The Vertical Report 2026

Euclid's annual analysis of 4K+ financings, 250+ exits, and the major trends in Vertical AI

2025 was the year Vertical AI moved squarely from hypothesis to reality. After a 2024 defined by AI infrastructure buildout and foundation model wars, capital began flowing decisively toward industry-specific use cases.

The data tells a clear story: across 4,395 VC financings totaling $186B in 2025, vertical startups captured 53% of deal volume and 30% of capital deployed. That share would be even higher if not for a handful of horizontal mega-rounds: OpenAI’s $40B, Anthropic’s $13B, plus several other GPU cloud and foundation model raises. Strip out the 12 deals sized $1B+ and vertical raises took in 51% of 2025 capital.

Some new trends emerged, while others held strong. Healthcare and Financial Services—no surprise—remained the twin pillars of vertical investing, combining for nearly 1,100 deals. 2025’s foremost emergent verticals, however, were Manufacturing & Industrials, Legal, and AEC & Trades. Manufacturing saw a 41% increase in deal count from Q1 to Q4. Legal produced two of the year’s largest rounds, with Clio ($850M) and Filevine ($400M): even if neither of these companies is AI-native, both are quickly becoming AI-powered as competition scales fast. And AEC & Trades saw both early and late stage enthusiasm, anchored by CompanyCam’s $415M round that made it Nebraska’s first unicorn.

On the exit side, 2025 delivered $131.1B across 158 vertical exits—a number skewed at the top by Ansys and a handful of mega-buyouts, but broad at the base: Healthcare alone generated 43 exits worth $17.1B, and the IPO window cracked open with 18 vertical offerings including Via and Hinge Health. Including horizontal deals, 2025 exits totaled $234.9B across 254 transactions—vertical companies captured 56% of total exit value. Excluding Ansys (the $35B acquisition that threw all the numbers off), vertical liquidity was almost exactly on par with non-vertical.

This report examines 2025 in full: deal volume and capital deployment trends, vertical-by-vertical breakdowns, stage dynamics, top investors, and geographic concentration—plus profiles of twenty thematically notable vertical deals to know. We conclude this report with Euclid’s perspective on the undercurrents and structural shifts we believe will define Vertical AI in the year to come.

I. Financing Overview

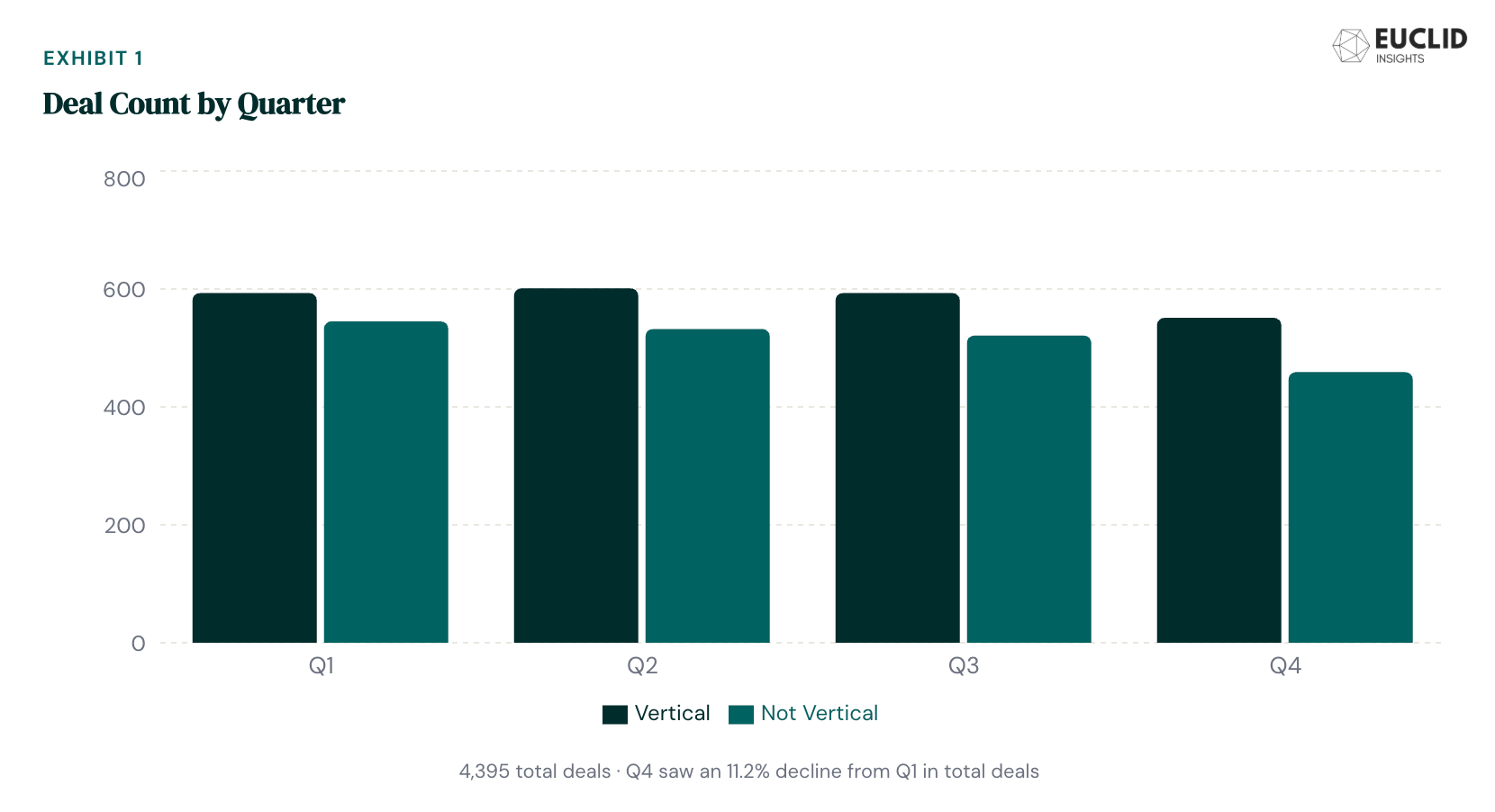

The US and Canadian VC market produced 4,395 software and AI financing deals of $1M+ in 2025 (excluding non-relevant deals), deploying $186B in aggregate capital. Deal volume across quarters was relatively even: Q1 and Q2 combined for 2,271 deals (52% of the year), while Q4 saw a cooldown to 1,010 deals—the lightest quarter and an 11% decline from Q1.

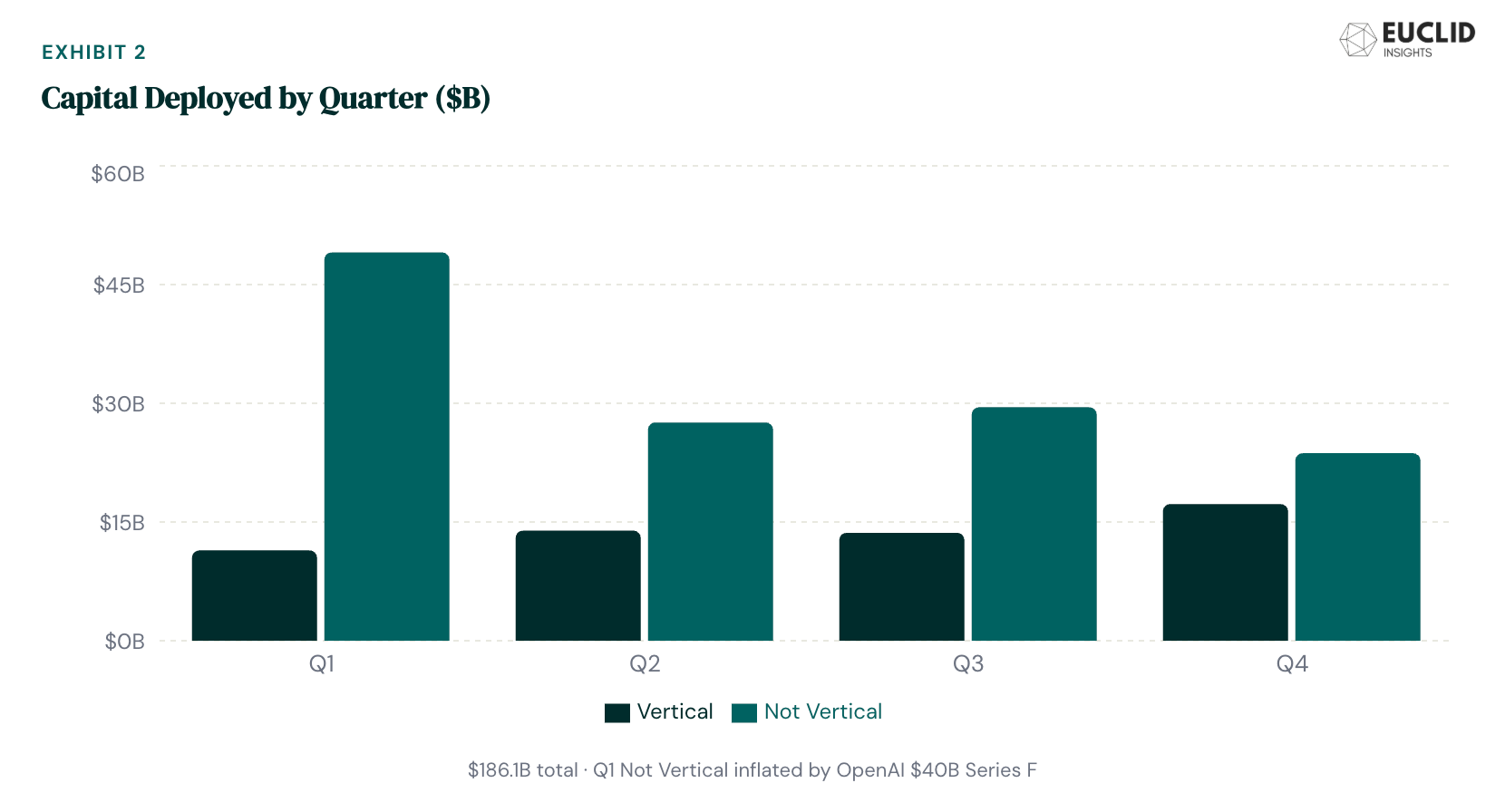

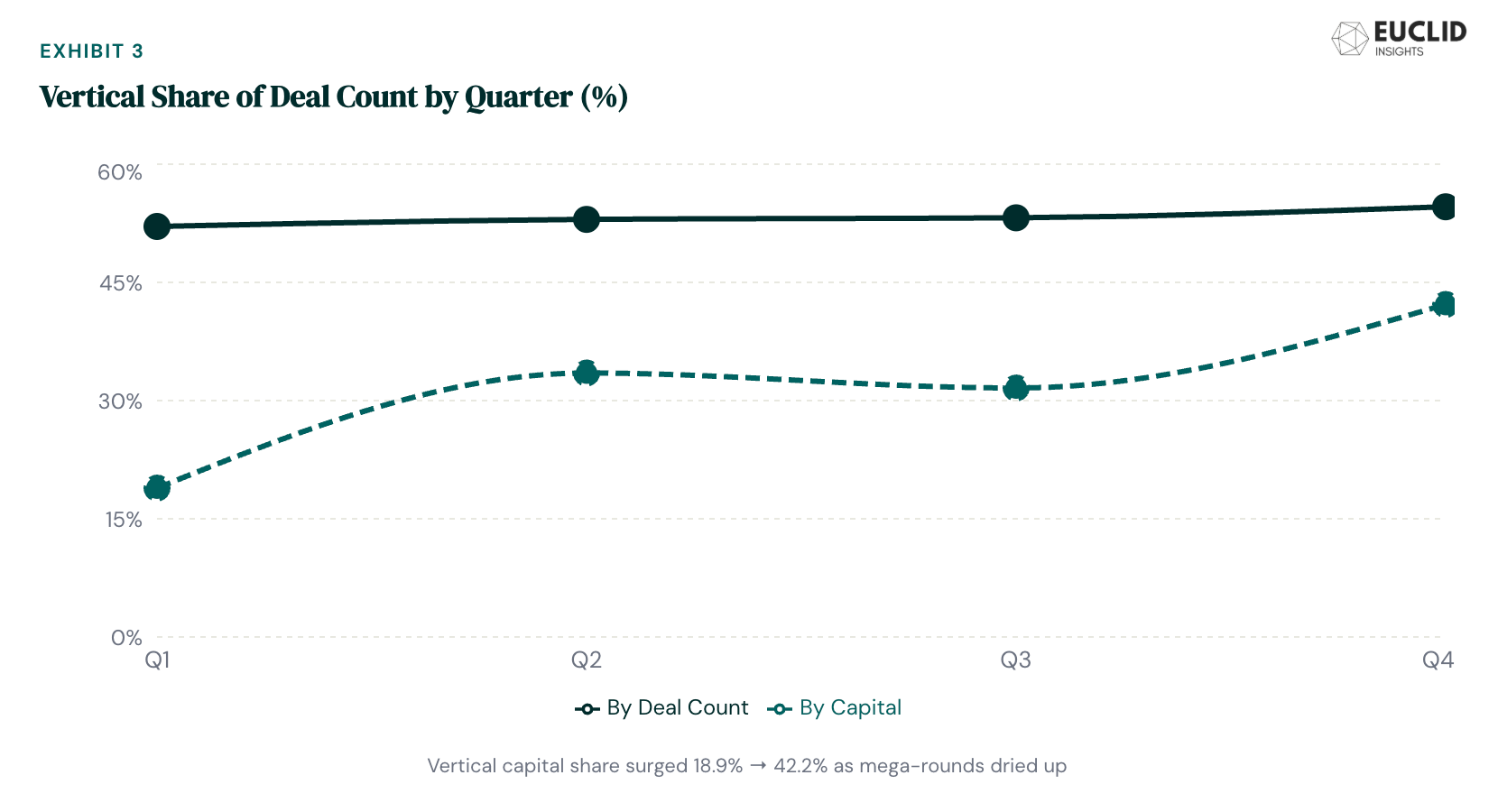

Capital deployment told a different story. Q1’s $60.5B was inflated by OpenAI’s $40B Series F—strip that out and Q1 looks closer to $20B, making the quarterly trajectory even more—a pattern consistent with our thesis on vertical AI market sizing. Vertical companies captured 19% of Q1 capital, then surged to 34% in Q2 as non-vertical mega-rounds dried up, before settling at 32% in Q3 and climbing to 42% in Q4. The full-year split—$56.2B vertical versus $129.8B non-vertical—still understates the vertical story thanks to a small handful of foundation model and infrastructure rounds (OpenAI, Anthropic, GPU cloud companies) in the non-vertical capital pool. On a per-transaction basis, verticals averaged $24.0M in deal size versus $63.1M for non-verticals, reflecting the latter’s concentration in capital-intensive model training and infrastructure.

The Vertical Share Is Growing

By deal count, vertical’s share held steady in the low-to-mid 50s: 52% in Q1, 53% in Q2, 53% in Q3, and 55% in Q4. The Q4 figure—more than half of all VC deals targeting a specific industry—represents the year’s high-water mark and suggests the vertical share is still expanding.

This wasn’t a sudden shift. In 2024, vertical applications already led deal count—especially in exits, where over 80% of PE-backed software acquisitions targeted vertical companies. But 2025 confirmed the trend quantitatively: the funding market is reorienting around industry-specific applications, and the Q4 acceleration suggests this isn’t cyclical.

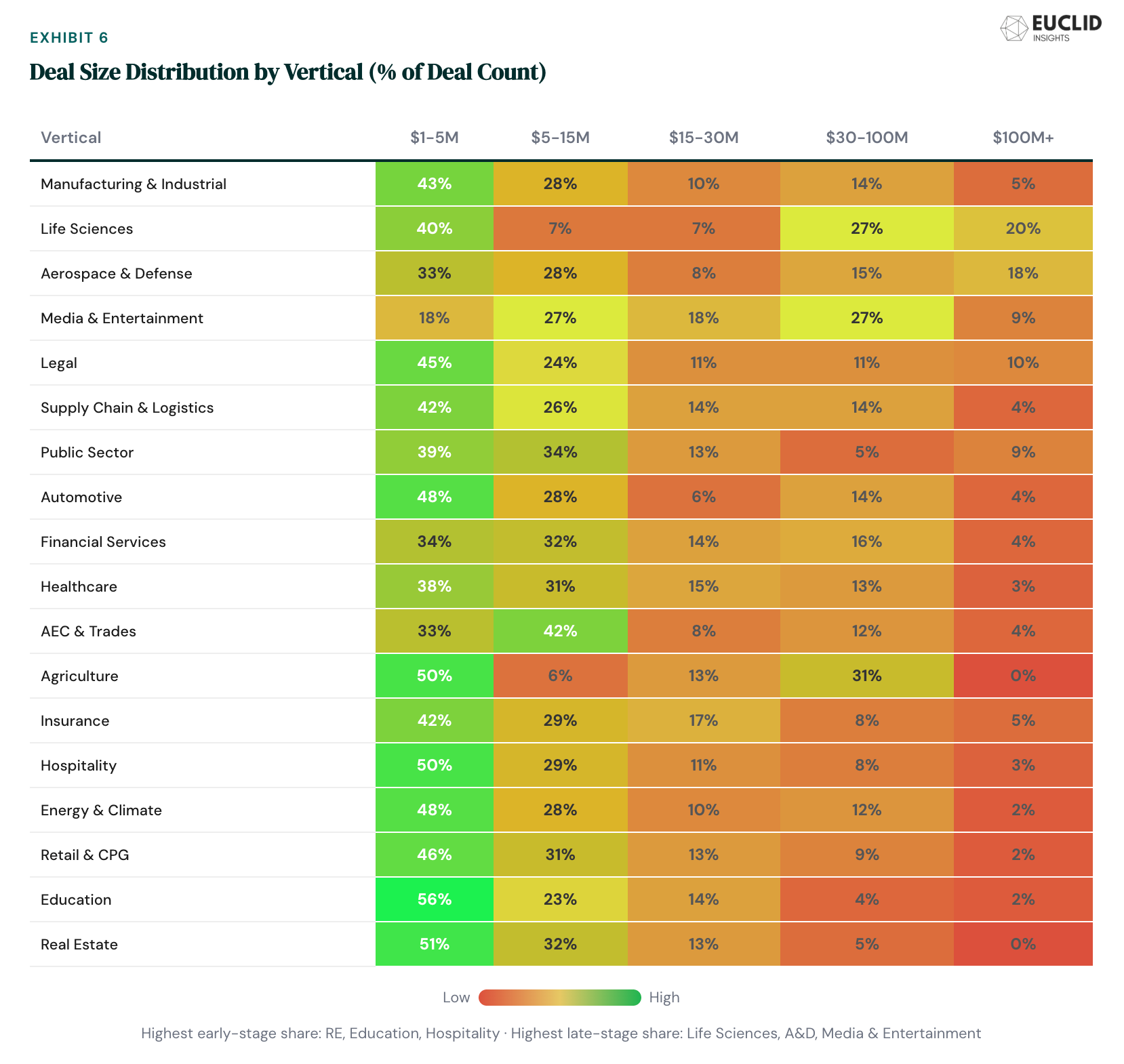

Deal Size Distribution

The 4,395 deals break down into five size buckets that reveal the market’s shape. $1–5M deals dominated at 1,733 transactions (39%), the earliest-stage formation layer. $5–15M rounds accounted for 1,357 deals (31%), the first scaling tier. $15–30M and $30M+ rounds made up 591 (13%) and 506 (12%) deals respectively, while $100M+ mega-rounds totaled 208 deals (5%).

Vertical companies held the majority at every deal size except $100M+, where the split was 45%/55%—essentially a coin flip driven by infrastructure and foundation model mega-rounds. The most vertical-skewed size tier was $30M+ at 58%, with $1–5M close behind at 54%. This makes intuitive sense: vertical companies build moats through industry-specific data, integrations, and domain expertise that compound over time, making them fundable at scale. At the $100M+ tier, infrastructure and horizontal AI companies (GPU clouds, foundation model labs) absorb capital at a rate that no individual vertical can match.

Quarterly momentum within size buckets tells another story. $100M+ rounds grew from 39 in Q1 to 55 in Q2, then held at 57 in Q3 and Q4—remarkably stable after the initial ramp. But the $1–5M tier—the new company formation layer—dropped from 503 in Q1 to 362 in Q4, a 28% decline. This could signal a tightening at the earliest stages, though Q1 2025 may have been inflated by deals delayed from late 2024.

II. Vertical-by-Vertical Analysis

Not all verticals are created equal. Healthcare and Financial Services are GDP-dominating, highly diverse markets with hundreds of deals each, while Agriculture and Life Sciences remain more niche. The more revealing analysis is relative momentum—which verticals are gaining share, and where is the capital concentrating?

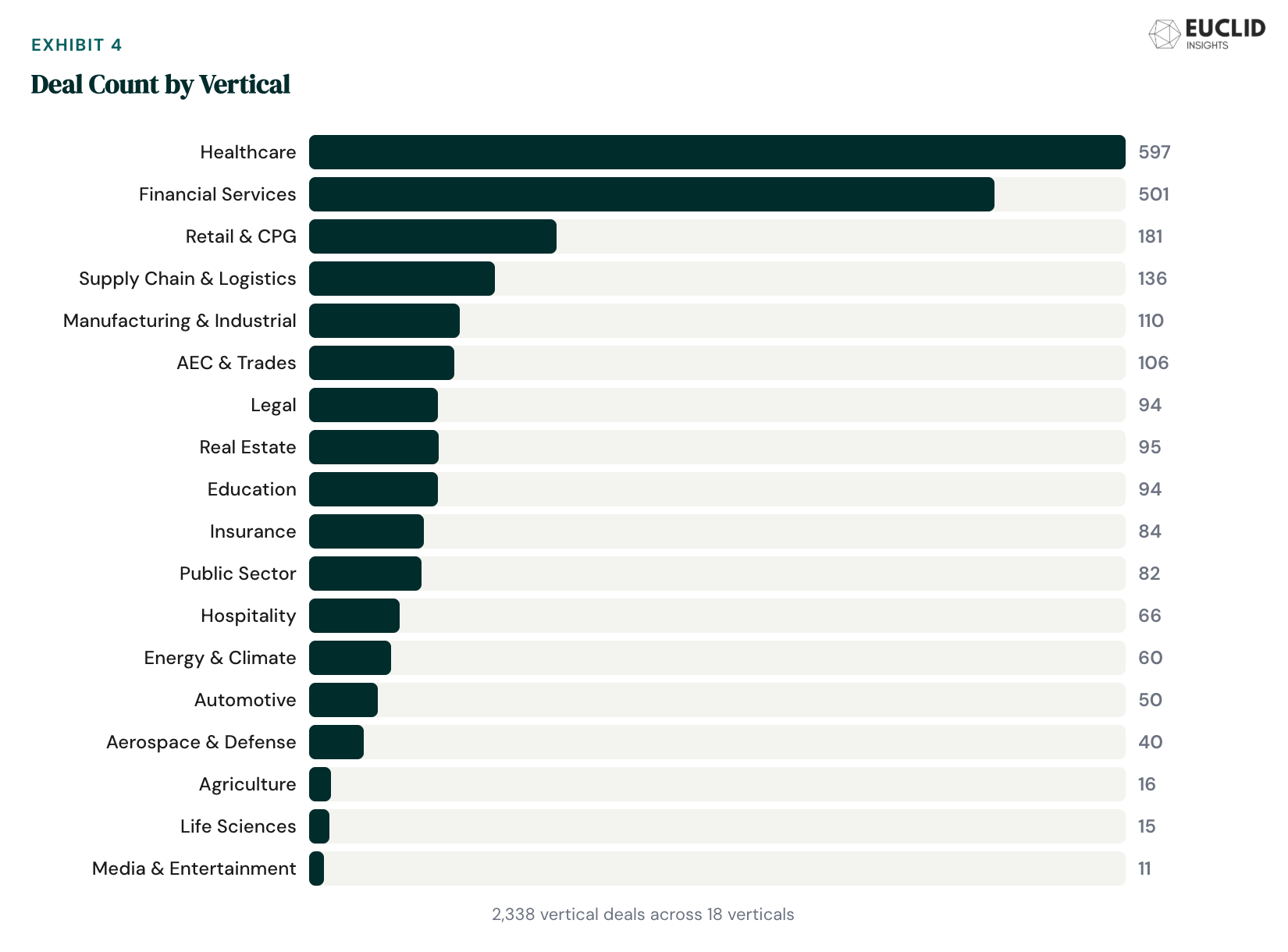

Healthcare (597 deals, $11.8B)

Healthcare was the most active vertical by deal count and the also the largest vertical by capital at $11.8B (slightly ahead of Financial Services at $11.7B). The stage mix skewed early: 38% of Healthcare deals were in the $1–5M tier, and the median deal was $6.8M. The big stories here were clinical AI documentation (Abridge’s $316M Series E, Judi Health’s $400M Series F), value-based care infrastructure (Strive Health’s $550M Series D), and the steady drumbeat of digital health buyouts—Modernizing Medicine ($5.3B), CentralReach ($1.9B), and VaxCare ($1.7B) were among the largest healthcare exits. Healthcare also led vertical exit count with 43 transactions worth $17.1B.

Financial Services (501 deals, $11.7B)

FinServ was the second-largest vertical by count and nearly tied with Healthcare by capital at $11.7B, exemplifying the embedded fintech thesis we outlined in “Vertical FinTech.” ($500M). The vertical also produced two IPOs: Figure Technology Solutions and Wealthfront. Deal activity was remarkably consistent quarter to quarter, suggesting structural depth rather than hype-driven surges. Ramp’s back-to-back Series E rounds ($200M in June, $514M in September) at a $22.5B valuation punctuated the year, alongside Plaid ($575M) and Wealthsimple ($536M).

Emerging Verticals

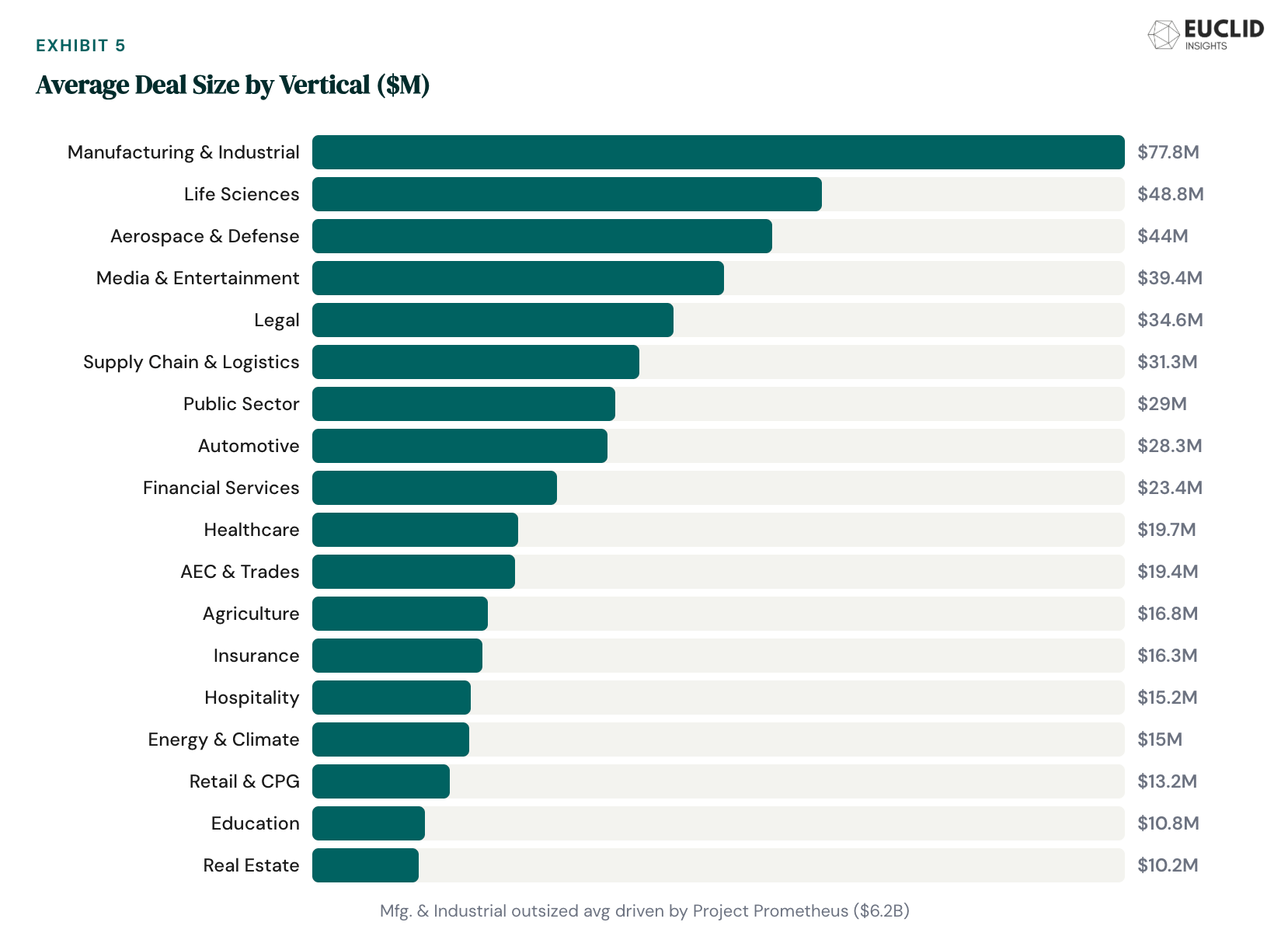

Manufacturing & Industrial — 110 deals, $8.6B

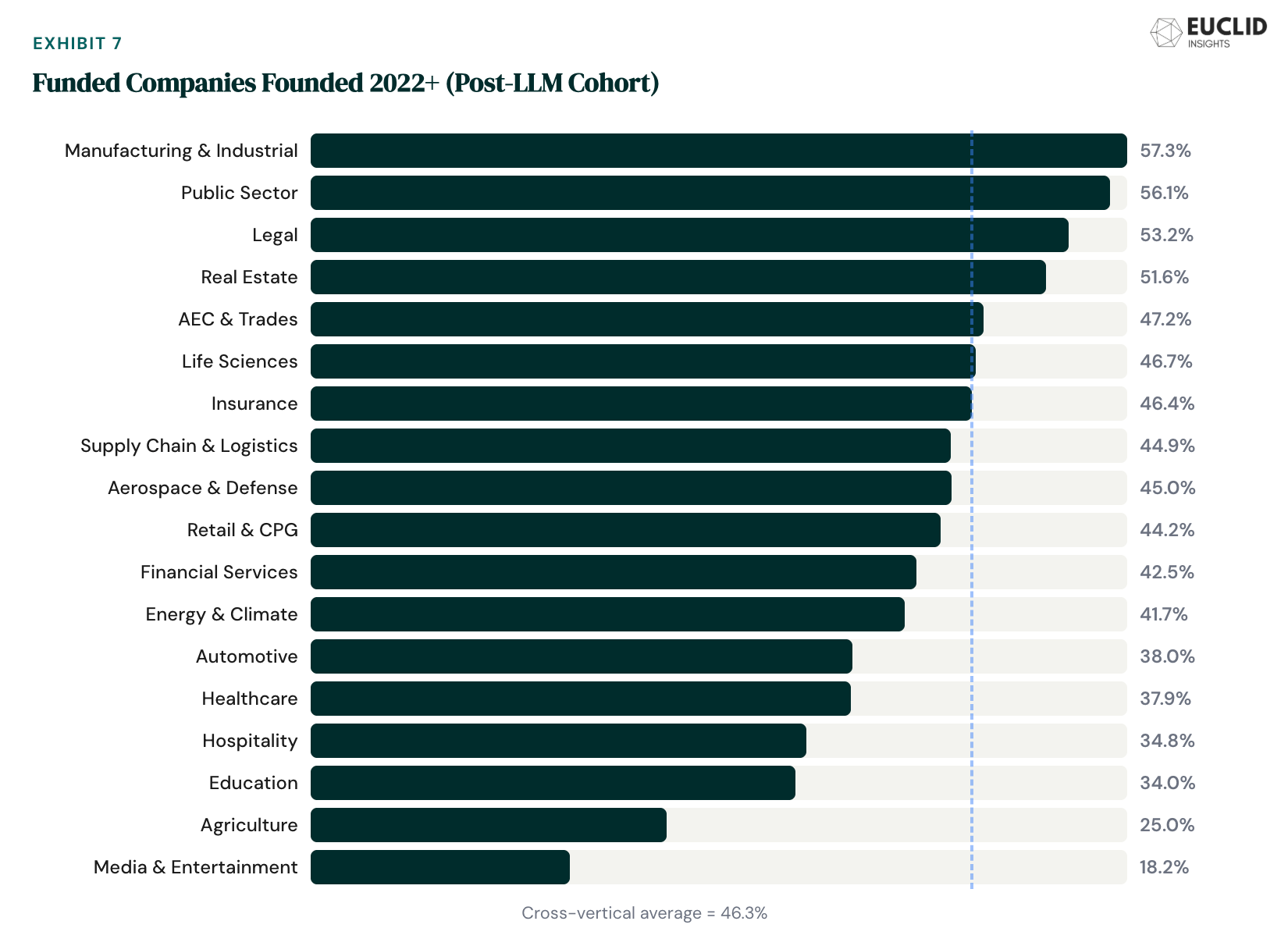

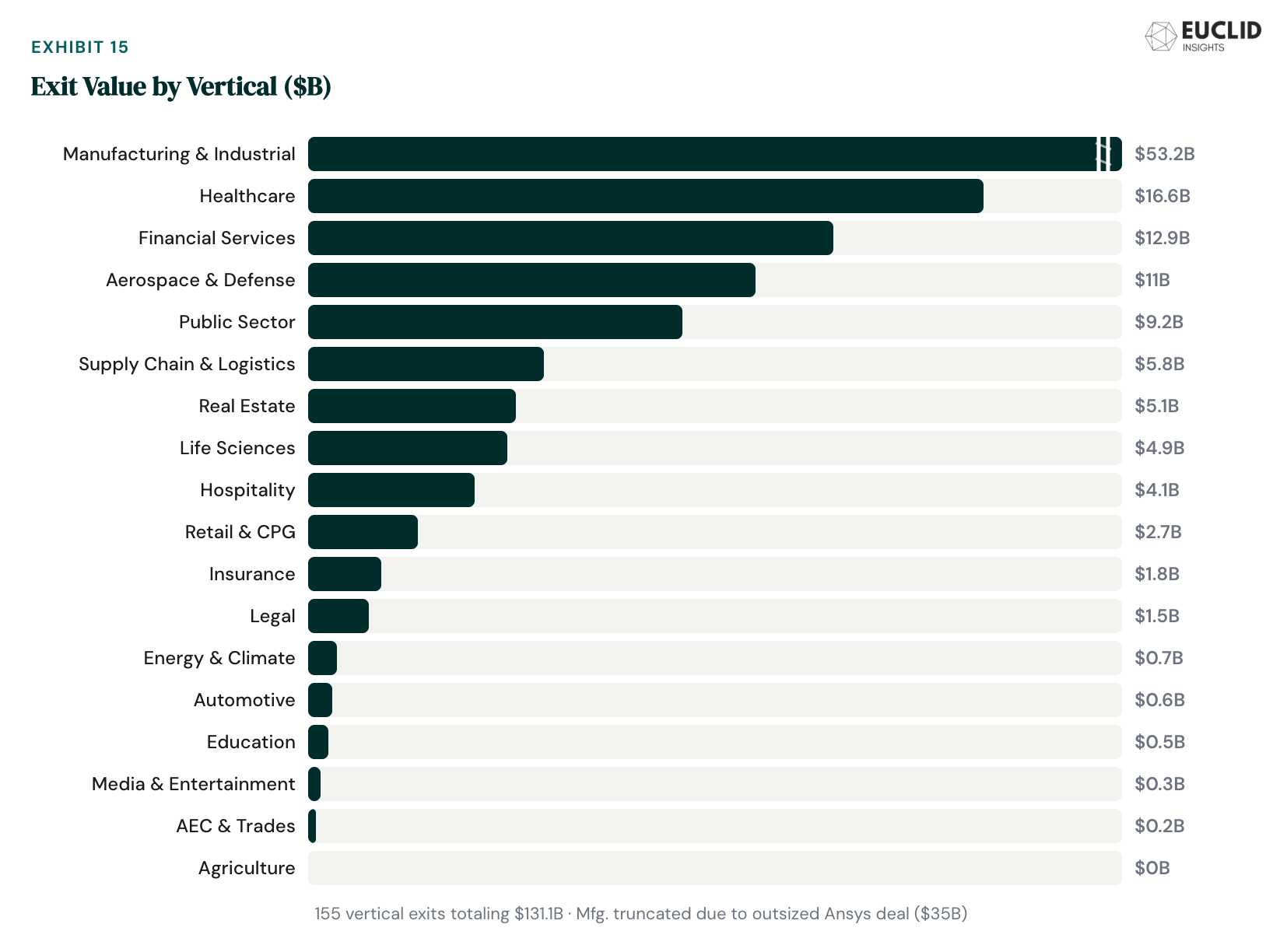

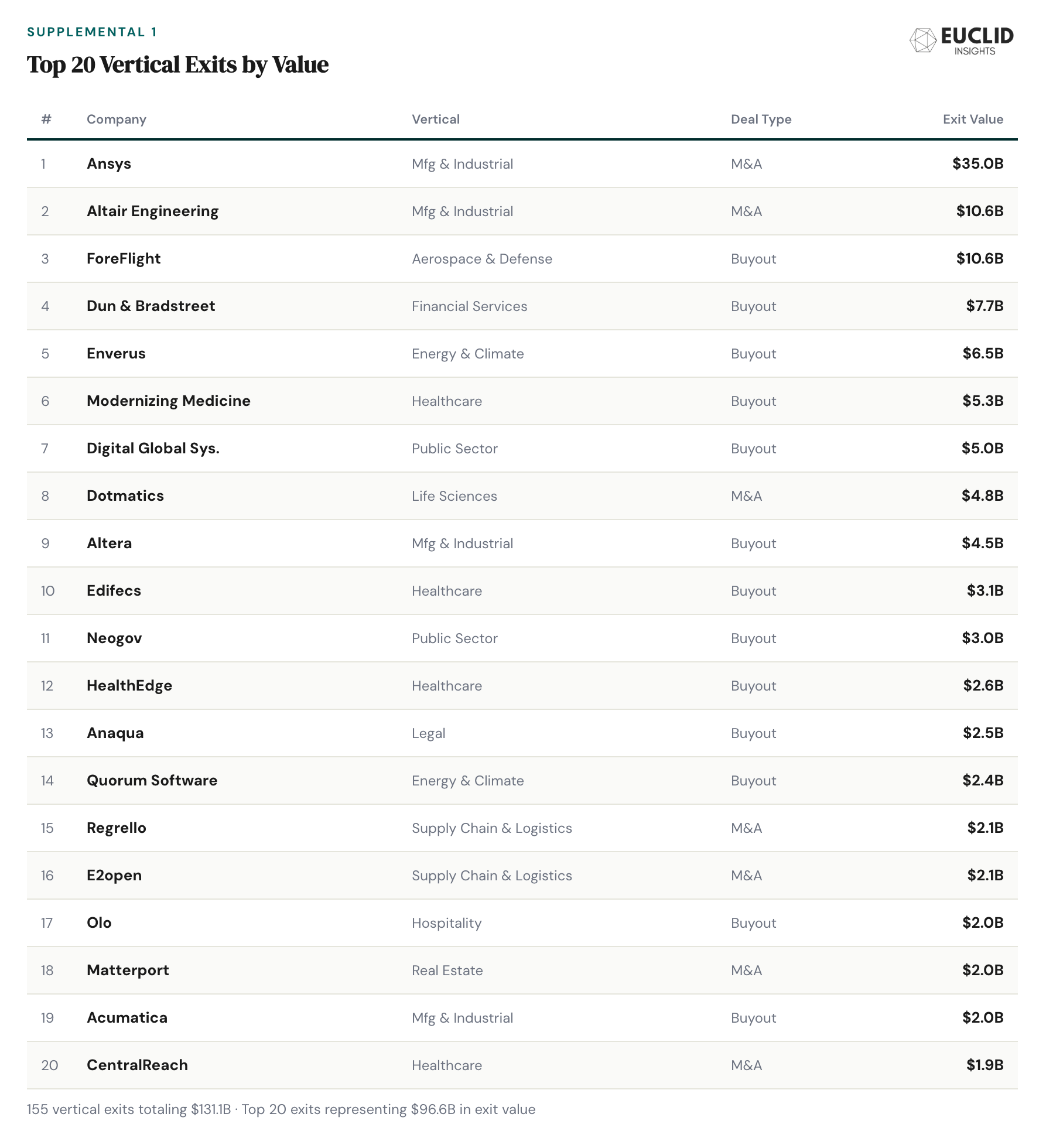

Deal count rose 41% from Q1 to Q4 (22 to 31 deals), and the vertical produced the year’s second-largest financing—Project Prometheus at $6.2B. Jeff Bezos’s return to operational company-building with a “physical AI” thesis for chip packaging, automotive assembly, and aerospace is a strong signal. On the exit side, Synopsys’s $35B acquisition of Ansys was the largest vertical exit of the year. Manufacturing had the highest share of post-2022 companies (57%) of any major vertical, confirming that AI is creating a new generation of industrial startups.

Legal — 97 deals, $3.3B

Two of the year’s 15 largest vertical rounds were in legal—Clio’s $850M and Filevine’s $400M. Both are case management platforms adding AI capabilities, and both are scaling aggressively through acquisition (Clio’s $1B vLex acquisition, Filevine’s push into corporate legal). 43% of Legal deals were in the $1–5M tier, with the category gaining more share of early-stage vertical deal count from 1H to 2H than any other. Despite the maturity, a wave of new AI-native legal startups is entering the market.

AEC & Trades — 106 deals, $2.1B

The trades—construction, roofing, HVAC, plumbing—are a classic vertical software opportunity: fragmented end markets, low technology adoption, high workflow complexity. CompanyCam’s $415M round and $2B valuation (making it Nebraska’s first unicorn) is the poster child. ServiceTitan’s December 2024 IPO opened the aperture — and set the stage for a pipeline of formation-stage talent. Deals were evenly distributed across quarters (with special strength at the $5-15M deal size), suggesting sustained interest.

Other Verticals of Note

Retail & CPG — 181 deals, $2.4B

Retail saw a notable front-loading of deal activity, dropping from 53 deals in Q1 to 39 in Q4. Capital deployment showed a similar trajectory, declining from ~$700M in Q1 to ~$400M in Q4. This likely reflects both macro headwinds in consumer spending and a shift in investor focus toward B2B applications. The exits, however, were healthy: 15 transactions worth $2.7B. On the financing side, Retail gained more share of early-stage vertical deal count than any category save Legal.

Supply Chain & Logistics — 133 deals, $4.2B

Supply Chain showed continued resurgence in 2025, coming off a venture-cycle low in 2022. The per-deal average of $31.6M reflects several large growth rounds in fleet management, warehouse robotics, and freight intelligence. Q1 was the strongest quarter at 36 deals and $1.0B in capital, with a steady decline through Q4 (24 deals). The exit environment was active: 12 transactions worth $5.8B, including several large PE-backed logistics technology acquisitions.

Energy & Climate — 60 deals, $965M

Climate tech’s intersection with AI remains nascent but promising. The 60 deals included both pure-play climate software (carbon accounting, grid optimization) and AI-for-energy applications. The vertical’s modest capital figure reflects the prevalence of early-stage deals—most Energy & Climate companies are still raising sub-$15M rounds. But the opportunity is real: as AI’s energy demands grow, expect a feedback loop between energy tech and compute to drive larger rounds in 2026.

III. Stage Dynamics

The $1–5M tier—the earliest-stage layer—dominated every vertical, but the concentration varied meaningfully—a pattern we’ve explored in “What’s My Stage Again?”. Education had the highest $1–5M share at 56%, followed by Real Estate and Hospitality and Agriculture at 50%. Healthcare, by contrast, had one of the lower early-stage shares at 38%, reflecting the category’s relative maturity—more companies are raising larger rounds as they scale.

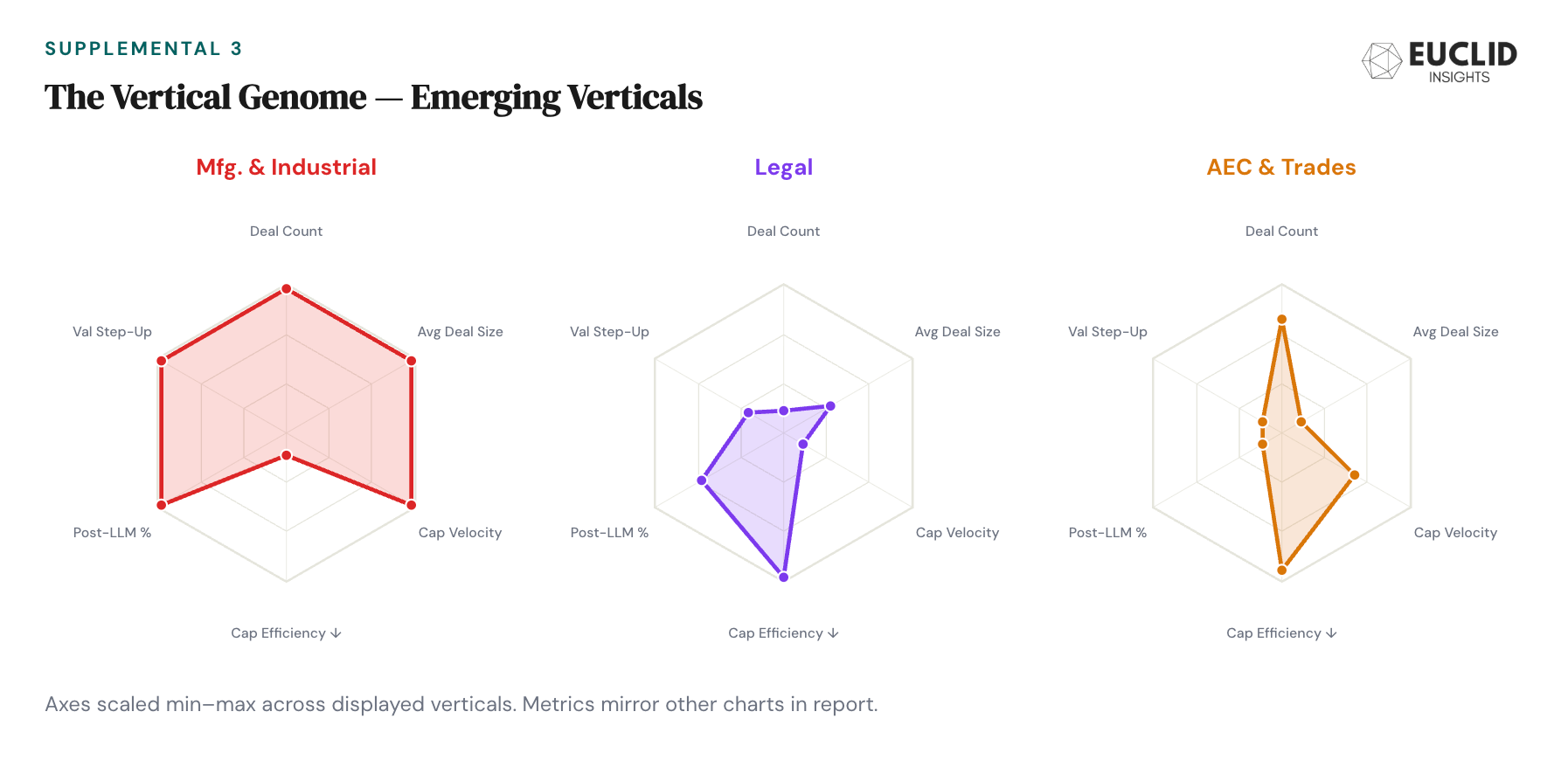

The $30M+ and $100M+ tiers are where vertical differences sharpen. Financial Services had the highest $30M+ share at 16%, reflecting a deep bench of growth-stage fintech companies. Legal’s 9% $100M+ share—the highest outside of Financial Services—reflects outsized Clio and Filevine rounds. AEC & Trades showed an unusual distribution: 42% of deals fell in the $5–15M bucket (the highest of any vertical), suggesting the category may be moving beyond the earliest stages of vertical AI formation and into more mainstream legibility.

One of the most telling stage signals is the “newness” of each vertical’s company base. We looked at the share of funded companies founded in 2022 or later—the post-ChatGPT cohort. Manufacturing leads at 57%, followed by Public Sector (56%) and Legal (53%). These are verticals where generative AI created net-new startup formation, not just incremental improvement to existing companies. The cross-market baseline sits at roughly 46%, meaning these three verticals have meaningfully higher shares of post-ChatGPT companies than the broader market.

The deal size distribution also reveals which verticals have deep, multi-layered ecosystems versus those still in their earliest innings. Healthcare’s balanced profile (38/31/15/13/3) is the hallmark of a mature vertical with companies at every lifecycle phase. Financial Services is similarly broad, with the highest $30M+ concentration (21%) of any major vertical—the fintech wave of 2019–2021 produced companies now reaching growth stage. Conversely, Real Estate’s 51% concentration at $1–5M and 0% at $100M+ signals a vertical still in early formation: lots of new entrants, few scaled incumbents.

The quarterly stage data surfaces one additional insight: the $100M+ tier grew from 39 deals in Q1 to 55 in Q2 and held at that level through year-end. This suggests that mega-round activity—often viewed as frothy—actually reflected persistent demand at the growth stage, driven in part by sovereign wealth funds, asset managers, and crossover investors entering AI for the first time. The smaller deal tiers, by contrast, showed more cyclical behavior, with the $1–5M bucket declining 28% from Q1 to Q4.

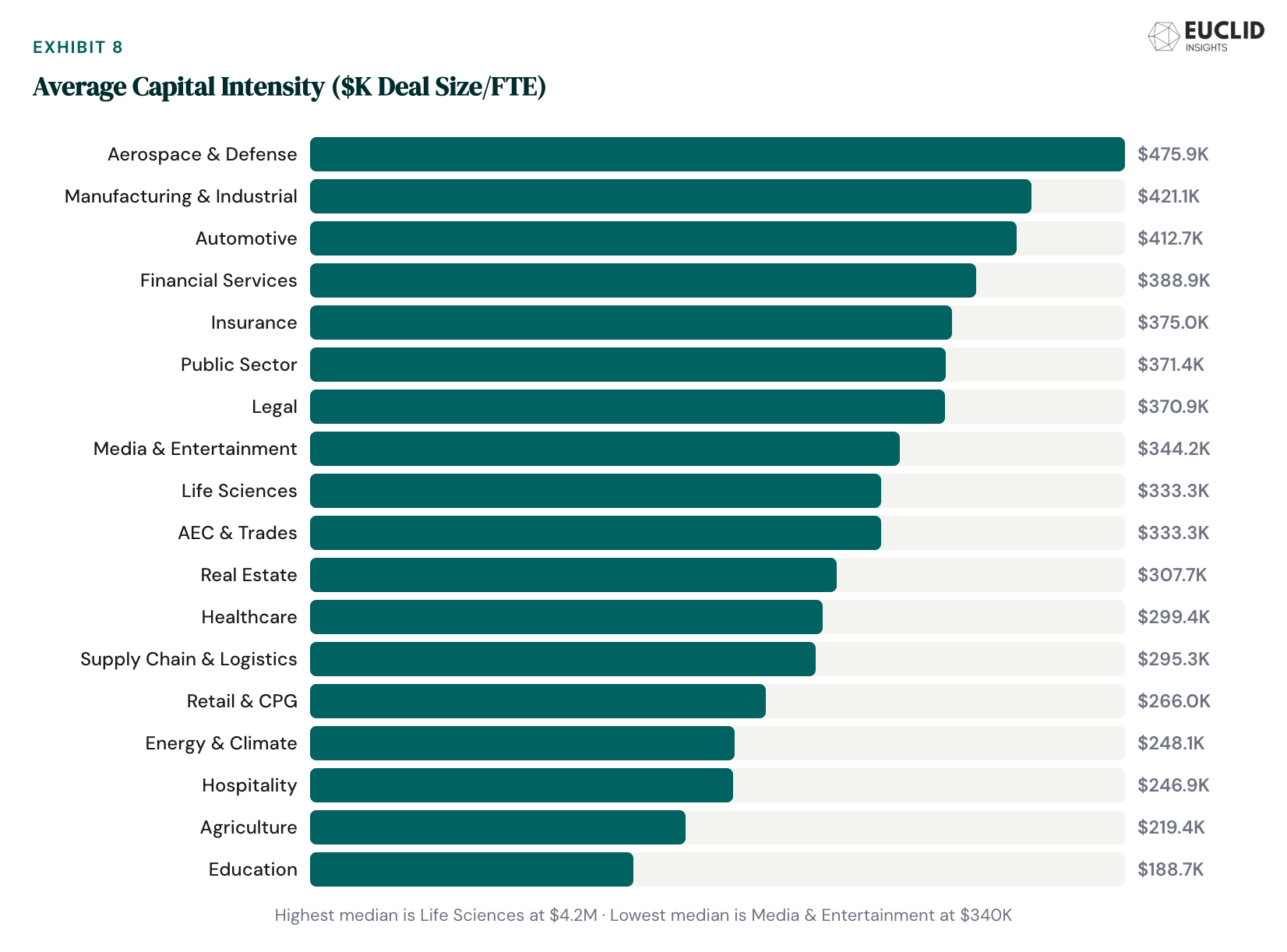

A few additional analyses help us shed light on how vertical companies deploy capital across sectors and stages. Looking at average deal size per employee (FTE)—a proxy for capital intensity—Aerospace & Defense leads ($476K), reflecting the R&D-heavy nature of the category. Manufacturing & Industrial follows at $421K, consistent with the physical-world infrastructure requirements of industrial AI. Education, raising on average less than $200K per employee in 2025 rounds, was the leanest, consistent with its lighter distribution model and lower customer acquisition costs (and perhaps also speaking to lower investor demand, despite great rounds from breakouts MagicSchool and SchoolAI).

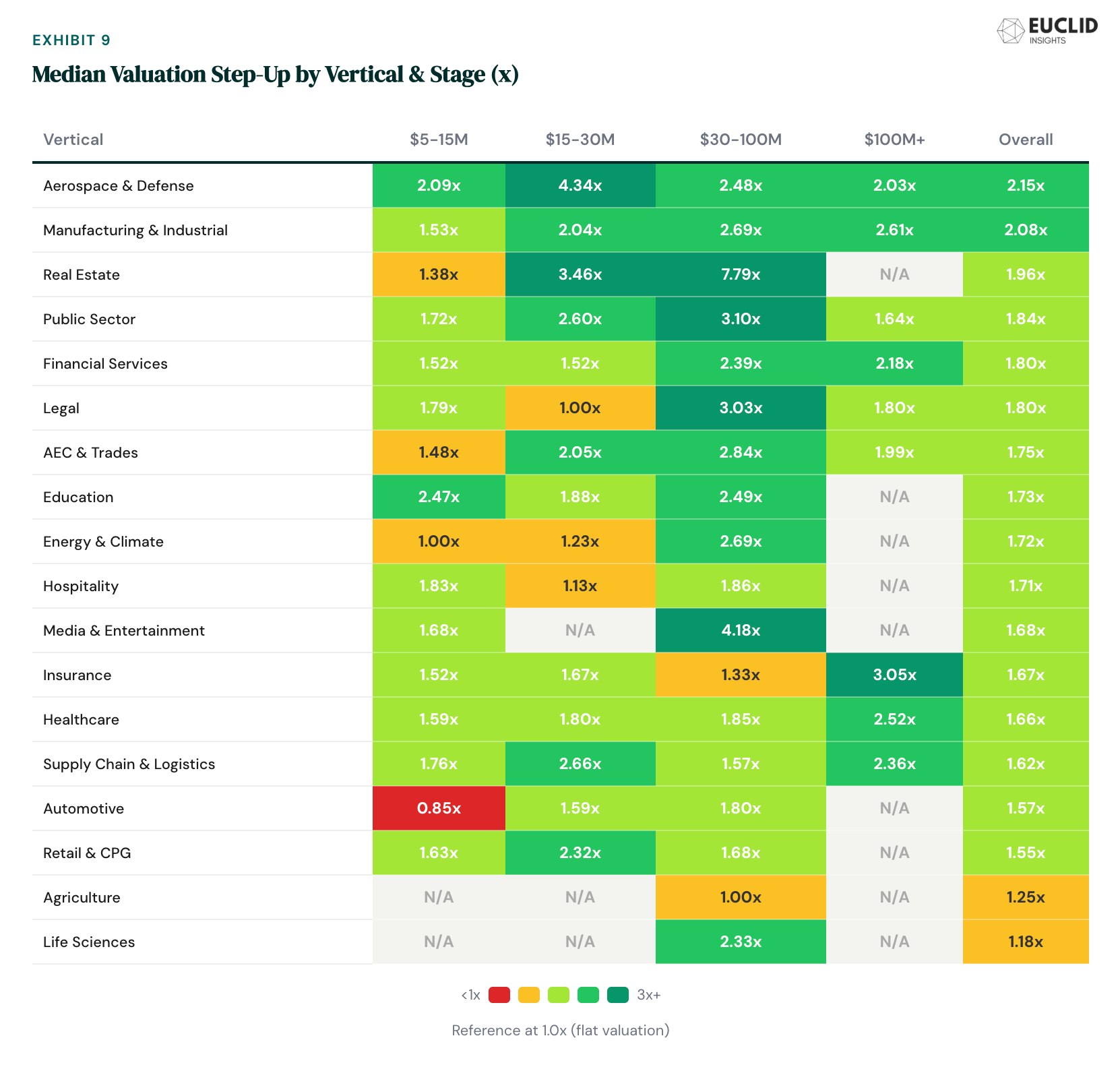

Median valuation step-ups—the post-money markup from one round to the next—reveal which verticals command the strongest investor conviction. Aerospace & Defense leads overall at 2.15x, followed by Manufacturing at 2.08x and Real Estate at 1.96x. At the early stage ($5–15M tier specifically), Education shows the highest step-up at 2.5x. Financial Services, despite attracting the most capital, shows a more modest overall step-up at 1.80x—suggesting that larger round sizes dilute the per-round markup even as total value creation remains strong.

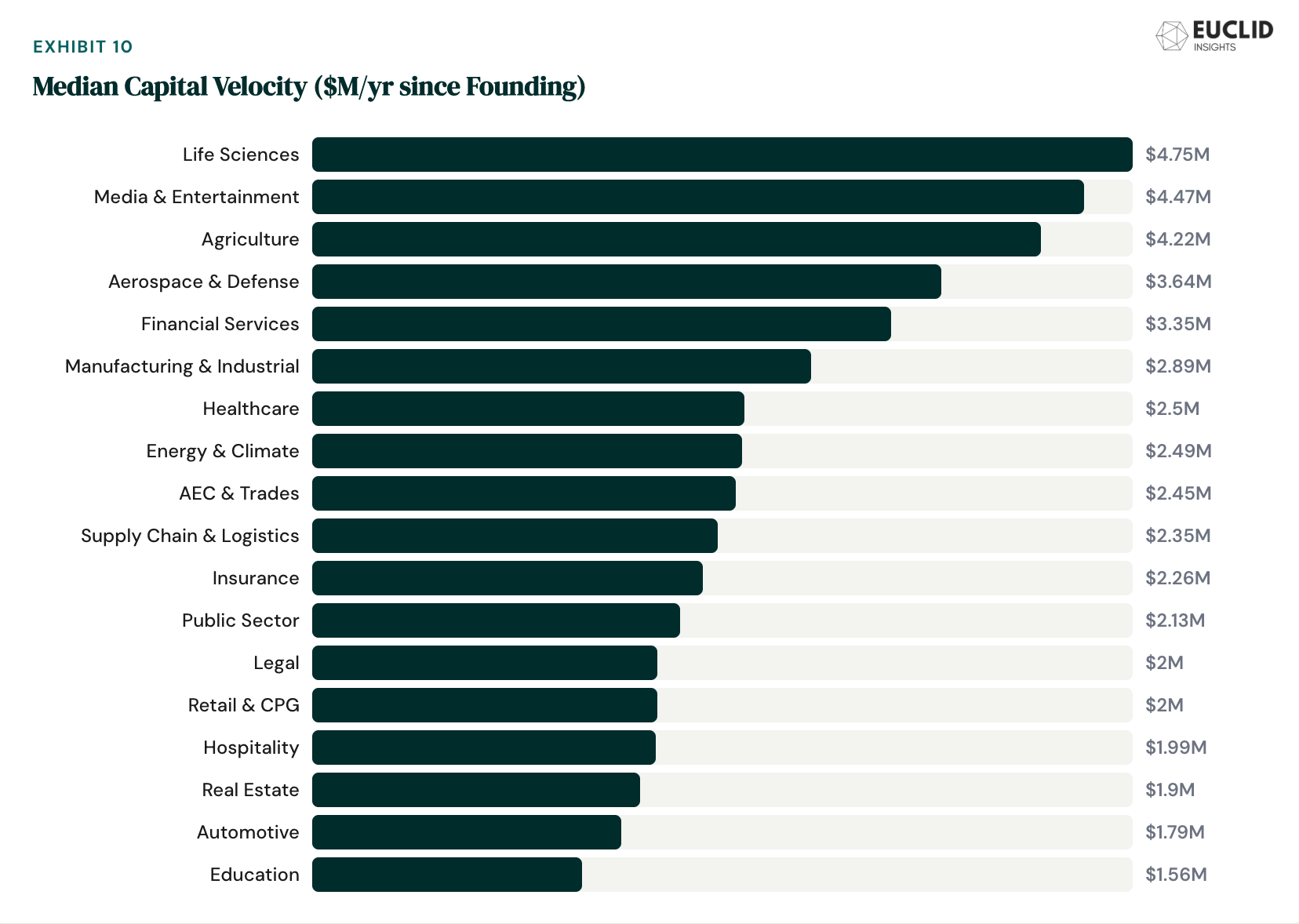

Capital velocity—measured here by median dollars raised per year since founding—aims to capture the appetite for capital vertical startups demonstrate as they scale. Life Sciences, unsurprisingly, leads at $4.8M per year. Closely following—perhaps somewhat counter-intuitively—are Media & Entertainment at $4.5M and Agriculture at $4.2M. Education trails at $1.6M, consistent with its smaller round sizes and more measured growth trajectories.

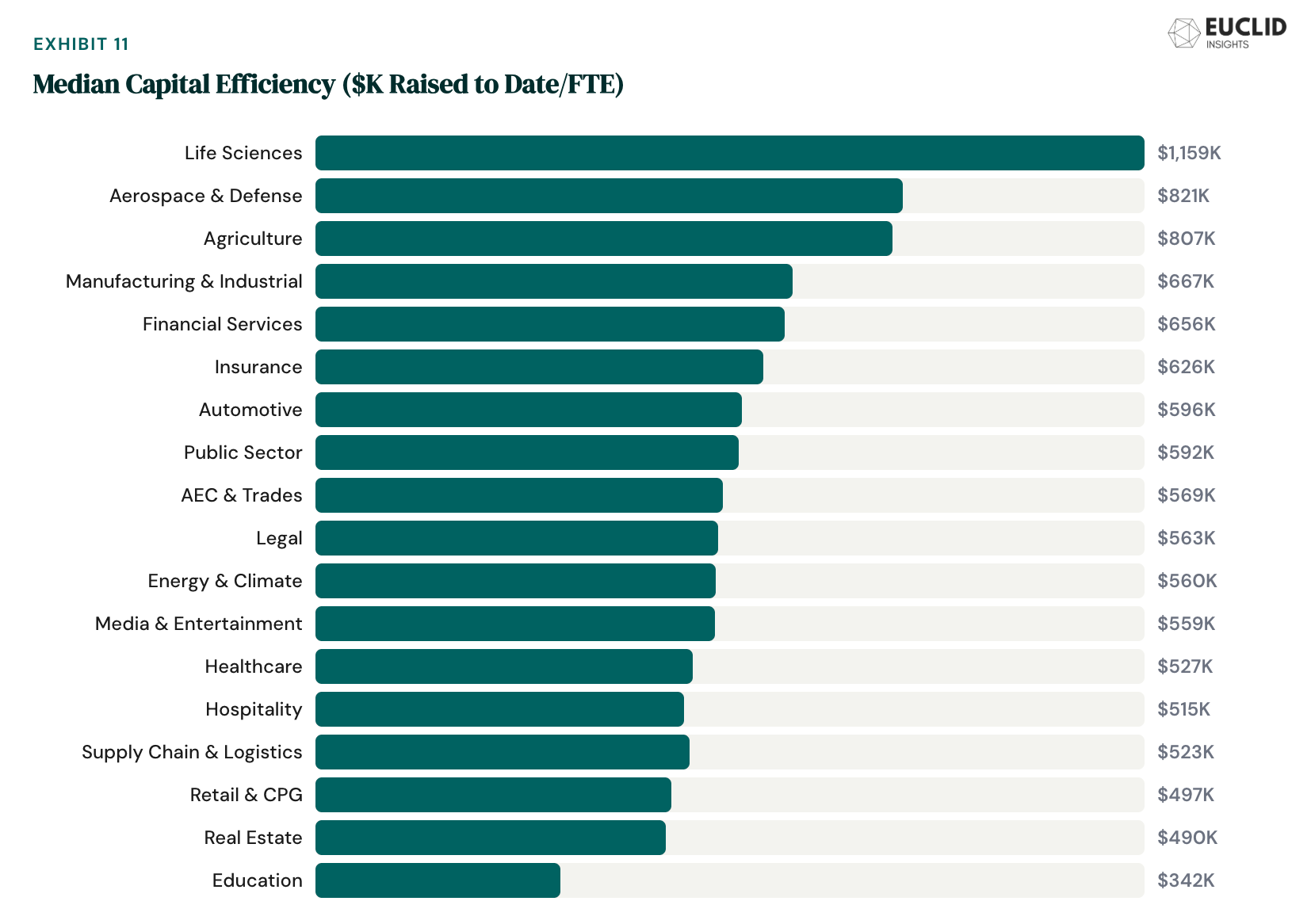

Capital Efficiency—measured here by median dollars raised per year FTE—captures how much leverage a business has created on its financing to date. While imperfect—given it does not capture the ebbs and flows of spend over time—we can see that Life Sciences dominates, with A&D and Agriculture a close 2nd / 3rd. In comparison to Capital Intensity, this suggests greater investment requirements over time rather than immediate investor demand. As with both Velocity and Intensity, Education trails at just $342K raised per employee.

IV. Momentum: Stage-Level Trends

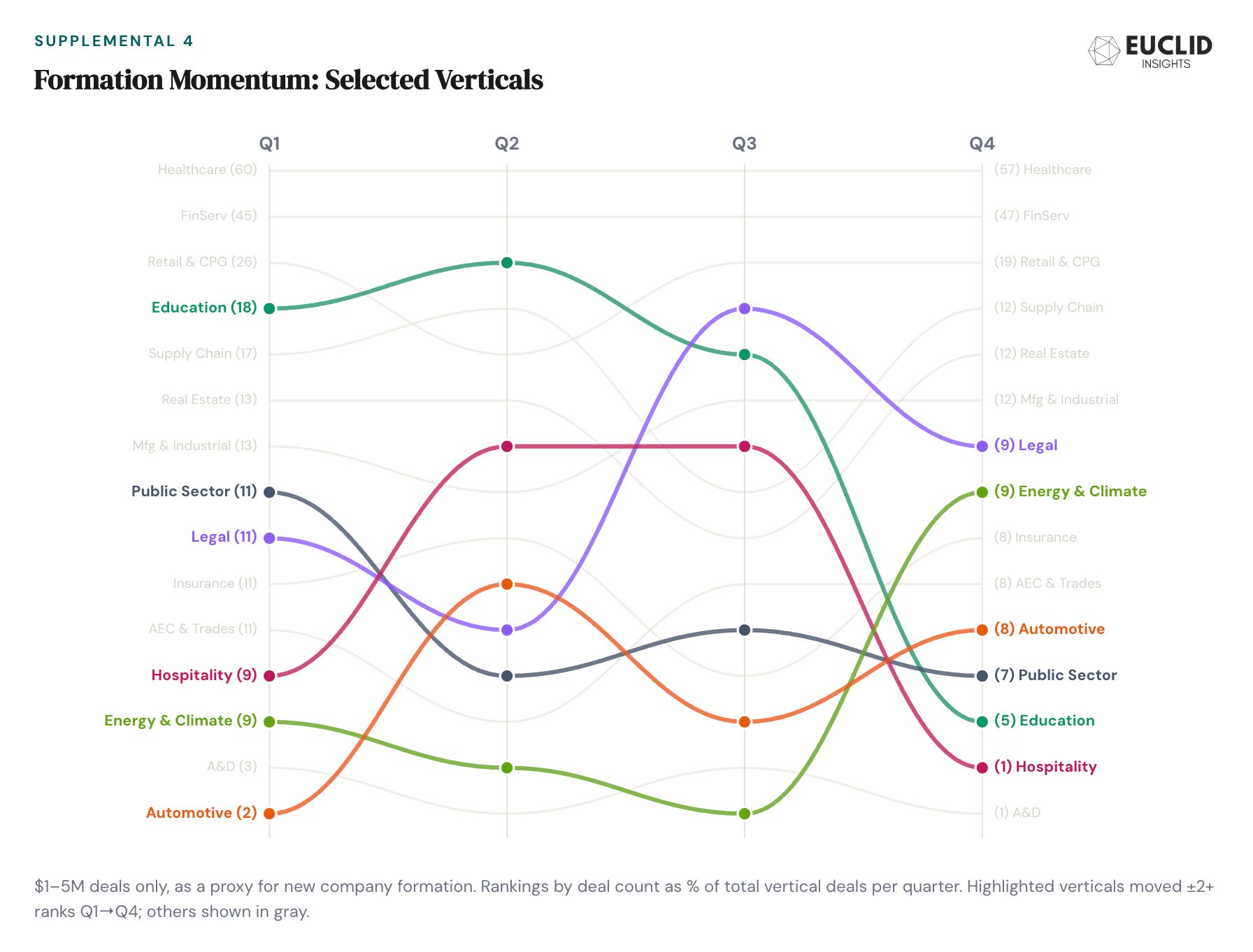

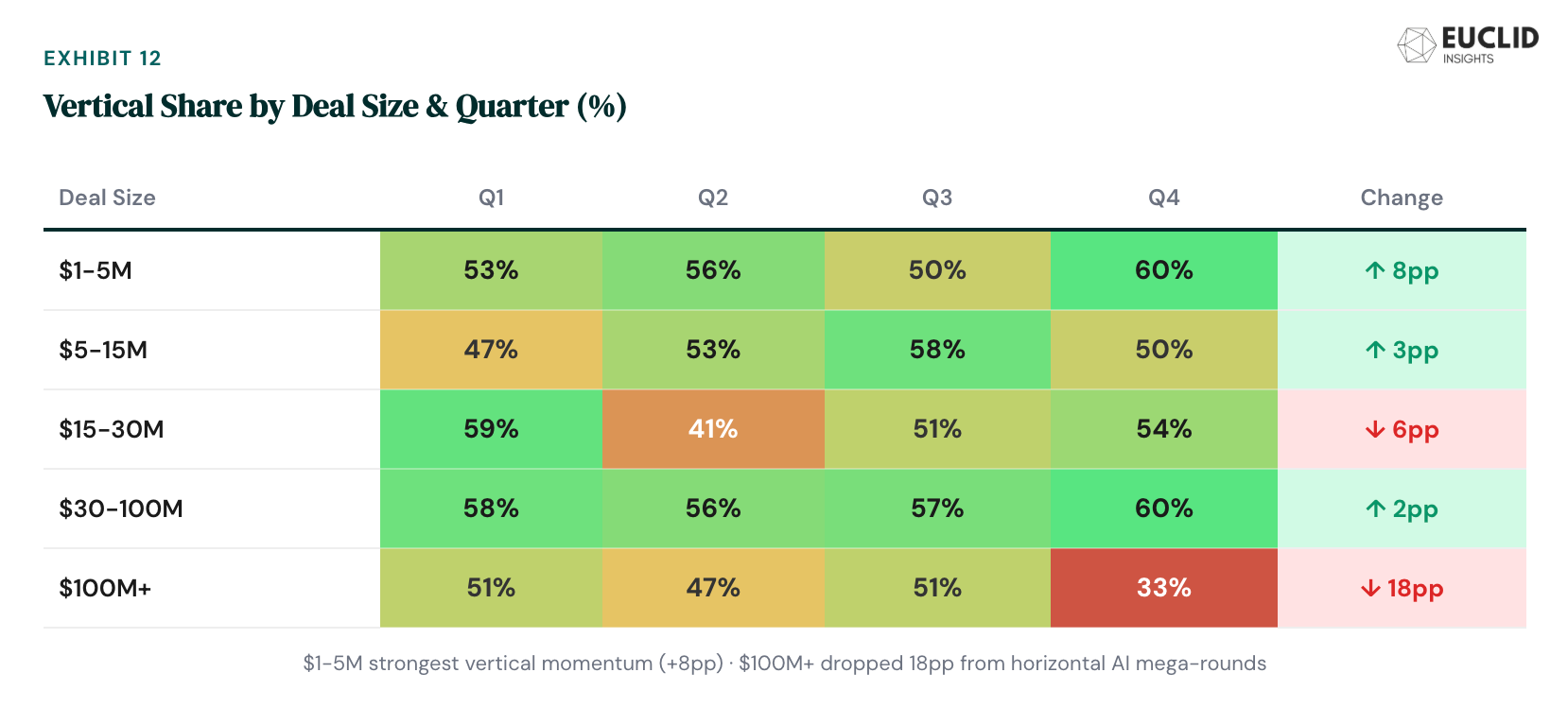

While the aggregate vertical share—53% of deals, 30% of capital—is a useful headline, we wanted to drill down into comparative dynamics at the stage level. By segmenting deals into five size buckets ($1–5M, $5–15M, $15–30M, $30M+, $100M+) and tracking vertical share by quarter, a more nuanced picture emerges: vertical AI has decisive early-stage and Series A / B momentum, but has yet to generate the volume of mega-deals that allow it to consistently maintain parity with horizontal at growth.

The $1–5M tier—the domain of pre-seed and seed—showed the strongest vertical momentum of any bucket. Vertical share rose from 53% in Q1 to 60% in Q4, an 8-percentage-point gain that represents the most significant forward-looking signal in this dataset. When three out of five new venture-backed companies are building for a specific industry, it says something about where founders see opportunity. The post-ChatGPT generation is not building general-purpose tools—they are building AI for healthcare, legal, construction, manufacturing, and logistics.

Moving to seed / Series A: the $5–15M tier ranged from 47% in Q1 to 58% in Q3, while $30M+ held between 56% (Q2) and 60% (Q4). Neither showed a clear directional trend. This stability suggests that once vertical companies graduate to their $5–15M+ round, the competitive dynamics at that stage are relatively balanced between vertical and horizontal players. The $15–30M tier was comparatively volatile—59% vertical in Q1, dropping to 41% in Q2, then recovering to 54% in Q4. The Q2 dip likely reflects a burst of horizontal AI activity versus any sort of vertical pullback.

The most striking divergence was at $100M+. Vertical share fell from 51%, an 18-percentage-point swing that represents the only bucket where non-vertical companies decisively overtook vertical during the year. This is almost entirely explained by the concentration of mega-rounds in foundation model companies, horizontal AI platforms (OpenAI, Anthropic, xAI, Databricks), and infrastructure providers that raised capital-intensive rounds in the back half of 2025. At every other tier, vertical maintained or expanded its lead.

Our momentum data produces a clean narrative: vertical making leaps and bounds at formation ($1–5M), holding steady through the scaling stages ($5–30M), and ceding ground only at the mega-round level ($100M+) where the magnitude of horizontal AI raises distorts the picture. For investors focused on the next cycle, the $1–5M signal is the one that matters most—if it takes 5–7 years for an early-stage cohort to reach maturity, the companies being formed today will define the vertical AI landscape of 2030–2032. We expect 2026 to be another year of prolific vertical AI formation.

V. Financing Highlights

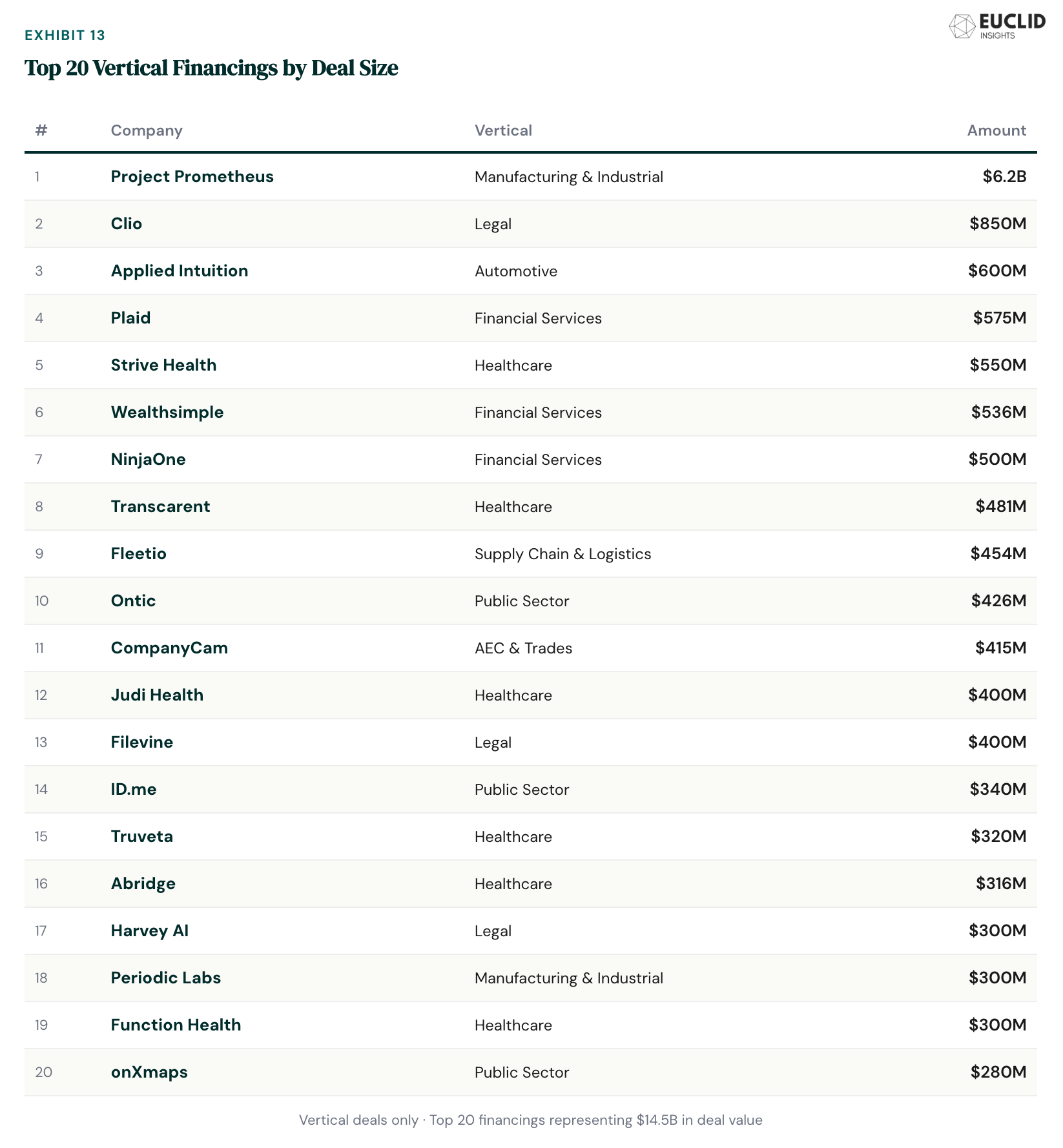

Below, we pull out 15 highlights of vertical businesses that raised in 2025—we selected some from the biggest deals above, and mix in others we think are most interesting. Our profiles range in deal size from $190M (Peregrine) to by far the biggest deal at $6.2B (Project Prometheus). Healthcare dominated the list with five companies (in line with its 30% share of the top 20). Legal and Manufacturing & Industrial also placed multiple highlights. Five of the fifteen are first or second rounds, suggesting that new company formation at massive scale is accelerating in verticals where the AI opportunity is freshly legible. Here are the deals we found most revealing, and characteristic of 2025:

Project Prometheus — $6.2B (Mfg. & Industrial, Q4)

Jeff Bezos’s return to operational company-building made headlines, but the thesis is what matters: “physical AI” for manufacturing, targeting chip packaging, automotive assembly, and aerospace operations. Co-CEO Vik Bajaj brings a career that spans Google Life Sciences (now Verily), GRAIL, and Foresite Capital—an unusual background that fuses deep science with operational scale. The team has pulled over 100 hires from DeepMind, Tesla, and OpenAI. At $6.2B, this is the largest-ever first financing for a vertical AI company—and it’s not close. It’s larger than the next four deals on this list combined. The round is a statement that the next wave of AI value creation will happen on factory floors, not in SaaS dashboards, and that the market for physical-world AI is large enough to justify deployment-stage capital before a single dollar of revenue.

Clio — $850M Series G (Legal, Q4)

Clio’s round ($500M equity + $350M debt) funded the simultaneous $1B acquisition of legal research platform vLex, creating an end-to-end research-to-operations platform at a $5B valuation. Founded in 2007 by Jack Newton and Rian Gauvreau, Clio was the first to commercialize cloud-based law practice management when on-premises systems dominated. The combined deal represents both the largest legal tech financing and the largest legal tech M&A transaction in history. What stands out in the data: at 5x revenue and a 1.38x step-up from its prior round, this is a mature, capital-efficient business using leverage strategically—the $350M debt component signals confidence in predictable cash flows. With 1,672 employees and 17 years of compounding, Clio is the anti-hype case study: a vertical SaaS company that defined its category long before AI became a funding catalyst, and is now using AI-era capital to consolidate it. NEA’s Tony Florence led the round alongside Goldman Sachs, TCV, Sixth Street, and JMI Equity.

NinjaOne — $500M Series C Extension (ITSM, Q1)

NinjaOne’s $500M Series C extension at a $5B valuation—a 2.37x step-up from $1.9B just twelve months prior—is the kind of round that reveals the power of vertical focus in what looks like a horizontal market. Co-founded in 2013 by childhood friends Sal Sferlazza and Chris Matarese, the company built a cloud-native endpoint management platform for IT teams and MSPs at a time when incumbents like Kaseya and ConnectWise were running on legacy architectures. The raise, led by ICONIQ Growth and CapitalG (Alphabet‘s investment arm), also funded the $262M acquisition of SaaS backup leader Dropsuite—a buy-and-build move that mirrors Clio’s consolidation strategy. Notable in the data: NinjaOne is one of only two companies on this list based in the South (alongside Fleetio in Birmingham), it has zero debt, and it remains founder-led and controlled. With over 35,000 customers across 140+ countries and 2,000 employees, this is a vertical platform executing a horizontal expansion playbook.

Fleetio — $454M Series D (Supply Chain & Logistics, Q1)

Fleetio’s $454M Series D—co-led by existing investor Elephant Partners and new investor Goldman Sachs Growth Equity—valued the combined business at over $1.5B and funded the simultaneous acquisition of Auto Integrate, the premier maintenance authorization platform in North America. The combined entity now services over 8 million vehicles and processes more than 13 million repair orders per year through 110,000+ repair shops. Fleetio was founded in 2012 in Birmingham, Alabama by Tony Summerville, with CEO Jon Meachin (Brown undergrad, Morgan Stanley and Parthenon Capital alum) running the business. This deal stands out for its 2.36x step-up and the sheer physical scale of the network it acquired. While most vertical AI companies on this list are primarily selling software or AI, Fleetio is building a two-sided marketplace for fleet maintenance—a structural asset that gets harder to replicate with every shop that joins the network.

CompanyCam — $415M Series C (AEC & Trades, Q3)

CompanyCam is a story of pure founder-market fit. Luke Hansen built the platform out of his family’s roofing business in Lincoln, Nebraska, solving the problem of photo documentation and job site coordination for contractors. The $415M round from B Capital valued the company at $1.99B—Nebraska’s first-ever unicorn. At a 3.21x step-up, this is one of the highest valuation jumps on the list, suggesting rapid revenue acceleration. The investor roster reads like a conviction trade: Insight Partners, JMI Equity, WndrCo, and Blueprint Equity all participated alongside B Capital. CompanyCam represents the broader AEC thesis—fragmented industries with low tech adoption, where mobile-first AI tools can compress workflows that previously ran on clipboards and phone calls. With 308 employees, it’s also one of the leanest companies on the list relative to its valuation, implying strong unit economics.

Filevine — $400M Series F (Legal, Q3)

Filevine’s $400M Series F at a $5.25B valuation makes legal tech the only vertical to place two companies in the top six deals of 2025. Co-founded in 2014 by Nathan Morris, Filevine provides case management and workflow automation software for law firms, with a particular strength in litigation and personal injury practices. Accel and Insight Partners co-led the round alongside The Halo Fund. The 1.74x step-up is more modest than CompanyCam‘s or Ambience’s, but the absolute valuation—$5.25B on its 8th round—places it alongside Clio as proof that legal tech has matured from a niche into a major vertical software category. The deal is also notable for its investor composition: Meritech Capital, StepStone Group, and Album VC joined, bringing a mix of crossover and institutional capital that typically signals pre-IPO positioning. With 700 employees in Salt Lake City, Filevine is a reminder that vertical unicorns don’t have to be in San Francisco.

Abridge — $316M Series E (Healthcare, Q2)

Abridge raised its Series E just four months after a $250M Series D, reaching a $5.3B valuation with an implied EV/Revenue multiple north of 697x. CEO Shivdev Rao is a practicing cardiologist who co-founded the company with CMU researchers Florian Metze and Sandeep Konam. The platform transcribes and summarizes clinical conversations, producing documentation, patient summaries, and educational content. Andreessen Horowitz led the round alongside Khosla Ventures, WndrCo, and newcomers Archerman Capital and the California Health Care Foundation. What stands out: the 0.35-year gap between rounds is the shortest on the list, suggesting either extraordinary growth or a competitive capital raise intended to lock out competitors like Ambience Healthcare. At $7.60M in revenue and 488 employees, Abridge’s sky-high multiple reflects the market’s belief that clinical AI documentation is a winner-take-most category—and the willingness to fund the race at nearly any price.

Periodic Labs — $300M Seed (Mfg. & Industrial, Q3)

Periodic Labs emerged from stealth with what may be the largest seed round in history—$300M led by Andreessen Horowitz at a $1.3B pre-money valuation. Co-founded by Liam Fedus, a former VP of Research at OpenAI who co-created ChatGPT, and Ekin Dogus Cubuk, who led the materials and chemistry team at Google DeepMind (including the GNoME project that discovered 2 million new crystals), the company is building “AI scientists” paired with autonomous robotic laboratories. The investor list reads like a tech hall of fame: Jeff Bezos, Eric Schmidt, Jeff Dean, Elad Gil, NVIDIA’s NVentures, Accel, DST Global, Felicis, and more. The thesis is that the internet’s text corpus is exhausted as training data; the next frontier is proprietary experimental data generated by AI running physical experiments. Periodic is targeting superconductors first, with early commercial work on chip heat dissipation for a semiconductor manufacturer. Among the 15 deals, this is the most audacious bet on founder pedigree over business traction—a $300M check written on a company founded in 2025 with no revenue and roughly 100 employees.

Ambience — $243M Series C (Healthcare, Q3)

Ambience Healthcare’s $243M Series C at a $1.25B valuation represents a 3.47x step-up—the second-highest on this list behind Peregrine‘s 6.58x. Co-founded in 2020 by Michael Ng (MIT Sloan, ex-Morgan Stanley, ex-Calera Capital), Ambience builds an AI-powered medical scribe that captures clinician-patient conversations and generates clinical notes in real-time, embedded directly into EHR workflows. Andreessen Horowitz’s Julie Yoo and Oak HC/FT‘s Vignesh Chandramouli co-led the round, alongside a deep healthcare-specialist syndicate: Sequoia, Kleiner Perkins, General Catalyst, OpenAI Startup Fund, and Optum Ventures. This is one of two clinical documentation companies on the list (alongside Abridge), highlighting the intensity of competition in a category where switching costs are high and health system contracts are sticky. At 200 employees and four years old, Ambience is executing a faster land-and-expand playbook than Abridge, with institutional health system partnerships as its primary channel.

Forterra — $238M Series C (Aerospace & Defense, Q4)

Forterra’s $238M Series C, led by Moore Strategic Ventures, positions the company as the leading autonomous ground vehicle platform for U.S. defense. Originally founded as Robotic Research in 2002 by Alberto Lacaze, the company rebranded under CEO Josh Araujo (ex-Jefferies, ex-Lazard, ex-USMC infantry officer). Forterra builds self-driving military land systems and robotic swarm coordination platforms. The round came on the heels of a landmark streak of government contracts: the first-ever DoD ground autonomy production contract (ROGUE Fires with the Marine Corps), a $114M prime contract for autonomous breaching systems, and the Army’s GEARS and UxS programs. Forterra also acquired tactical mesh networking company goTenna, adding a communications layer to its autonomy stack. Among the 15 deals, Forterra is the oldest company by founding date (2002) and the most evolved from a business-model standpoint—it has real production contracts and program-of-record revenue, not just R&D grants. The investor syndicate (Salesforce Ventures, Franklin Templeton, Hanwha Asset Management, NightDragon) reflects the growing crossover between defense tech and institutional capital.

Teamworks — $235M Series F (Media & Ent., Q2)

Teamworks’ $235M oversubscribed Series F, led by returning investor Dragoneer, pushed the company past a $1B pre-money valuation—minting a unicorn in the sports technology vertical. Founded in 2004 by Zach Maurides, a Duke offensive lineman who built the first version as a sophomore-year class project to manage his own chaotic practice schedule, Teamworks has grown into what it calls “the Operating System for Sports,” powering over 6,500 elite teams globally across professional leagues, NCAA programs, Olympic sports, and military organizations. The round is a combination of primary and secondary capital. What makes Teamworks unusual on this list is its acquisition-driven expansion: the company has completed 13 acquisitions (nine in the past three years alone), including INFLCR (NIL content), ARMS Software (compliance), Smartabase (performance), Zelus Analytics (predictive intelligence), Telemetry Sports (computer vision for football, used by 80% of NFL teams), Opteamal (athlete monitoring), and most recently Sportlogiq (AI-powered hockey analytics, used by 97% of NHL teams). The Sportlogiq deal alone brought 80 employees and 10 AI researchers with 180+ published papers. This is a roll-up strategy executed with venture capital rather than private equity—rare in vertical SaaS. At ~450 employees across 11 countries and headquartered in Durham, NC, Teamworks is a textbook founder-market-fit story: Maurides understood the coordination problem in athletics from the inside and has spent two decades compounding that insight into a platform that spans talent acquisition, player development, game preparation, and operations. The $411M raised to date and Series F stage also make it one of the most mature businesses on this list.

Lila Sciences — $235M Series A (Life Sciences, Q3)

Lila Sciences’ $235M Series A (part of a broader $350M close that brought total funding to $550M) valued the company at $1.26B and represents the second “AI for science” bet on this list alongside Periodic Labs. Incubated at Flagship Pioneering—the venture studio behind Moderna—Lila was founded in 2023 by Geoffrey von Maltzahn, a Flagship General Partner with a PhD in biomedical engineering. Braidwell and Collective Global co-led, with NVIDIA‘s NVentures, In-Q-Tel (the CIA’s venture arm), Analog Devices, and institutional LPs including the Abu Dhabi Investment Authority and State of Michigan Retirement System participating. While Periodic Labs targets materials science through autonomous physical experiments, Lila is focused on life sciences and chemical discovery through what it calls “AI Science Factories”—autonomous lab facilities where AI agents design, execute, and iterate on experiments. In-Q-Tel’s participation signals national security interest in accelerating materials discovery for computing, energy, and infrastructure. At 195 employees, Lila has demonstrated early results including novel protein therapeutics, green hydrogen catalysts, and carbon capture sorbents.

OpenEvidence — $210M Series B (Healthcare, Q3)

We would have included OpenEvidence’s $210M Series B at $3.5B valuation on this list even if it hadn’t more than tripled its valuation with further raises in the interim. Founded in 2017 by Daniel Nadler—whose previous company Kensho was acquired by S&P Global for $700M in 2018—OpenEvidence built an AI-powered medical search engine that has been adopted by over 40% of U.S. physicians, processing 8.5 million consultations per month. Google Ventures and Kleiner Perkins (with Chairman John Doerr personally involved) co-led; Sequoia, Coatue, Conviction, and Thrive followed on. The data tells the story: at a 35x EV/Revenue multiple on $100M of revenue, this is the most capital-efficient company on the list by a wide margin. Its implied valuation-to-revenue of 35x compares to Abridge‘s 697x. The 3.35x step-up and a mere 36 employees make OpenEvidence the leanest operation here—fewer than one-fifth the headcount of most peers. The freemium model (free for verified physicians, monetized through advertising) bypassed traditional enterprise healthcare sales cycles entirely. Nadler’s TIME100 Health recognition and partnerships with the AMA, NEJM, and JAMA Network suggest a platform with both distribution and credibility moats. With only 0.4 years between its Series A and B, OpenEvidence is on a trajectory that has since seen it raise a $200M Series C at $6B and a $250M Series D at $12B.

Commure — $200M Series E (Healthcare, Q2)

Commure’s $200M Series E, led by General Catalyst, is the infrastructure play in an otherwise application-heavy healthcare contingent. Co-founded in 2017 by Tanay Tandon, Commure builds an interoperable data platform that unifies fragmented healthcare datasets—an integration layer that sits beneath the clinical applications companies like Abridge and Ambience are building on top. This is Commure‘s 9th round and the data shows a raised-to-date figure of $2.1B—by far the most cumulative capital of any healthcare company on this list. The 0.47-year gap between rounds suggests continuous capital deployment. With 492 employees in Mountain View, Commure occupies a different strategic position than the clinical AI documentation companies: it’s a platform bet on healthcare data infrastructure rather than a point-solution bet on any single clinical workflow. General Catalyst‘s Pranav Singhvi led alongside LTS Growth, Maverick Ventures Israel, and Shasta Ventures.

Peregrine — $190M Series C (Public Sector, Q1)

Peregrine’s $190M Series C, led by Sequoia Capital‘s Andrew Reed, valued the company at $2.56B—a staggering 6.58x step-up, the highest on this list by a factor of two. Co-founded in 2018 by Nick Noone, a former Palantir executive who headed the U.S. Special Operations (SOCOM) business unit, Peregrine builds a data intelligence platform for law enforcement and public safety agencies. The company was built while embedded inside the San Pablo Police Department, and its platform was deployed for Super Bowl LIX security coordination in New Orleans. The growth metrics are striking: revenue reportedly tripled from $3M to $10M in 2023, then tripled again to $30M in 2024. Agencies using the platform have reported measurable outcomes—a 40% decrease in open homicide cases in Albuquerque, a 21% reduction in violent crime in Atlanta. At 311 employees and just $63M raised prior to this round, Peregrine‘s capital efficiency is notable. The 6.6x step-up reflects both the growth rate and the scarcity premium of govtech companies that can actually land and expand across fragmented municipal and state agencies. Peregrine is the only public sector company on this list, and the only one with Palantir DNA in its founding team.

Themes Across the Top Deals

Four patterns recur across the year’s most notable financings. First, the convergence of AI and physical-world operations: Project Prometheus, Periodic Labs, Lila Sciences, Forterra, CompanyCam, and Fleetio all apply AI to industries where the value sits in atoms, not just bits: factory floors, autonomous ground vehicles, robotic labs, or repair shop networks. Physical-world companies account for a substantial share of the list.

Second, these highlights underscore the power of vertical founder-market fit. Shivdev Rao (cardiologist building clinical AI), Luke Hansen (roofer building construction tech), Jack Newton (17 years building legal tech), Zach Maurides (Duke offensive lineman building sports operations tech), Nick Noone (Palantir SOCOM lead building public safety tech)—most successful vertical AI companies are led by people who understand the industry’s workflows from the inside, or who bring a directly transferable prior success.

Third, the capital advantage of category creation: companies with a strong claim to dominating a core function or major segment within their vertical—Clio and Filevine in legal, Abridge and Ambience in clinical documentation, OpenEvidence in medical search, Peregrine in public safety intelligence—attract capital on fundamentally different terms than companies competing in crowded horizontals. Multiple deals on this list feature step-ups above 3x, a signal that investors are paying for category leadership and the expansive terminal value that can accompany it.

Fourth, a new theme emerged in 2025: the AI-for-science mega-round. Periodic Labs ($300M seed) and Lila Sciences ($235M Series A) represent a conviction that the next source of valuable AI training data isn’t the internet—it’s proprietary experimental data generated by autonomous laboratories. Both companies raised at $1B+ valuations with minimal revenue, staking their cases entirely on team pedigree and the structural argument that physical-world data is the new moat. This is a category that didn’t exist on last year’s list, and it may define the next cycle.

VI. Exits

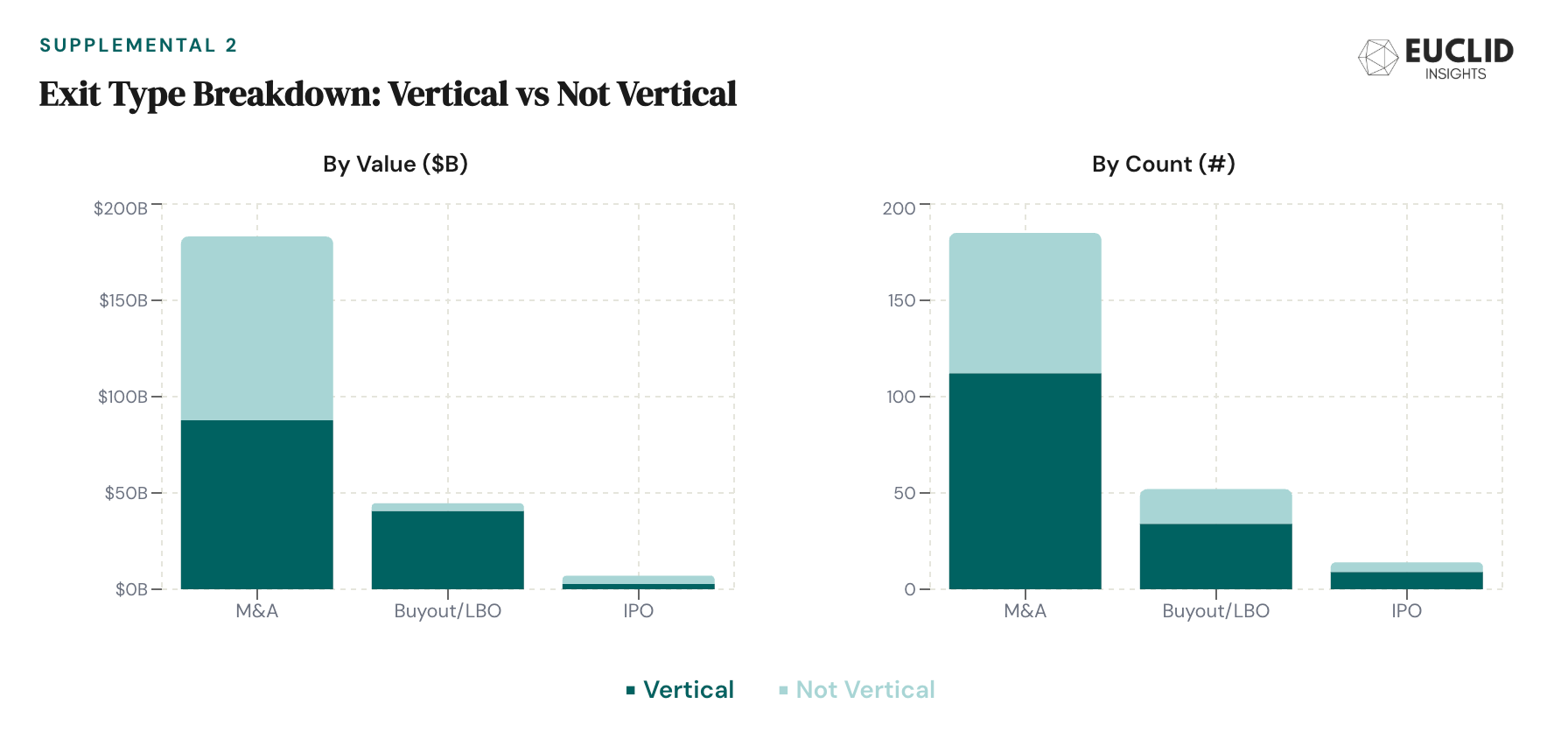

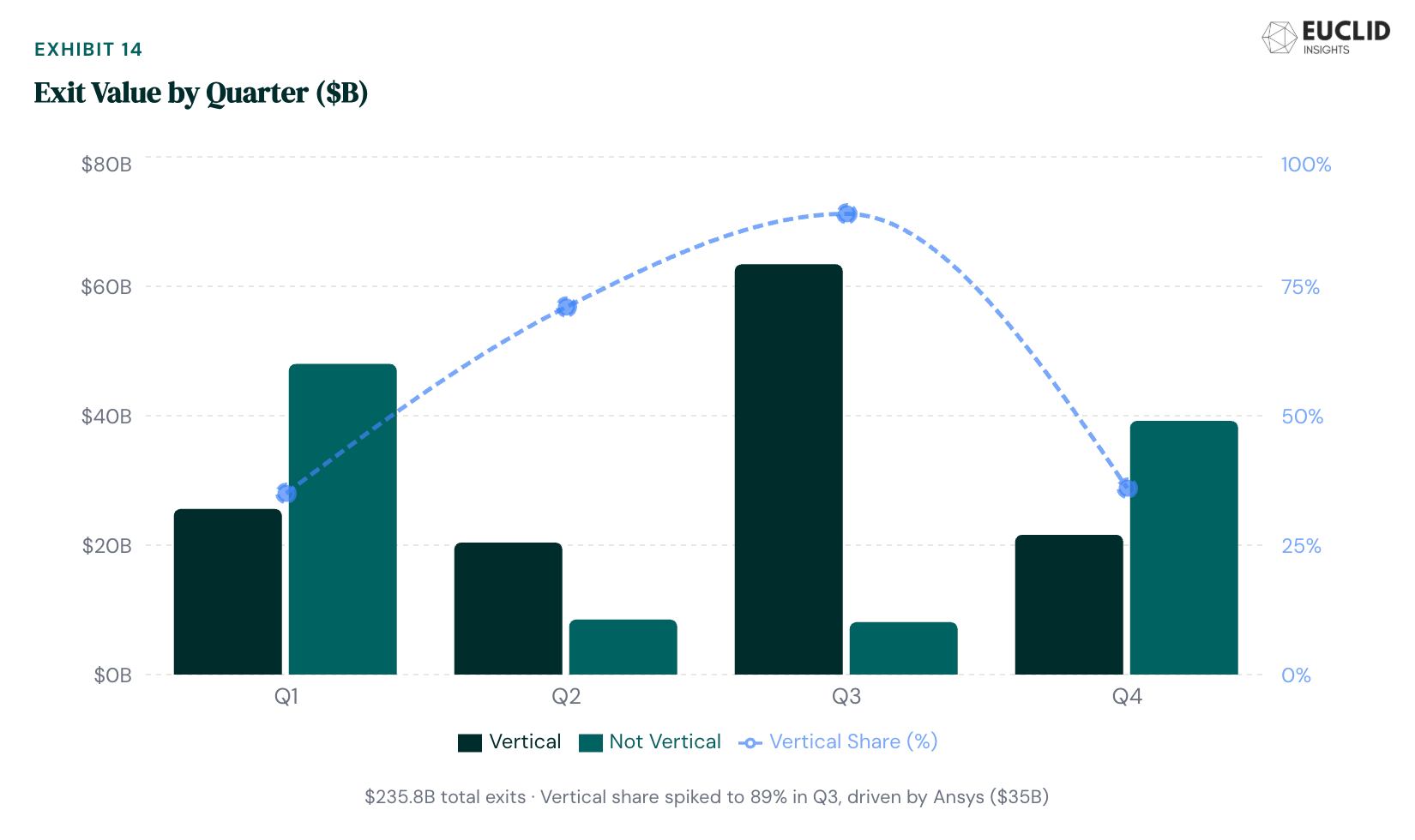

The 2025 exit market produced 158 vertical transactions worth $131B, headlined by Synopsys’s $35B acquisition of Ansys. While M&A dominated with nearly two-thirds of transactions by number, liquidity generated by the category ($89.4B) trailed Buyout/LBO ($90.0B) marginally. The year saw vertical 18 IPOs, composing $4.3B in aggregate deal value.

Including non-vertical exits, the total market was $235.8B across 254 transactions—vertical companies captured 56% of total exit value. Excluding Ansys, vertical share of value was 49%.

The quarterly pattern was uneven. Looking at all deals: Q1 produced the most exit value at $73.8B (thanks in large part to the X merger), while Q3 generated the highest exit count at 74 transactions. Q4’s combination of 54 exits and $60.8B in value included the Groq acquisition and several large PE buyouts, suggesting the exit environment was accelerating rather than cooling as the year ended. Vertical share over the course of the year was volatile by quarter, swung one way or another depending on mega-deals or lack thereof. Vertical had a dominant share in Q2 and Q3 (73%, 89%), while capturing barely over a third of value (35%, 36%) in Q1 and Q4.

Manufacturing & Industrial led exit value at $67.3B, driven by Ansys ($35B) and Altair Engineering ($10.5B). Healthcare generated the most exit activity with 43 transactions worth $17.1B, led by Modernizing Medicine ($5.3B), CentralReach ($1.9B), VaxCare ($1.7B), and Iodine Software ($1.3B). Financial Services contributed 25 exits worth $14.1B, led by NinjaTrader ($1.5B), Enfusion ($1.5B), and Hidden Road ($1.3B).

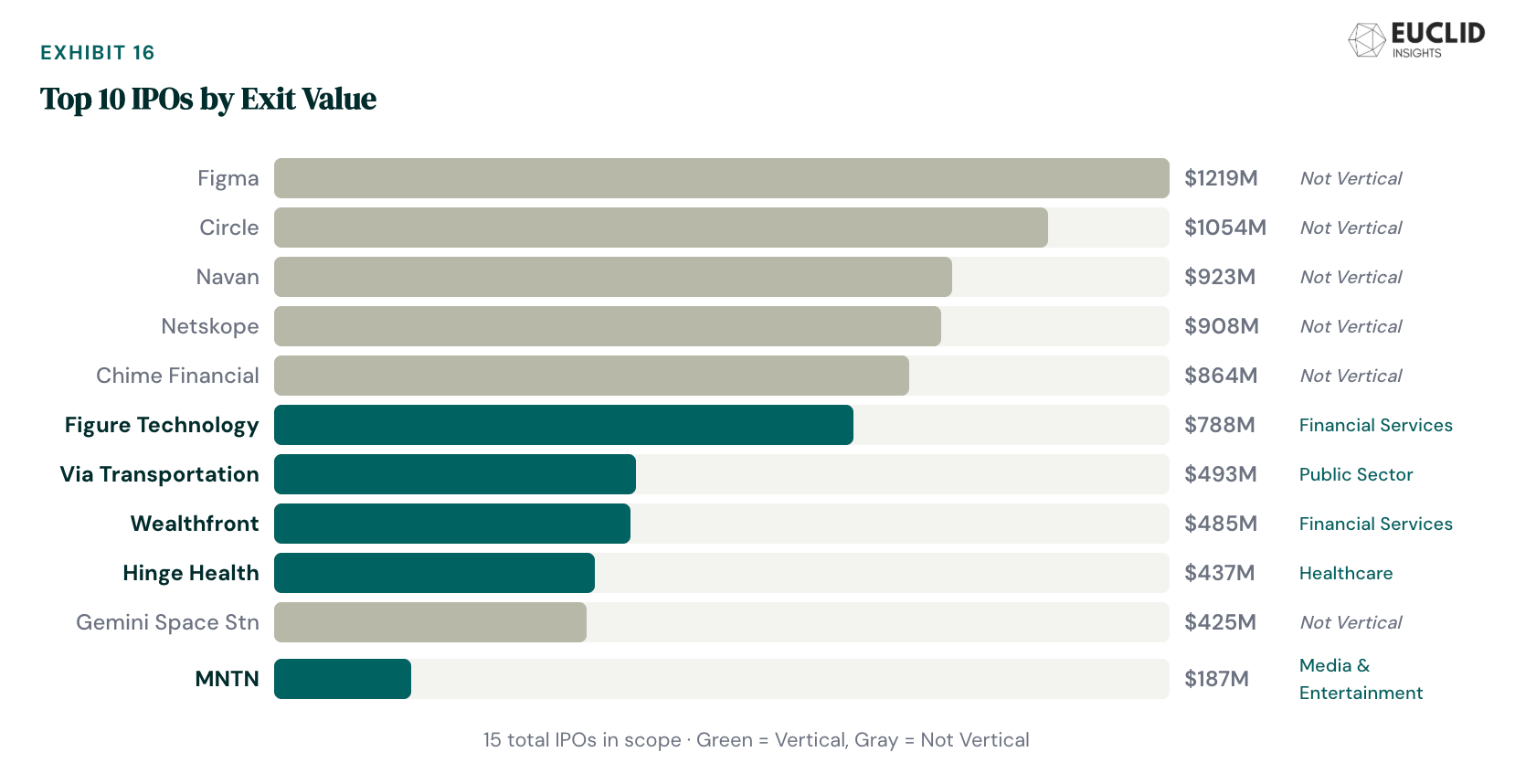

The IPO Window

After a two-year drought, the IPO market reopened meaningfully in 2025 with 24 total relevant offerings, driving $12.3B in value. Including both vertical and horizontal companies: Figma ($1.2B) and Circle ($1.1B) led on the horizontal side, while vertical standouts included Figure Technology Solutions ($788M, Financial Services), Via Transportation ($493M, Public Sector), Hinge Health ($437M, Healthcare), and MNTN ($187M, Media & Entertainment). The diversity of verticals—and a strong thread of B2C usage / B2B monetization—suggests an IPO market with a high bar for traditional software or consumer tech business models.

Exit Path Trends

Buyout/LBO transactions accounted for 20% of exits but a disproportionate share of value. Silver Lake ($4.5B Altera), EQT ($3.0B Neogov), and TPG ($1.1B SynXis) were among the most active acquirers. This confirms a continuing pattern: PE firms view vertical software as ideal targets—recurring revenue, defensible market positions, and operational leverage from AI integration. Over 80% of PE-backed software acquisitions in 2024 were vertical; that trend appears to have continued through 2025.

The most revealing exit metric may be the simplest one: the median vertical exit in 2025 was approximately $500M. For the many seed and Series A funds that have scaled up AUM since 2021, driving superlative returns via such median outcomes demands discipline on entry price that seems quite rare these days. At a $10-20M post-money seed, a $500M exit represents 25-50x gross valuation appreciation—exceptional. At a $50M+ post-money “seed” (increasingly common in consensus Vertical AI), the same exit is 7-8x gross. Still great, but tough math for a >$100M AUM fund.

The top 10 exits by value in 2025 accounted for over 60% of total vertical exit value—a reminder that no category escapes power-law dynamics. Below the mega-deals, PE remains a leading exit path and IPOs remain selective — the “middle market” of vertical exits ($250–1B EV) is arguably the healthiest and most under-appreciated segment of the liquidity environment, at least in VC land.

Top Exits & Other Trends

The quarterly exit cadence showed meaningful variation. Q3 led with 74 exits and $72.2B in value, while Q4 produced 54 exits and $60.8B. There was a boom in Healthcare exits mid-year: 12 in Q2, 19 in Q3, but just 7 and 5 in Q1 and Q4, respectively. Financial Services saw its own 1H concentration, with 17 exits versus 8 in the back half of the year. Along with Ansys, Manufacturing & Industrial had a spike in Q3—with 6 exits, half of its 2025 deals closed in that quarter.

The exit size distribution is worth noting. The top 10 exits by value accounted for over 60% of total vertical exit value, reflecting the power-law dynamics inherent in software M&A. Below the mega-deals, the median vertical exit was approximately $500M—large enough to generate meaningful returns for growth-stage investors but small enough that PE firms remain the natural buyers. The middle market of vertical exits is arguably less dependent on public market conditions or strategic M&A cycles.

VII. The Investor Landscape

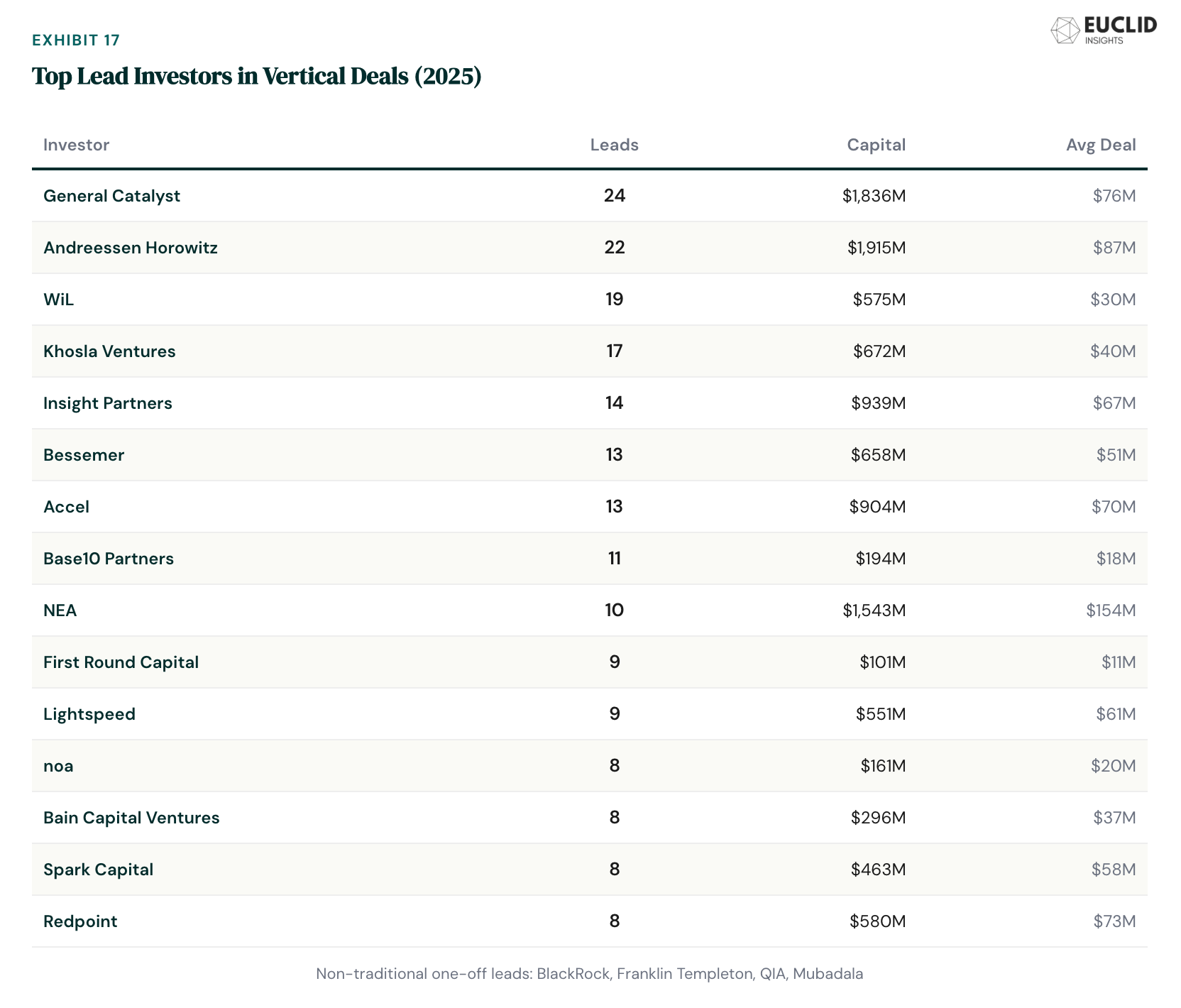

General Catalyst was the most active lead investor in vertical deals in 2025, leading 24 round representing $1.8B in value. Andreessen Horowitz followed closely at 22 leads over $1.9B worth of rounds, spanning Healthcare (Abridge), Legal (Clio), and Financial Services. WiL (19 leads) and Khosla Ventures (17 leads) rounded out the top four, with Khosla maintaining its earlier-stage focus at a $40M average deal size. Across the top 15, NEA’s average deal was largest by a wide margin at $154M, while First Round Capital had the lowest average deal at $11M.

At the $1–5M tier, Y Combinator was the most active at the earliest stage of vertical financing (7 leads), alongside Gradient (5) and HealthX (5). European-based funds also has a strong presence here, with Pi Labs and Nina Capital both clocking 4 leads.

The $5-15M band was anchored by First Round Capital with 9 vertical deals led in 2025, those startups capturing over $100M in aggregate. Next were Susa, Madrona, and Menlo, with 6 leads each, followed closely by Pear and Costanoa with 5 each.

In the $15-30M bucket, Base10 was the unequivocal vertical leader, with 11 leads at an average deal size of $18M. noa—the sole European investor in the top 15—was the next-active here with 8 leads. SignalFire—the third-place VC in this band with 7 leads last year—stood out with the highest average deal size of the cohort ($30M), and over $200M captured by its investees. Honorable mentions include Bonfire (4) and Building Ventures (4).

Moving to Series A and beyond—deals $30-100M in value—it’s perhaps surprising to see that a16z did not take first place in the vertical league table. That honor went to General Catalyst, with 24 leads (though a16z closely trailed with 22). Companies backed by these two firms raised $3.8B in total in 2025. The next tier of prominently vertical investors included Khosla (17), Insight (14), Bessemer Venture Partners (13), and Accel (13). While Sequoia may not have been as prolific this year (7 vertical leads), they registered the largest average vertical deals ($94M), with a16z and IVP close behind.

Late-stage vertical ($100M+) saw six multi-deal leads, all with a relatively tight mean deal size in the $110-180M range: NEA (10), Kleiner Perkins (7), Oak HC/FT (5), B Capital (5), DST Global (4), and Ribbit (3).

Concentration patterns within specific verticals are revealing. In Healthcare, a16z, General Catalyst, and Khosla accounted for a combined 18 of the top 50 lead positions. In Manufacturing & Industrial, a small number of growth-stage investors (including Coatue, Tiger Global, and GIC) drove a disproportionate share of capital through mega-rounds. Financial Services was the most fragmented—no single investor led more than 4% of deals, reflecting the vertical’s maturity and the breadth of sub-categories (e.g. payments, lending, insurance, wealth management, compliance).

The most popular verticals amongst this group of VCs was — no surprise — Healthcare (55) and Financial Services (38), together representing nearly half of the total deal lead count. Interestingly, Supply Chain and AEC & Trades were next, composing another ~14% of lead rounds. Most of the rest of the verticals fell in the 2-5% range, with Retail & CPG, Manufacturing & Industrial, Public Sector, Education, and Insurance clocking 5+ (and in that order of incidence).

Corporate venture activity in vertical AI also warrants mention. NVIDIA Ventures, Salesforce Ventures, and Google Ventures were active across multiple verticals. Perhaps more interesting was industry-specific CVC activity: health systems (Mayo Clinic, Kaiser) investing in clinical AI, financial institutions (Goldman Sachs, JP Morgan) backing fintech infrastructure, and energy companies (Shell, BP) funding climate tech.

A final interesting 2025 pattern was the (re-)emergence of non-traditional leads in big vertical rounds. BlackRock co-led Applied Intuition’s $600M round. Franklin Resources (Franklin Templeton) led Plaid’s $575M financing. Qatar Investment Authority participated in Applied Intuition. Mubadala co-led Crusoe’s $1.4B raise. While asset managers in pre-IPO rounds is familiar (reminiscent of 2021), the uptick of sovereign wealth involvement is perhaps more notable — especially in light of their parallel interest in backing US VC funds as LPs. Along with growing federal embrace of AI and defense startups in the US, the intersection of government and technology warrants continued focus in 2026.

VIII. Geographic Distribution

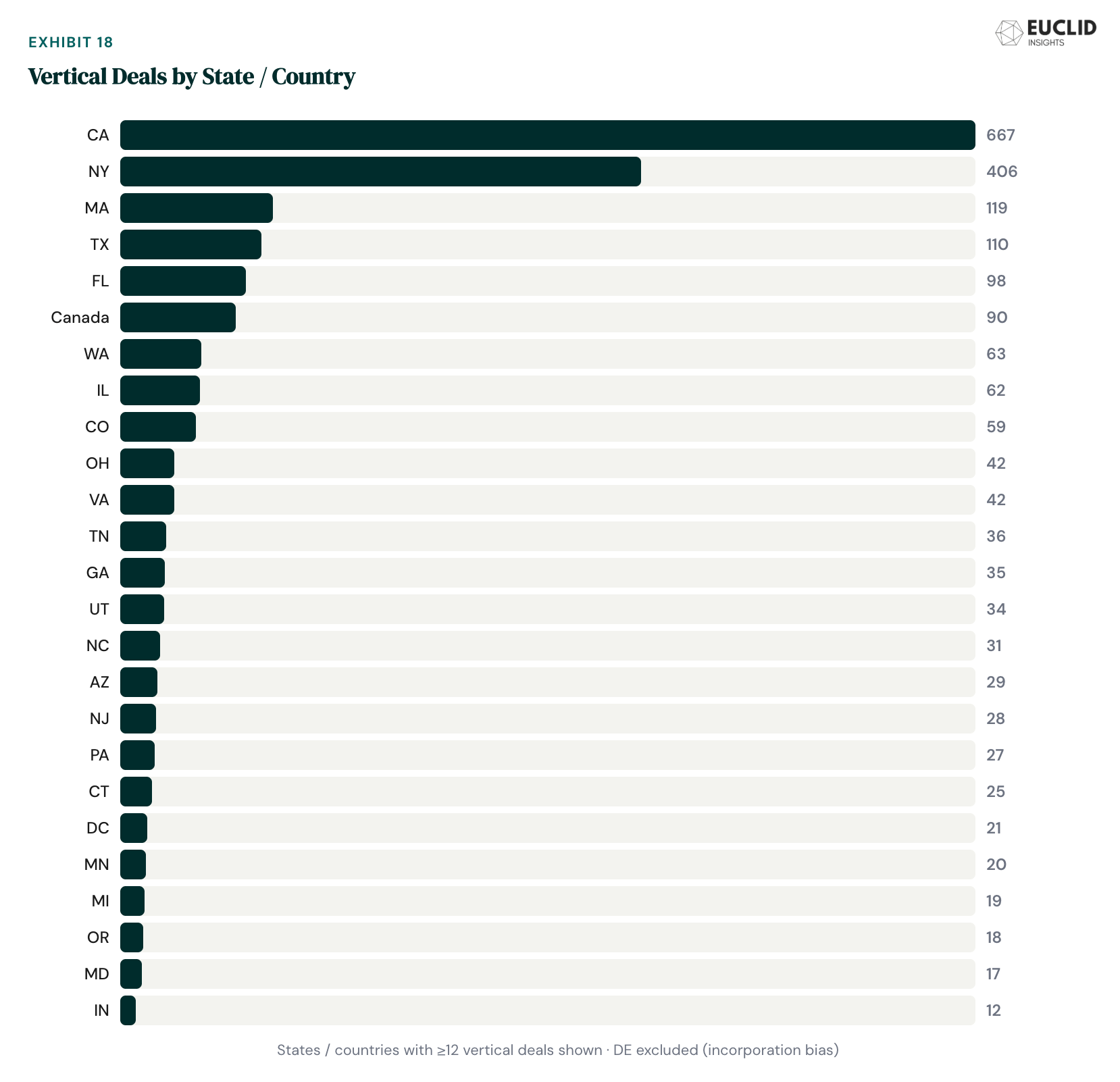

Vertical deal activity in 2025 was concentrated in established tech hubs but showed meaningful geographic breadth. California led with 667 vertical deals (29% of all vertical activity), followed by New York at 406 deals (17%). Massachusetts (119), Texas (110), and Florida (98) rounded out the top five. Washington, Canada, and Illinois each contributed 60–100+ vertical deals, reflecting the nationwide diffusion of vertical software.

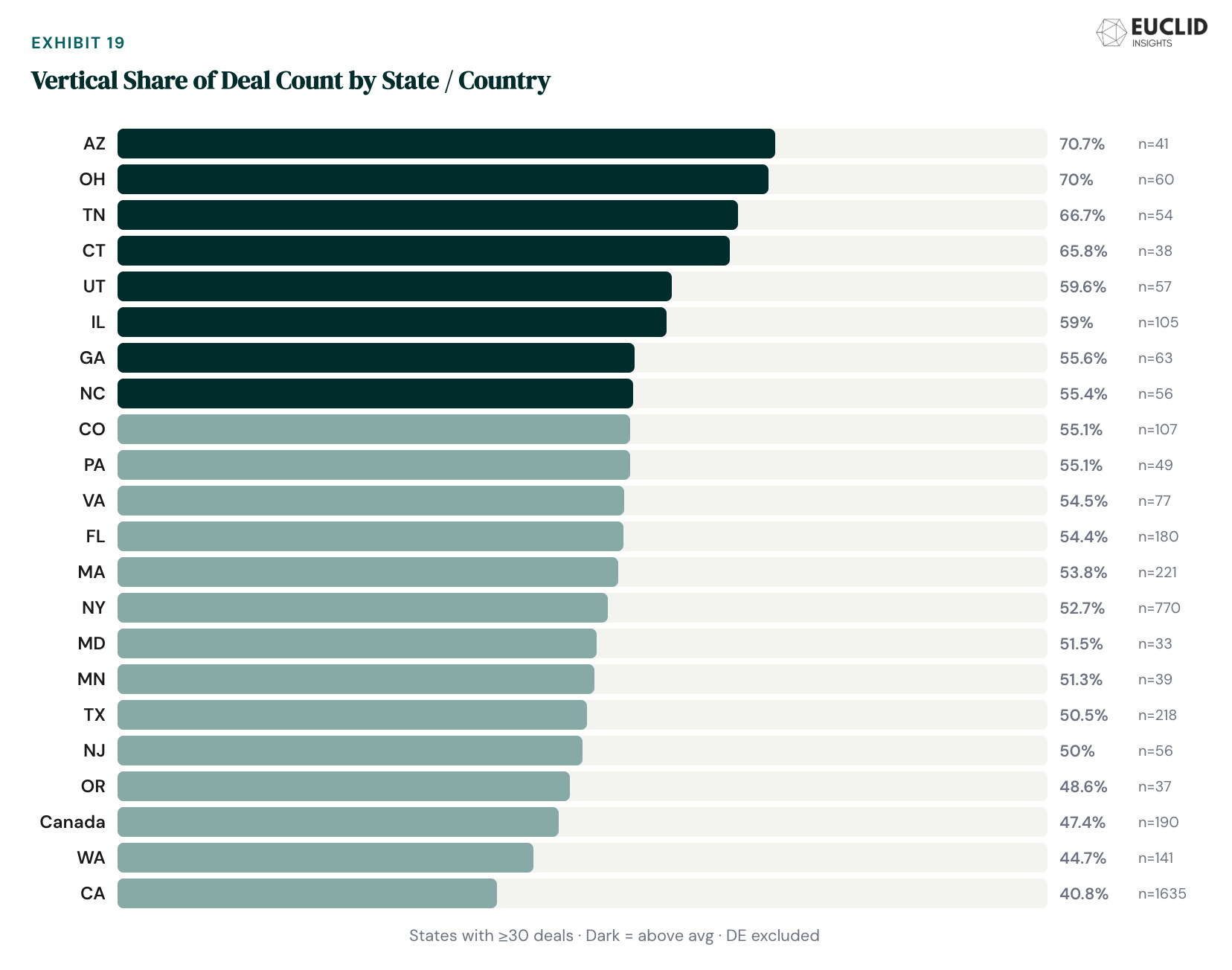

The more revealing metric is vertical share by state. Among states with meaningful deal volume (30+ deals), industry-proximate states dominated: Arizona (71%), Ohio (70%), and Tennessee (67%) posted the highest vertical shares. Illinois (59%), Colorado (55%), and Florida (54%) all exceeded the 55% average reference line. The most striking finding: California, despite leading in absolute deal count, had the lowest vertical share of any major state at just 41%—reflecting its deep concentration of horizontal AI infrastructure, foundation model, and developer-tooling companies. New York (53%) and Massachusetts (54%) tracked near the mean.

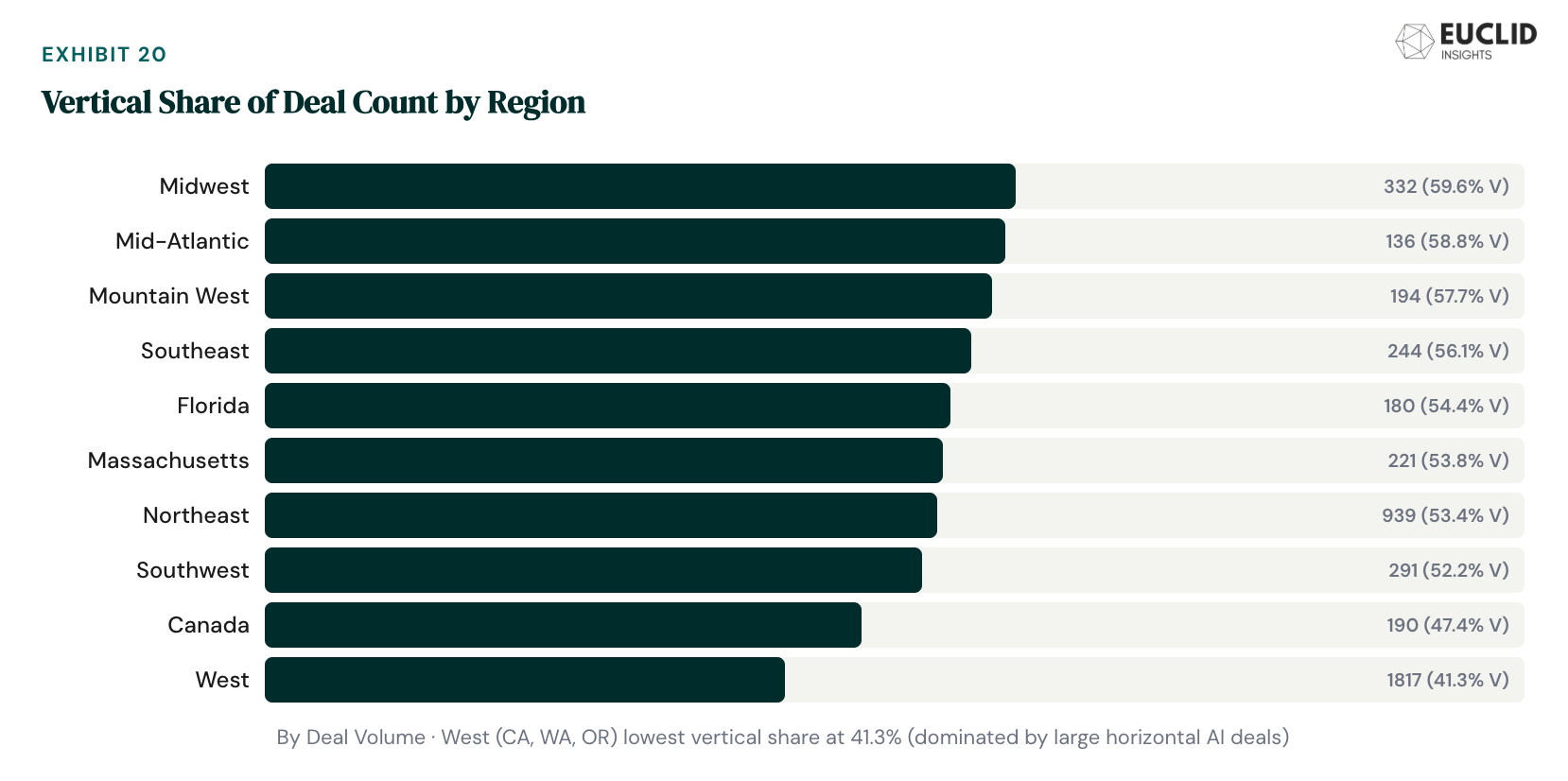

Examining vertical share by region uncovers some additional interesting findings. The Midwest leads in terms of vertical proclivity (59.6% of its deals). It joins a relatively tight high-mid-fifties grouping with the Mid-Atlantic, Mountain West, and Southeast. Overall variance between regions is actually relatively low, with Canada and the West representing the two greatest points of contrast.

Canada’s lower vertical leaning is somewhat surprising, given Toronto’s outsized vertical presence (the home of Constellation Software since 1995). We believe, however, that the country’s industry-specific focus is concentrated in that one metro—and that much of its “vertical reach” involves investment in US-based companies.

Finally, it shouldn’t come as a surprise that the West trails in vertical share by region, with a paltry 41.3%. As a global Mecca of technical talent—frontier AI and otherwise—the Bay Area drives the predominance of infrastructure, dev tooling, and foundation model / lab financing. It’s important to remember, however, that the clear plurality of vertical deals are still inked in California (667 in 2025). New York follows behind, with 406 deals. These two are the clear leaders by vertical deal volume, with a yawning gulf between them and the next tier: Massachusetts with 119 and Texas with 110.

In our view, San Francisco and New York City—considering volume, concentration, and subjective deal quality—remain the twin dominant vertical hubs, with strong and growing tailwinds behind the latter. Non-coastal hubs have the highest verticality. But whether they are as quick to embrace AI-native approaches at the formation stage as the hubs remains to be seen.

IX. What to Watch in 2026

From our vantage point at Euclid, a handful of structural dynamics from 2025 set the table for the vertical VC and startup landscape in 2026:

The Seed-to-A graduation test

In 2025, the goalposts for Series A shifted. Seeds now look like what Series As did 5-10 years ago. The result has been widening gap between seed and A, with contracting graduation rates between then. Seed-stage vertical AI companies raised at a historic clip in 2023–2025, but many will hit this gap in 2026–2027: strong product, real customers, not yet at the milestones today’s “true Series A” investors require. The sectors with the highest formation rates (Manufacturing, Legal, Public Sector, AEC) may end up being the most exposed.

We expect capital supply to adjust, but unevenly, as capital supply (VC funds and allocators) responds. That likely involves a drawdown in the current over-concentration of capital at “mature seed,” where too many funds compete for the same $3–8M checks—that competition has led to GPs looking earlier to get their ownership, and thus too many companies over-funded for their stage. In 2026, we expect many of them to hit that wall—perhaps creating great opportunity for VCs with “tweener” strategies, but also creating significant risk for the tier of excellent companies that haven’t hit exit velocity prior to the few-million-ARR mark.

Deep tech’s maturity cycle

Project Prometheus ($6.2B), Figure AI ($1.5B), and Applied Intuition ($600M) collectively raised $8.3B in 2025 for companies building AI that interacts with the physical world. They aren’t outliers—Periodic Labs raised $300M for autonomous robot-driven research facilities, Thinking Machines Lab raised $2B for scientific AI tools, and Physical Intelligence pulled in $1.1B for robotic foundation models. In total, robotics startups raised over $6B in just the first seven months of 2025, with capital concentrating into fewer, larger rounds. Manufacturing & Industrial led in share of 2025-funded companies founded 2022+, with a 57% share. Figure alone went from a $2.6B valuation to $39B in 18 months, while its robots were still performing controlled demos at a single BMW plant.

There’s an important distinction between hardware companies and Vertical AI as we define it. While it may be an outmoded term, Vertical AI is defined by the software layer, operating on fundamentally better economics than hardware businesses: lower capital intensity, faster iteration cycles, higher gross margins, and the compounding moat of domain-specific data. Physical AI is a multi-trillion-dollar opportunity that extends across the economy and will change the world as we know it over decades. In the short term, “deep tech”—at least, the version that conflates hard with valuable—is looking overextended. In the long run, we’re bullish on the vertical software layer bringing AI to physical action.

Shifting winds of liquidity

With Blackstone, Thoma Bravo, Clearlake, and Vista all executing multi-billion dollar vertical buyouts in 2025, the PE-led exit environment for mature vertical SaaS companies is robust. That cycle’s health depends on interest rates and debt markets, but the demand side is proven—and we expect that to continue to ramp.

Perhaps the bigger question, pertinent to the health of the venture capital ecosystem, is public market liquidity. 2025’s IPOs were a start, not the floodgate-opening many are waiting for. The backlog of late-stage vertical companies—many of which raised $200M+ rounds in 2025—will likely face go / no-go decisions on public listings in 2026–2027. Next year specifically, the vertical IPO pipeline looks sparse: beyond EquipmentShare’s January debut, Plaid is the only highly-rumored candidate of note, although there are many potential entrants. Overall, we estimate the IPO narrative in 2026 to be dominated by horizontal infrastructure & AI (e.g. Databricks, Anthropic, OpenAI).

A clarion call for AI defensibility

The defining tension in vertical software today is breadth versus depth, and the extent to which that facilitates defensibility in a fast-moving era of AI—we touched on this in a recent essay, called “Software Is Dead — Long Live Software”. Horizontal AI tools are getting better at surface-level tasks across industries, which means vertical players need to focus on the depth advantage their industry focus often lends—the surface areas of workflow, regulatory, and data idiosyncrasies that makes each sector unique. Emergent leaders in verticals that were seen as big, attractive land-grabs for solution-first AI—Harvey in Legal, Rogo in Finance—will come under increasing fire as the AI labs take low-hanging-fruit opportunities to extend their core competencies to industry. OpenAI and Anthropic have already made overtures in those two verticals. And while we haven’t yet seen the canonical example of vertical SaaS market leaders making the leap to Vertical AI leader, legacy systems of record are certainly ramping up sharp-elbowed tactics—we expect both startup displacement and defensive M&A to ramp up dramatically. In any case, the Vertical AI startups that will define 2026 will need to take specialization and long-term moats seriously.

Report Methodology

This report covers 4,395 US and Canadian VC financings of $1M or greater in software and AI, sourced from PitchBook’s transaction database with supplemental company-level data from Harmonic. The dataset spans calendar year 2025 and includes closed deals (at time of close, not announcement).

Deals not primarily software are excluded from the analysis—specifically: pharmaceutical and biotech, pure hardware and device companies, four-wall retail and services businesses, and capital-intensive infrastructure plays where software is incidental to the business model. The line between “software” and “not software” is increasingly blurry in an era of AI-enabled services; our general rule is that companies deriving the majority of their value from a defensible software or model layer are included, while those primarily selling labor, physical goods, or regulated products are not.

The remaining universe is classified as either vertical (defined primarily by the end market) or not vertical (horizontal tools, developer infrastructure, AI infrastructure, general-purpose foundation models, and 95% of crypto/blockchain). We don’t make an explicit distinction between B2B and B2C, though B2C is typically only classified as vertical when it is a market network connecting vertical stakeholders (e.g. lawyers, architects) with consumers, or the product is monetized vertically despite consumer usage (e.g. payors, realtors).

Exit data covers 158 vertical transactions (254 total) and includes M&A, buyout, and IPO events. To maintain focus on liquidity-generating exits, the following transaction types are excluded: recapitalizations, PIPEs, public-to-private transactions, acquisition financing, asset acquisitions, secondary buyouts, and reverse mergers (with the exception of SPACs, although none were recorded this year).

We selected 18 representative verticals which, while imperfect, cover most of the universe. AEC = Architecture, Engineering & Construction. CPG = Consumer Packaged Goods. We occasionally refer to Manufacturing & Industrial as Mfg., and Aerospace & Defense as A&D.

Market data providers’ coverage of recent early-stage deals (pre-seed and seed) is inherently lossy. As a result, the true volume of late-2025 early-stage activity is likely higher than what appears here. This bias, if anything, likely understates the share of early-stage Vertical AI activity.

Finally, big shout out to Gotham Chi for their work sourcing and classifying much of the data behind this year’s report. Founded by University of Chicago students, they work with startups and VCs with research and analysis — reach out to them here if you’d like to learn more.

Thanks for being a subscriber and supporter of Euclid Insights! The Vertical Report is published annually by Euclid: a VC firm backing Vertical AI founders from inception. For questions, please reach out to the Euclid team via LinkedIn or DM here.

Enjoyed reading this!

Great work, Nic and Omar -- excellent report.