The Next Chapter for Vertical Software

SaaS isn't dead, it's being re-born

We founded Euclid because we believe we are in the early innings of an inevitable transformation resulting in every vertical of the economy being powered by its purpose-built constellation of software. LLMs have been a powerful driver of net new wedges and platform architectures pushing that secular trend forward. However, an equally important, if underappreciated driver has been business model expansion. We touched on this in a previous essay, A Framework for Evaluating Vertical Software Value Creation:

…a significant innovation in driving adoption, increasing market share, and producing winners has been an emerging class of vertical software companies that have moved beyond traditional SaaS pricing paradigms, attaching themselves to discrete industry-specific value streams and business outcomes. The net result of this shift is an order-of-magnitude increase in market size for vertical startups and potential venture-scale outcomes.

The first chapter of vertical SaaS saw our knowledge of successful cloud apps transposed to specific verticals. In many cases—Autodesk, Appfolio, Veeva—that play was and remains outstandingly successful. It has now become clear, however, that a seat-based subscription OpEx is not the universal path to technology adoption across industries. The next chapter of successful vertical software is seeing the incorporation of substantial business model innovations, taking into account the idiosyncrasies of each vertical to minimize friction of adoption.

The Evolution Beyond SaaS

In today's essay, we will catalog the new archetypes of value creation to demonstrate how historical assumptions around the difficulty of SaaS adoption in certain verticals may not hold in the future. In our view, this logical evolution of vertical software business models will go a long way toward subverting the heralded “the end of SaaS.”

Matt Brown of Matrix wrote a great piece on the Invisible asymptotes in vertical software, discussing the hidden constraints that limit the growth of a company and market:1

Vertical software models have their own asymptotes. For SaaS-focused ones, the asymptote was the number of potential seats in a company and the amount that could be charged per seat. Even if they captured 100% of the seats in a company and charged a high SaaS fee, the overall spend on software would still be a small fraction of the business's expenses or revenue. This product and pricing model was the asymptote.

As we discussed in our piece around value creation for the next generation of vertical software companies, new startups have already begun to dismantle this asymptote by moving from traditional SaaS to hybrid business models:

Consider this simple framework: in many traditional industries, technology spending has often plateaued between 2- 5% of overall industry revenues. At the lower end of this spectrum, an industry would need >$75B of gross revenue to reach a potential $1B software TAM. It also strongly limits the number of potential winners in low-spend categories. However, business model expansion has enabled new vertical startups to capture value from the 95% of non-tech spending, including sales & marketing, materials, freight, payment processing, labor, recruiting, training, insurance, banking, and many others.

The impact of this hybridization was an increase in TAM and the number of venture-scale vertical markets. Many of these hybrid monetization models expanded their market opportunity because of their approach. In other words, prior, their ability to service customers constrained by IT spending—by positioning to capture non-software budgets, this constraint evaporates. Toast, Flexport, ServiceTitan, and many others have succeeded by combining software with transactional and Fintech revenue streams. The hybrid model is already quite dominant in at-scale vertical SaaS and we don’t expect that to change in the near term. For example, we remain particularly excited about novel vertical-specific approaches to common HCM and FinOps challenges. Despite its success, we believe horizontal product expansion strategies in vSaaS, financial services and otherwise, are still in early innings of adoption across the ecosystem.

Hope You’re Ready for the Next Episode

As we run the hybrid monetization model in vertical software forward, it’s clear we will reach yet another asymptote eventually, reaching constraints similar to those of traditional SaaS: a limit on venture-scale markets constrained by a set number of customers and a glass ceiling on ARPU. Just like IT budgets were constrained for SaaS, there are ceilings on reasonable take rates from product expansion and financial services.

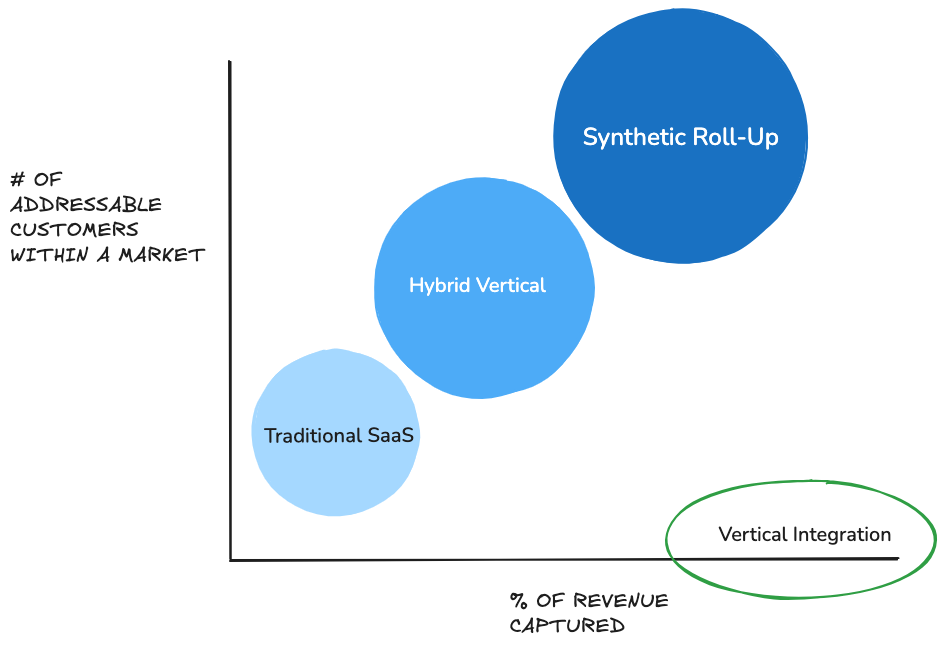

It follows that the next successful vertical platform archetypes will need to further innovate. The next frontier, we believe, will not only contemplate multi-product expansion but also new mechanisms to fundamentally rethink what software TAMs can be. SaaS of the past give businesses the tools to do something better. Software platforms of the future will facilitate the creation of new businesses and take more direct responsibility for helping existing enterprises grow. To offer a simplified analogy, it’s the difference between software as a budget line item to support a department, and a software platform subsuming the function itself, becoming a partner more than a tool. Amidst this evolution of vertical software, we see two distinct species emerging:

Vertical Integration: the startup is the sole customer of the software, scaling revenue through tech-enabled services and/or roll-up strategies.

Synthetic Roll-Ups: a concept we introduced in our piece on AI Roll-Ups

A Synthetic Roll-up—still fundamentally an application-layer software platform, [even if it isn't seen that way by customers]—holistically powers, helps operate, or directly contributes to the growth of legacy businesses. It brings to the table SaaS, yes, but also a highly vertical-specific wedge and likely some network element that contributes to a healthier business model for the operator and / or consumer surplus for their customers. This “roll-up” doesn’t own the underlying business but it is enough of a “partner” to earn share in its upside—either a share of revenue / profit or via some other value-based model.

While we have and will continue to invest in vertically integrated businesses, these usually involve significant capital intensiveness, tougher margin profiles, and higher exposure to operational or macro-economic risks. We remain highly sensitive to these downsides, though we do think one shouldn't throw the baby out with the bathwater here—there are limited forms of vertical integration we believe may yield fruits without poisoning the magic of the software business model.

We’ll cover a deep dive on vertical integration and service-as-software in an upcoming piece. The net impact of the Synthetic Roll-up, however, is another step-function increase in addressable market opportunity for vertical software, both in terms of customers and revenue capture, while maintaining the promise of highly efficient business models.

Successful Archetypes of Synthetic Roll-Ups

At their core, Synthetic Roll-Ups entail two key interconnected modalities that unlock larger TAMs: (1) removing vertical-specific constraints to growth and (2) leveraging economies of scale through aggregation. We wanted to highlight a few specific successful archetypes we’ve come across, with focus on the “wedge product” that is driving adoption in ways that traditional SaaS could not.

Business Formation

Marketing Services

Sales Enablement

Roofr built a service enabling roofing companies to win more business by automating roof measurements and proposals with software.

EvenUp automated the process of demand-letter generation for personal injury law firms, enabling them to increase caseload and revenue.

Tarro built a multi-language phone ordering service, starting with independent Chinese restaurants.

Business Operations

Dandy helped dental offices increase revenue and improve patient outcomes with digital scanning and software.

Cents enabled laundry and dry cleaning businesses to grow their businesses by offering pickup and delivery.

Theradriver built software to optimize scheduling, improve clinician utilization, and increase revenue for ABA clinics.

Payments & Financing

What we find particularly important about wedge products in Synthetic Roll-Ups is their predominant focus on helping customers generate more revenue (even those starting from zero). The “efficiency” cost-cutting ROI story is far less compelling for these models, with two exceptions: (1) that efficiency is tied to revenue or business expansion in the mind of the customer, or (2) the target vertical has endemic and existential problems with unpredictable costs, something we would most often expect in asset-heavy industries.

As we discussed in our essay, Nobody Wants Your Product! on reaching Vertical PMF, founders need to identify latent demand for their wedge product—and this is especially true for driving the widespread adoption required for a Synthetic Roll-Up play:

Before any solution can take hold, genuine, sustainable demand must exist in some form, even if market dynamics have suppressed that demand to date. What do you need to hear from your market to validate latent demand? You don’t need to hear a desire for software products…Successful founders—even those deeply embedded in their vertical—spend time identifying how software can be built around the work to be done.

The early success of startups applying AI—currently most often LLM-based—to ubiquitous, mandatory “work to be done” is one reason we’re extremely bullish on the Synthetic Roll-Up. Especially for emergent use cases within sales enablement and business operations, the ability to synthesize unstructured voice and text data and extract information (for example) has rapidly opened up new opportunities for AI-first startups to attack novel revenue-generating opportunities and markets. Combining these capabilities with mission-critical workflows, new entrants can rapidly gain adoption even in markets with constrained IT budgets and / or entrenched incumbents.

The Winning Playbook

In sum, the Synthetic Roll-Up playbook is simple but powerful:

Identify an impactful constraint to revenue growth for your vertical and solve it.

Drive growth with an easy-to-adopt wedge and aggregate businesses.

Become the all-in-one solution for vertical, leveraging scale and first-party data to layer in more products and services over time, increase revenue per customer, and build a compounding moat.

It is through customer aggregation that Synthetic Roll-Ups earn upfront demand v1 SaaS could not, develop meaningful leverage off the bat, expand accessible budgets, and build staying power by embedding in customer businesses—and while partners more than tools, they can remain software businesses at their core.

Expanding the software product suite remains a crucial enabling strategy but traditional adoption frictions will remain. Next-gen opportunities lie in leveraging economies of scale as the customer base grows. The strongest examples of this are driving in-network demand and collective bargaining with suppliers and service providers. Slice, for example, drives top-of-funnel for its pizzerias through its consumer app while also negotiating group discounts on key supplies like pizza boxes. Rula provides in-network client referrals for their therapists and psychiatrists while also negotiating payouts from payers. Roofr expanded beyond measurements and proposals into material ordering and financing.

As a result, Synthetic Roll-Ups can grow in wallet share alongside the value they provide to customers, initially around revenue growth but also participating in cost reduction achieved through economies of scale. Such success-based models align incentives but, equally importantly, enable startups to capture high wallet share; at scale, these models can earn anywhere from 10% to 30% of customer revenue, an order of magnitude higher than pure SaaS or even hybrid models. Such meaningful take rates obviously greatly expand both TAM and the universe of potential venture-scale markets.

This is why we bristle when we hear chatter about the prospective end of vertical software: there is naturally a limit to the business models that have brought us here but the scope of the larger software opportunity is widening—and we believe it will only grow with the rising capabilities of LLMs.

There may be markets where vertical integration, including traditional roll-up strategies, could be preferable. Our bet, however, remains that the biggest winners in this AI-first vertical software world will remain application-layer platforms. We’d wager this will be true in an absolute sense, but it will almost certainly be true when adjusted for return on capital raised.

Thanks as always for reading Euclid Insights. For more suggested reading, check out the rest of our sources here.2 Building a Synthetic Roll-Up or want to chat more about the model? Please reach out or share feedback in the comments below!

Brown (2024). Invisible Asymptotes in Vertical Software. Matt Brown’s Notes.

SignalFire. (2023). AI Business in a Box. SignalFire. https://www.signalfire.com/blog/ai-business-in-a-box

Single Aim Health. (2023). Growth of the Healthcare "Business-in-a-Box" Model. Single Aim Health. https://www.singleaimhealth.com/news/growth-of-the-healthcare-business-in-a-box-model#therapists

O'Malley, Bornstein, Brussell (2023). From digitally native brand to digitally native franchise: a new model. Forerunner Ventures.

Haber (2024). The Messy Inbox Problem: Wedge Strategies in AI Apps. a16z Enterprise

Yuan (2024). The Franchise: An Archetype for Vertical SaaS. Tidemark