SaaSpocalypse Now

Five myths about the software selloff — and what they mean for Vertical AI

Public SaaS stocks just went through a brutal repricing, with the median price down 32%. Median EV/Revenue tanked from 9.1x to 4.8x — a 42% contraction, during which 86% of companies saw their multiples compress. At minimum, this should tell us something about how the potential of AI is interpreted by the wider market — we’re interested in it as a foil for thinking about the future landscape of application layer software.

Public market performance, of course, is an imperfect teacher for founders and VCs. After all, public SaaS downturns can have both bad (the application layer is dying) and good (the next generation is taking over fast) implications for startups. Especially in moments of uncertainty, markets can be sentiment-driven — a Buffett voting machine that’s at best distracting to those concerned with 10-20-year cycles.

Yet certain conclusions have been popularized in the wake of the “SaaSpocalypse” that, absorbed without proper context, lead to the wrong vision for the future of the software. This essay is our attempt to make sense of the lessons we can draw from public SaaS movements over the preceding months: dispelling some that unfairly discount the potential for AI-native software, and highlighting others we think are portents for the future of the Vertical AI landscape.

1. Vertical Software Has Stopped Growing

Tom Tunguz’s article from a few months back was a great, concise summary of the recent public market movements. Ultimately, it laid the blame for poor vertical SaaS performance on fundamentals. Despite ostensible value in their moats, he said, they were repriced more aggressively because they are slowing down:

Vertical software companies like Veeva, AppFolio, & Procore possess genuine moats: regulatory barriers, deep integrations that make their products operating systems for entire industries, years of accumulated domain data that is particularly relevant for AI. If anything, these companies should be harder to displace than generic workflow tools. Yet vertical software trades at the steepest discount. Because they simply aren’t growing that fast.

— Tom Tunguz, How Markets Price AI Risk

You wouldn’t have to indict vertical SaaS as a business model to believe that story. On average, public vertical SaaS companies are nearly 10 years older than horizontal peers. A thick cohort of legacy, pre-internet vertical players — Dye & Durham (1874), FICO (1956), Agilysys (1963), Tyler (1966) — pulls the 75th percentile vertical age to 42 years old versus 27 for horizontals, which might explain slower growth across the bucket.

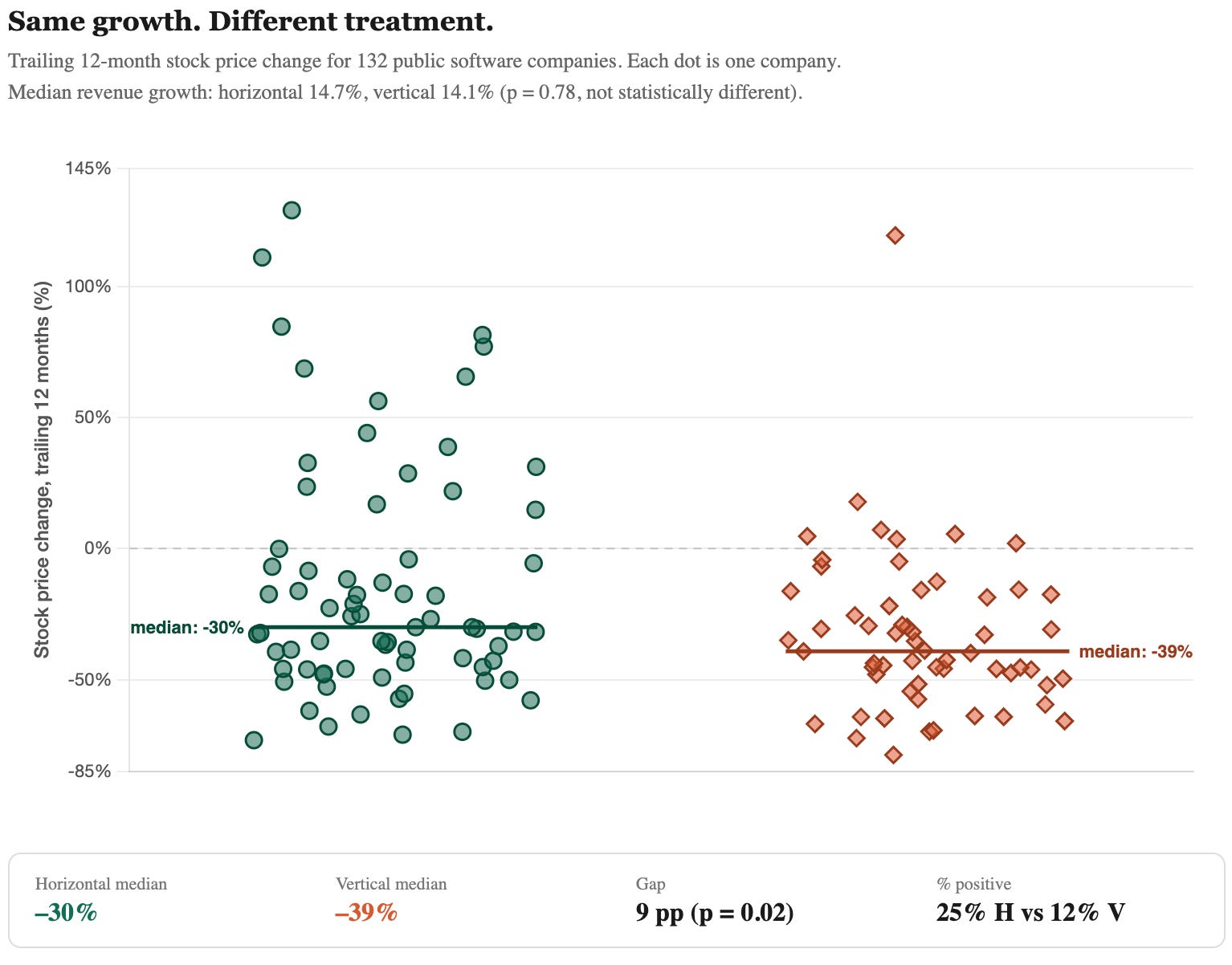

There’s just one small problem with the “slower growers” explanation: it’s not true. Our review of 130 public SaaS stocks yielded effectively no difference between median LTM growth: horizontals grew 14.7%, verticals 14.1%. Across our SaaS comp set, fundamentals had almost no correlation with price performance. Revenue growth correlated with returns at r = 0.07; EBITDA margins at -0.03. Within Vertical SaaS, the bottom 15 performers had higher median margins and higher median growth than the top 15.

2. Vertical Software is Less AI-Moated

In his piece, Tom also summed up the popular view well: “Vertical software has fallen 43% this year. DevTools, just 21%. The gap between them… tells you what markets actually believe about AI.” While facially accurate, this takeaway misses a few things.

It implies that the market concluded that vertical software itself — by nature of being industry-specific — was vulnerable to AI. Many have run with that conclusion, surmising that vertical SaaS is easier to replicate with LLMs.

Those conclusions fly in the face of two realities, however:

The performance differential had more to do with a handful of horizontal SaaS companies that were “graded” by the market as being not just defensible but poised to benefit from the rise of AI. The following tickers got the “AI picks-and-shovels” treatment, appreciating by >50%: Bandwidth (telecom APIs), Datadog (observability), MongoDB (database), Twilio (comms APIs), Fastly and Akamai (CDN), JFrog (software supply chain), and Innodata (AI training data).

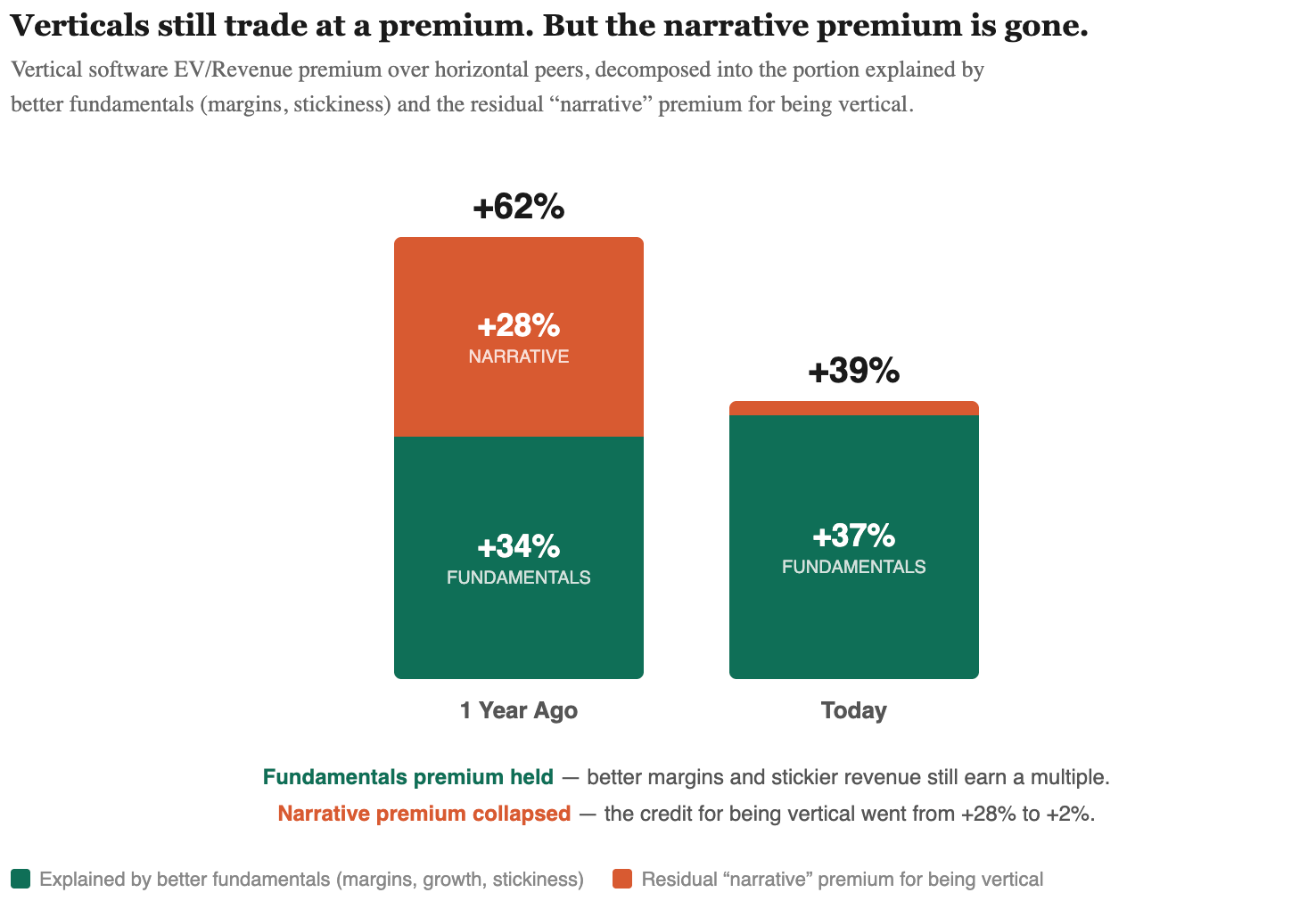

Vertical SaaS still trades at a premium to horizontal peers, even accounting for fundamentals. The recent repricing reflects a significant rethinking of that “narrative premium.” In other words, vertical software traded much higher to begin with, so this is perhaps just a case of the bigger they are, the harder they fall. From our perspective, this largely reflects a devaluing of moats that are not immediately visible in the P&L (more on this to come).

None of this suggests that Vertical SaaS is less defensible from AI. It suggests that perhaps the traditional valuation bonuses they fetched are less rich—and that only the most legible, near-term AI tailwinds are being rewarded (more on that below).

3. The Market Has Correctly Repriced Terminal Value

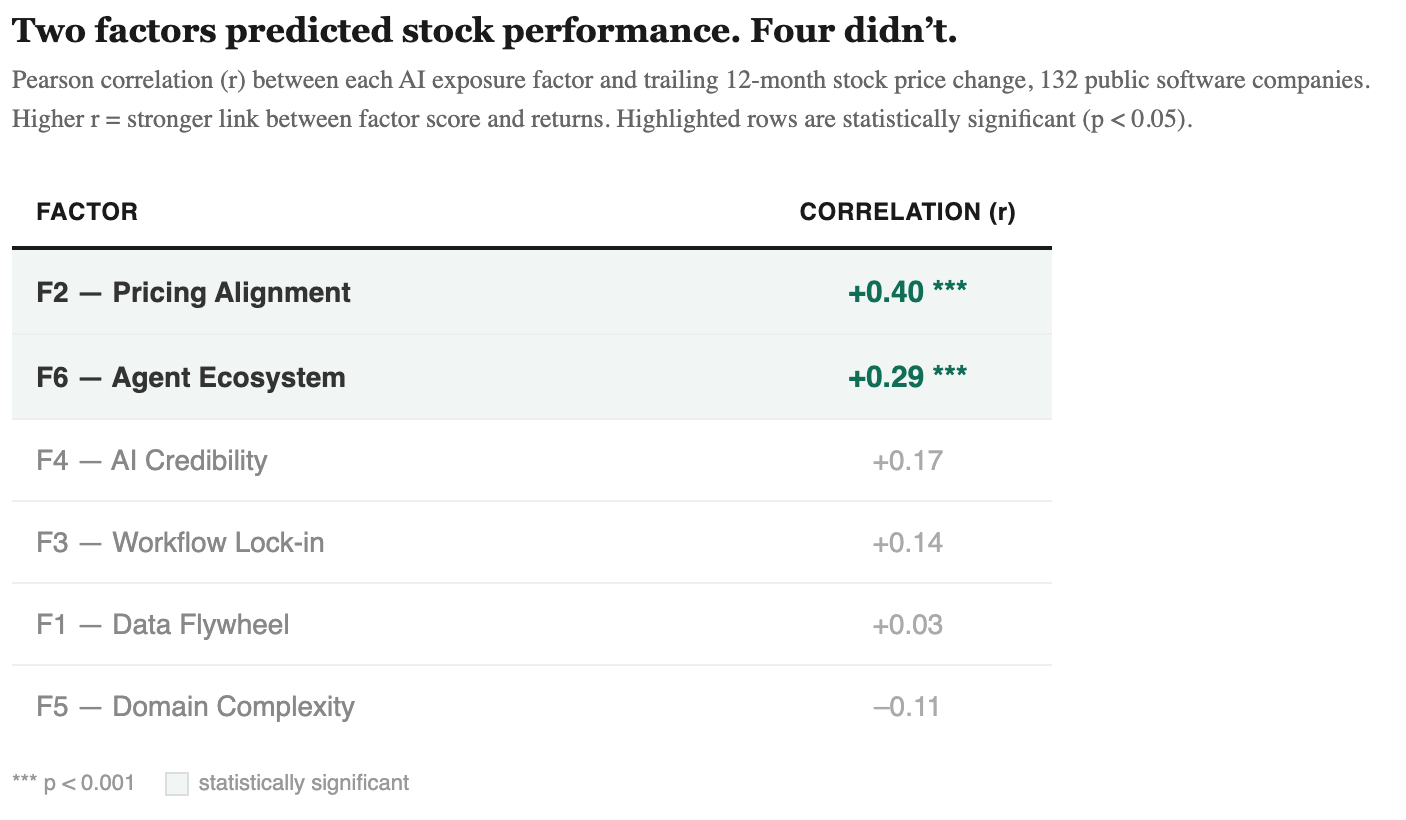

Looking across the whole data set, consumption-based access & pricing models were the clearest driver of software performance over the last several months. We came to this conclusion by blind-scoring all 130 software stocks on the six most important a priori considerations1. Strong correlations should suggest how the market is “grading” AI exposure. Whether a company’s existing product and monetization will thrive in a world where agents are doing more and more work is a very reasonable measure of immediate AI benefit. It’s telling, however, that less tangible moats — workflow depth, proprietary data, regulatory & domain complexity — were not rewarded.

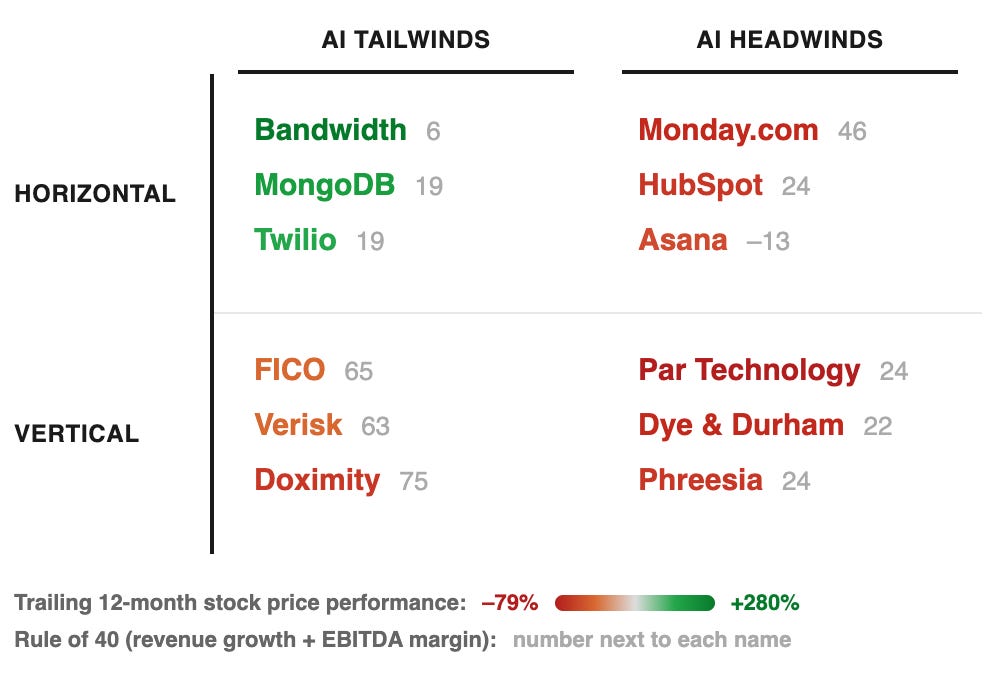

We can even simplify the moat that mattered to one question: Are you agentic infrastructure?

Let’s put that question to the test by comparing Bandwidth (a horizontal that appreciated 280% despite an R402 of 6) and Doximity (a vertical that drew down 65%). If you aren’t familiar with Bandwidth, they’re a Twilio competitor — a CPaaS (Communications Platform as a Service) that sells APIs for voice and SMS used by RingCentral, Zoom, etc. In an AI world, every voice agent that makes a phone call using BAND generates usage-based revenue. As Tom put it, “the data infrastructure tailwind is structural. More AI means more queries, more embeddings, more vector operations.” It’s less immediately clear how Doximity — LinkedIn for physicians, more or less — will benefit from agentic work under the current business model. After all, pharma and hospitals pay subscriptions to market to Doximity’s audience.

Much is lost in this simplistic view of AI moats, however. Doximity, for example, has strong network effects, with 80%+ of doctors on the platform and many hospitals requiring them to sign up. They have data gravity, aggregating proprietary clinical datasets (e.g., PeerCheck, Pathway Medical), which have immediate value to current customers. They have a relatively AI-ready talent, with a 380-person R&D team already layering AI tools (Scribe, DoxGPT) to drive new revenue from health systems. They have workflow loops that deeply integrate with telehealth, faxing, and clinical documentation. And finally, they arguably have regulatory moats from operating all this in a HIPAA-regulated environment.

It’s further evidence that the SaaSpocalypse offered reprieve only to those with immediate revenue opportunity — the potential to benefit from AI in any manner more complicated than picks-and-shovels tomorrow was flatly ignored. Not exactly a deep consideration of terminal value, as one might expect from public markets mostly concerned with next quarter’s earnings.

As Ben Thompson observed in his Stratechery interview: “the destruction and the value creation are not simultaneous in time.” Public markets are pricing the destruction phase. They are pricing the obvious acceleration. They have ignored the longer-term value creation.

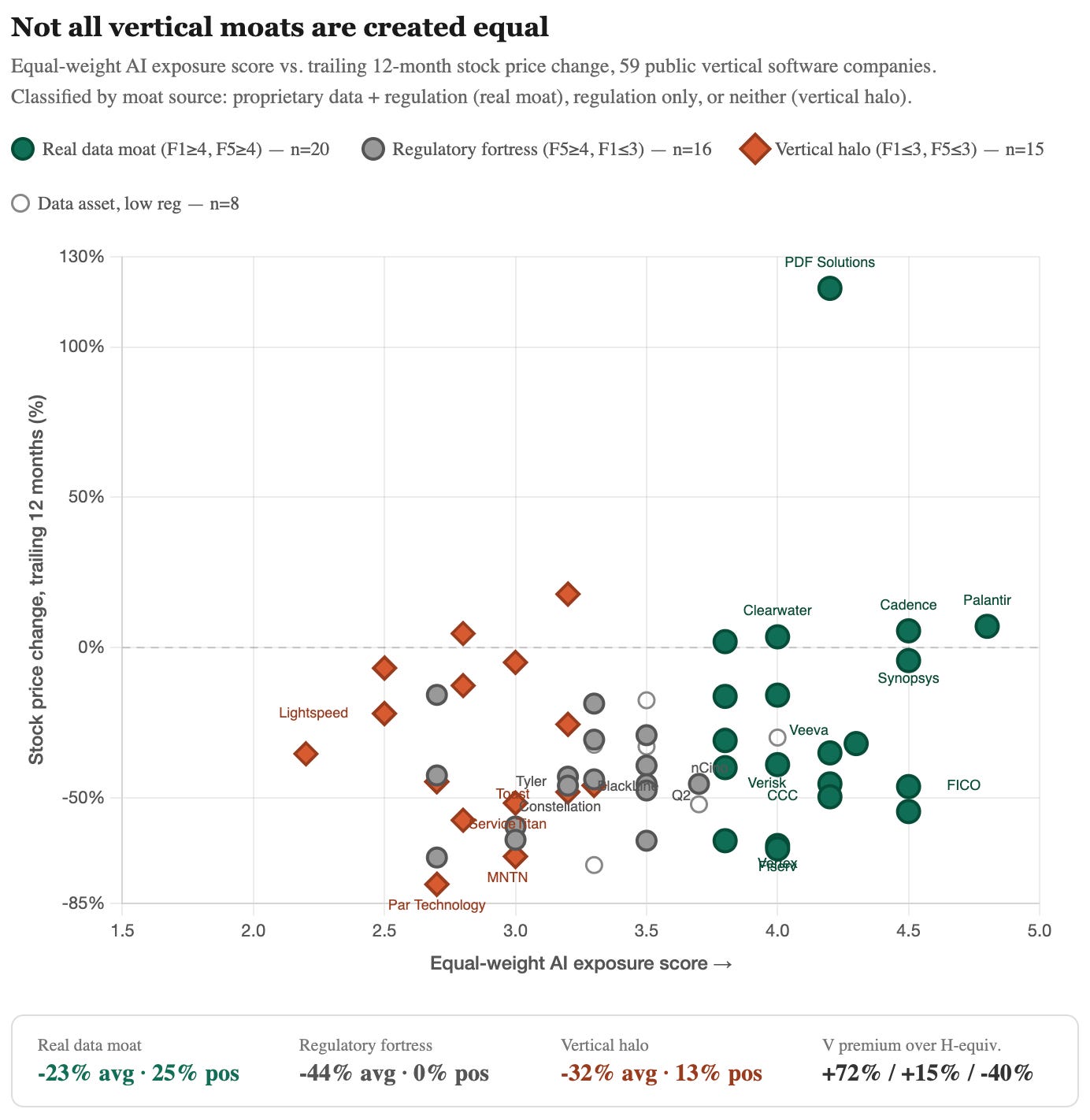

4. All Vertical Moats Are Eroding Equally

When we classify the 57 public vertical SaaS players in our dataset by source of defensibility — using the moat taxonomy from Dude, Where’s My Moat? — three groups fall out.

Proprietary data moats. Verisk, FICO, Cadence, Veeva, CCC (20 total). These sit on data that cannot be reconstructed or easily replicated. A year ago, they traded at 220% above what a horizontal with the same growth and margins would command. Today: 72%. 18 of 20 are still trading above their horizontal equivalents.

Regulatory barriers without compounding data. Tyler Technologies, ADP, Constellation, nCino, Q2 (16 total). Legal and procedural barriers to entry, rather than data-driven ones. Their premium went from 120% to 15%.

The vertical halo. ServiceTitan, Par Technology, Toast, Lightspeed, MNTN (15 total). They traded at a 41% premium a year ago on the vertical SaaS narrative — own the vertical, high NRR, extensibility. Today, they trade at a 40% discount to the horizontal equivalent.

Clear and present vertical data moats are still rewarded in the market with elevated multiples (even after accounting for fundamentals). Along with pretty much everything outside of immediate AI revenue tailwinds, however, the recent repricing assigned zero value to even the strongest cases of data gravity.

In an essay three months ago, we shared a simple litmus test on the defensibility of Vertical SaaS: Is the data proprietary? Is there regulatory lock-in? Is the software embedded in the transaction? Two or three yeses and you’re probably fine. The market’s repricing roughly tracks this — proprietary data moats still command a 72% premium. But it’s assigning nearly zero credit for the second and third.

5. The Application Layer Is Dying

The market is pricing the impacts of widespread AI adoption in our economy, including both the decreased cost of software development and the resulting absorption of work by agents. It isn’t yet pricing in the rise of a new generation of AI-native software. Accordingly, pipes that serve AI, generating near-term revenue uplift, get insulated — while software across the board sees erosion, with staying power in question. It certainly isn’t pricing to an application-layer AI steady state, in which data and workflows will be more valuable than ever.

As we shared in our initial essay on the SaaSpocalypse earlier this year, we are still quite early in the destruction phase, despite the market panic.

Some vertical software companies will die, though we think the durability of those names is far higher than that of their horizontal peers. Some of the next generation of vertical AI companies will be built on the rubble, but most of them will be built on green fields. The market, by definition, cannot expand if it’s just ripping and replacing legacy vendors.

— The Verticalist

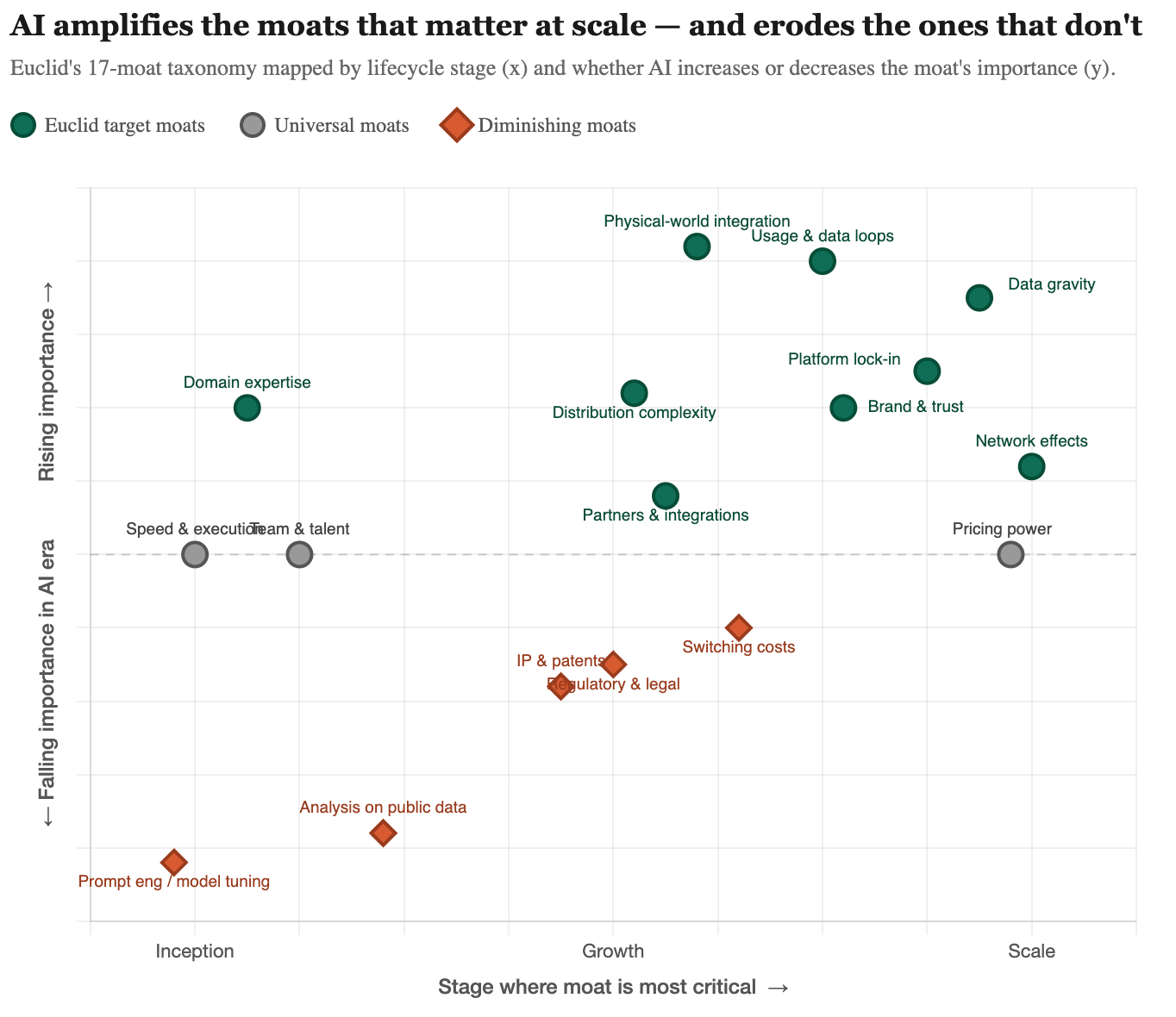

LLMs have demonstrated the value of scaling for training data and the ability of agents to become more capable through reinforcement learning. To expand beyond language-centric use cases, however, AI will need domain-specific data and decision context. It exists nowhere on the public internet, isn’t for sale, and in many cases, it lives only in the minds of professionals. Vertical platforms have always been best positioned to capture this data. Only now is it becoming so valuable — even if the market hasn’t yet priced it in.

The bears assume AI will shrink the market for vertical software. They're wrong — it will dramatically expand it. AI needs domain-specific data and decision context to move beyond language-centric use cases, and that data exists nowhere on the public internet. It lives in the workflows, transactions, and institutional knowledge that vertical platforms are uniquely positioned to capture. Some incumbents with strong moats and the willingness to cannibalize their own products in favor of an AI angle will thrive. But the biggest winners will be a new generation of AI-native companies — built not just on the rubble of legacy software, but also on greenfield use cases, budgets, and verticals the public market hasn’t even begun to consider.

Proprietary Data Flywheel measures whether the company accumulates irreplaceable, compounding data through its product — the kind of dataset a foundation model or new entrant couldn’t reconstruct in 12 months. Verisk’s decades of actuarial claims history scores a 5. Dropbox’s file storage, where the data belongs to the customer, scores a 1.

Pricing Alignment captures whether the revenue model benefits or suffers when AI agents generate more activity. Consumption and usage-based models where more API calls mean more revenue — Bandwidth, MongoDB, and Datadog score highest. Seat-based models where AI reduces the number of humans who need licenses — Asana, Monday.com, Workday — score lowest.

Workflow Replaceability asks how deeply embedded the product is in the customer’s operations, scored inversely — a 5 means the product is nearly impossible to rip out. Oracle’s ERP and ADP’s payroll infrastructure score 5. Dropbox and Amplitude, which could be swapped in a week, score 1.

AI Credibility assesses whether the company has the engineering team, R&D investment, and leadership DNA to build real AI capabilities — not just bolt on a chatbot. We looked at R&D as a percentage of revenue, the CEO's background, AI acquisitions, and named AI products with measurable adoption. Palantir and Datadog score 5. Tyler Technologies and Constellation Software score 2.

Domain Complexity measures how regulated, specialized, or expert-dependent the customer environment is. Deep regulatory barriers that take years to satisfy — FDA clinical trial submissions at Veeva, CJIS certification at Tyler, credit scoring regulation at FICO — score 5. Horizontal markets with no such barriers score 1.

Agent Ecosystem asks the forward-looking question: in a world where AI agents orchestrate enterprise workflows, does this product get more or less usage? Products that agents can route through — databases, communication APIs, security layers, observability platforms — score 5. Products that are human coordination layers agents are unlikely to use — task trackers, dashboards, file storage — score 1.

Rule of 40 Score: Revenue Growth + EBITDA Margin.