access to the control point. Past that basic threshold, the risk is that ownership adds friction without durability.

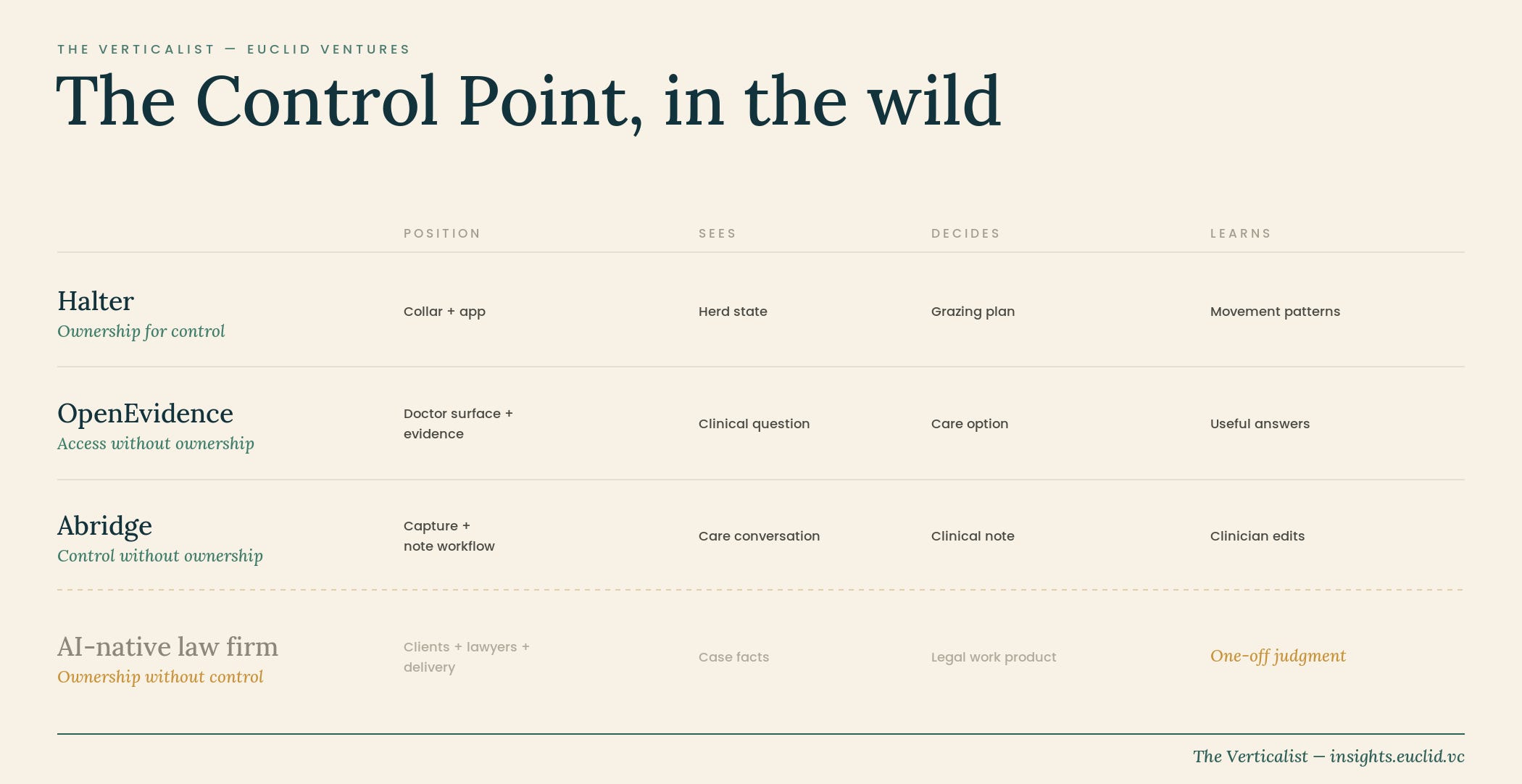

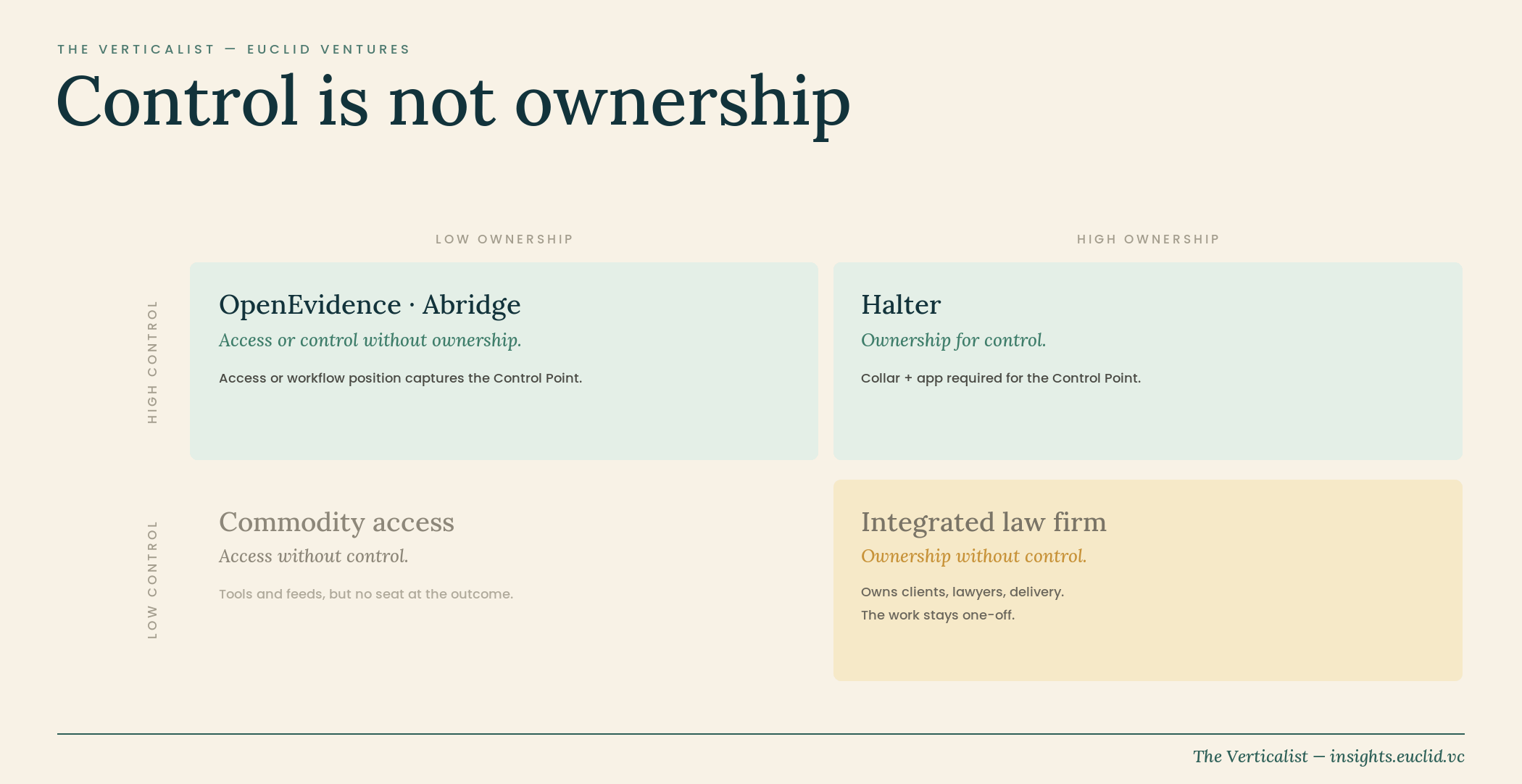

Control Points in the Wild

There are three independent variables to describe the components of vertical integration. Access means you can use an asset without owning it. Ownership means the asset belongs to your company. Control means the control point itself.

Four examples show how they combine in practice:

OpenEvidence: access without ownership

OpenEvidence sees the clinical question at the point of care, retrieves the relevant evidence, and presents an answer to the physician.

Commercial agreements with medical journal publishers secured access to licensed content. The control point is the clinical question at the point of care. It does not need to own the journals, the hospital, or the physician workflow end-to-end. It needs trusted access to evidence and repeated presence at the clinical question.

Its defensibility, therefore, depends on the durability of its content access, physician distribution, trust, and the value of aggregated demand, not yet on a fully closed clinical learning loop. In this case, licensed access, without ownership, may be sufficient for long-term durability — because ultimately it isn’t necessarily the content that provides differentiation. It is their superior understanding of physicians’ questions and answers in situ, and the resulting ability to provide the best physician experience.

Halter: ownership for control

Halter captures cattle data, directs movement through virtual fencing, and gives the rancher an application for managing their herd.

The collar is required because it provides access to the control point. Without the hardware, Halter would not have access to the signal, action, or outcome.

However, the hardware itself is not the moat. It is mission-critical today because it secures the observation-and-action loop and the rancher workflow where learning compounds. Over time, modular hardware components should be allowed to commoditize, provided this expands access to first-party data without weakening control point ownership.

Abridge: control without ownership

Abridge captures the clinical conversation, creates documentation, and connects the note to downstream charting, coding, and revenue workflows.

While the sensor is the microphone, Abridge’s control point is the authoring layer: the clinical note starts in their software, flows into the health system through deep integrations, and serves as the base layer for critical downstream work. That position captures clinician edits, approvals, coding changes, and revenue outcomes.

Abridge’s learning loop does not require any additional parts of the healthcare value chain beyond their control point and its downstream workflows. Even as clinical notetaking commoditizes, what compounds is that downstream position, not the transcription itself. In the medical scribe world, the question remains whether the underlying technology supports long-term defensibility of this control point, especially in the face of highly dominant and motivated incumbents — but the control point that matters remains clear.

The AI-Native Law Firm: ownership without control

Now consider a fully integrated AI-Native law firm: client relationships, lawyers, and delivery all in-house.

While owning the entire value chain may appear defensible, in practice, it often results in collecting undifferentiated data that is easily accessible to frontier model companies, traditional law firms using tools like Harvey, and other AI-Native law firms. We discussed this dynamic in our essay on AI-Native services:

Model improvements only make a service defensible to the extent that no competing service adopts the same LLM advances. That’s not a bet we’d take.

The strongest moats in software have always been those that are not easily replicated — proprietary data loops, workflow integration, distribution, network effects — not the infrastructure they’re built on, regardless of whether you charge for the tool or the output.

When Integration Is Actually Necessary

While cautioning against the reflexive urge to own the entire value chain, vertical integration can often be structurally necessary to win a market.

Integration can secure supply, reduce latency, improve quality control, establish a single accountable operator, or prevent a critical supplier from capturing product economics. These are real advantages, but they are mechanisms rather than moats.

Integration is most defensible when one of three conditions holds.

1. The category is not stable enough for modularity

If the handoffs between the model, workflow, hardware, and surrounding environment change constantly, separate vendors may not be able to coordinate fast enough.

In these markets, integration is necessary for rapid iteration. However, this supports integrating across unstable interfaces, not owning every adjacent business.

2. Performance is below the buyer’s threshold

A multi-vendor system may be too immature or brittle, and the buyer may opt for a single party to guarantee reliability. Integration may be necessary to establish trust. RLHF (Reinforcement Learning from Human Feedback) vendors likely fall into this category.

Even in these cases, companies should distinguish between layers required for current deployments and those likely to be defensible profit centers in the future.

3. Durable access cannot be secured without ownership

A supplier may refuse to provide the data. The sensor, literal or figurative, may not exist. A software vendor may make integrations nearly impossible or severely restrict the actions a product can take.

If the only reliable way to secure access is to own the relevant asset, ownership may be required.

These conditions are real but more limited than the integrationist narrative suggests. They also evolve rapidly, especially in the LLM era. Markets mature quickly, fierce competition drives interoperability, and buyers are quickly becoming more attuned to their needs. Modular entrants will inevitably target individual layers of the integrator’s stack, often after the integrator has established the category.

Modular competitors do not always win. But the advantage created by ownership is often time-limited unless the integrator continues to own the performance bottleneck, the control point, or both.

We are in a classic Christensen’s Young Market moment today. Buyers are struggling with understanding what to buy or build — and what is even worth adopting in the first place. To that end, it can make sense to be more experimental, to be more consultative, and to take on more than you otherwise might have to solve enterprise problems. And the reward may indeed be owning more than a traditional wedge, faster.

We believe, however, the prescription for Vertical AI founders is not to blindly commit to owning everything from the get-go. Toeing this line requires strong management discipline and taste, but the ones who do it well — testing everything while retaining focus — will benefit greatly. There are a number of strategies founders can use to maintain balance, manage a wider footprint, and test expansion.

Commoditize Complements, Don’t Adopt Their Economics

In A Guide to Disrupting Incumbents, we wrote about eating complements and nuking pricing power. A startup can weaken incumbents by making adjacent products cheaper, free, embedded, or otherwise less able to capture margin.

But commoditizing a complement does not require ownership, nor does it require adopting its economics or business model. Often, the better strategy is to make the complement abundant, standardized, and cheap so that value shifts back to the layer you control.

Startups can undercut on price or promote interoperability standards. The objective is to remove the bottleneck without permanently inheriting the complement’s cost structure.

If a healthcare AI company identifies services as the bottleneck, it may initially require human intervention. However, the goal should be to convert repeated service work into access to a control point, rather than simply becoming a lower-cost services provider.

The primary advantage of software is leverage. AI changes the boundaries of what startups can do, but it does not negate the attractiveness of software and asset-light business models. If anything, leverage matters more as baseline intelligence gets cheaper. Fast followers, perhaps even the frontier models themselves, will modularize your offerings.

Before founders ask what part of the stack they should own, they should ask a more important question:

What are we trying to commoditize?

If a complement hinders adoption, integrate only enough to reduce its pricing power, coordination costs, or reliability risks. If a layer does not strengthen the control point, consider renting, licensing, or exposing it through a modular interface.

Commoditize complements, but avoid adopting their cost structures. The specialization of function and labor is as close to a fundamental economic truth as we have — great founders pick their battles against this principle wisely, and recognize they are unlikely to win a protracted war.

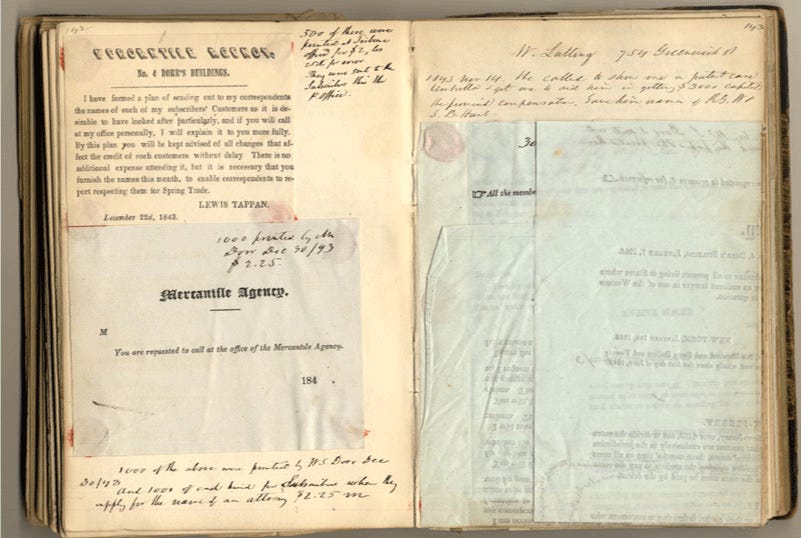

The Control Point in 1841

After the Panic of 1837 exposed the lack of reliable commercial credit information, the abolitionist merchant Lewis Tappan founded the Mercantile Agency. The agency built the first B2B credit network: a network of paid correspondents across the country, mostly lawyers, bankers, and other local observers, who reported on merchants’ solvency, reputation, and creditworthiness. A young Abraham Lincoln was reportedly among the early network correspondents.

The merchants were the vertical integrators of their era: they bore the capital and operating risk. They held the inventory, warehouses, supply chain, and customer relationships. The Mercantile Agency owned something else: a valuable information layer critical to recurring, high-value business credit decisions.

The correspondent network gave the agency the data. That data was then compiled into useful decision-support systems for credit. Each new piece of information, including payments and delinquencies, improved the system, enabling an “asset-light” merchant to capture the control point. The Mercantile Agency eventually became Dun & Bradstreet, one of the most enduring business-data companies in the United States.

Christensen’s Law of Conservation of Attractive Profits applies to the Mercantile Agency as well as to Vertical AI: profit does not necessarily accrue to the company that owns the most layers. It migrates toward the company that controls the performance bottleneck.

The Mercantile Agency needed thousands of correspondents and decades of patience to capture its control point: the merchant credit ledger. They owned neither the inventory nor the warehouses, but rather the clearinghouse of business trade.

Vertical AI founders should look for the modern equivalent of that ledger. Own enough of the stack to make it accurate, durable, and compounding. Serve a domain so well, displacement becomes not only difficult but uninteresting.

If Tappan or Christensen could give you one piece of advice today, it might this: bundle and unbundle with care.

Thanks for reading The Verticalist. Euclid partners with Vertical AI founders at inception. If someone in your network is building in the space, we would love to meet them. LinkedIn is the best place to reach us.

Our friends at Tidemark have done great work on the control points in Vertical Software and have extended that work to AI-Native challengers.