The concept that Vertical AI is going to be won by whomever who can jam AI down the throats of an industry fast enough is sorely mistaken. There’s a deep graveyard of startups from the last decade filled with ideas that took the same view with SaaS. No doubt, speed matters—and exploring how AI can bring net-new leverage (that prior software generations could not) is important. But ultimately, most industry buyers don’t care are AI for AI’s sake.

Today’s episode is the reminder that the most powerful wedge into a vertical is usually quite simple: help someone run (or perhaps even start) the business, become their #1 trusted partner that’s not on the payroll, and then steadily earn the right to help power more and more of their growing enterprise.

Dan Friedman, our Vertical Titan this week, is a man of many talents. Starting out as a Thiel Fellow—like VERTICALS’ own Luke Sophinos—he found success in his first startup Thinkful, an early online bootcamp that helped over 10k people change careers. He sold this business to Chegg, before launch yet another shot at category-creation: Boulton & Watt. Dan calls it the “world’s slowest startup incubator”… and in today’s episode you’ll get a taste for the depth and open-mindedness his team brings to launching net-net vertical platforms.

You’ve likely heard of their Dan’s incubation, Moxie. The leading OS and digital partner to aesthetic practices (e.g. medspas), Moxie has become a poster child for the vertical business-in-a-box model, finding incredible growth in a regulated, state-by-state, and wildly expanding market.

In this episode, we’ll dig into Dan’s learnings with Moxie, the business-in-a-box model, his framework for validating opportunities with this model, and how early on, services & third-party software can actually help drive trust. Stick around for our debate on the role of AI in driving early vertical customer trust.

A Quick Word from Our Partner

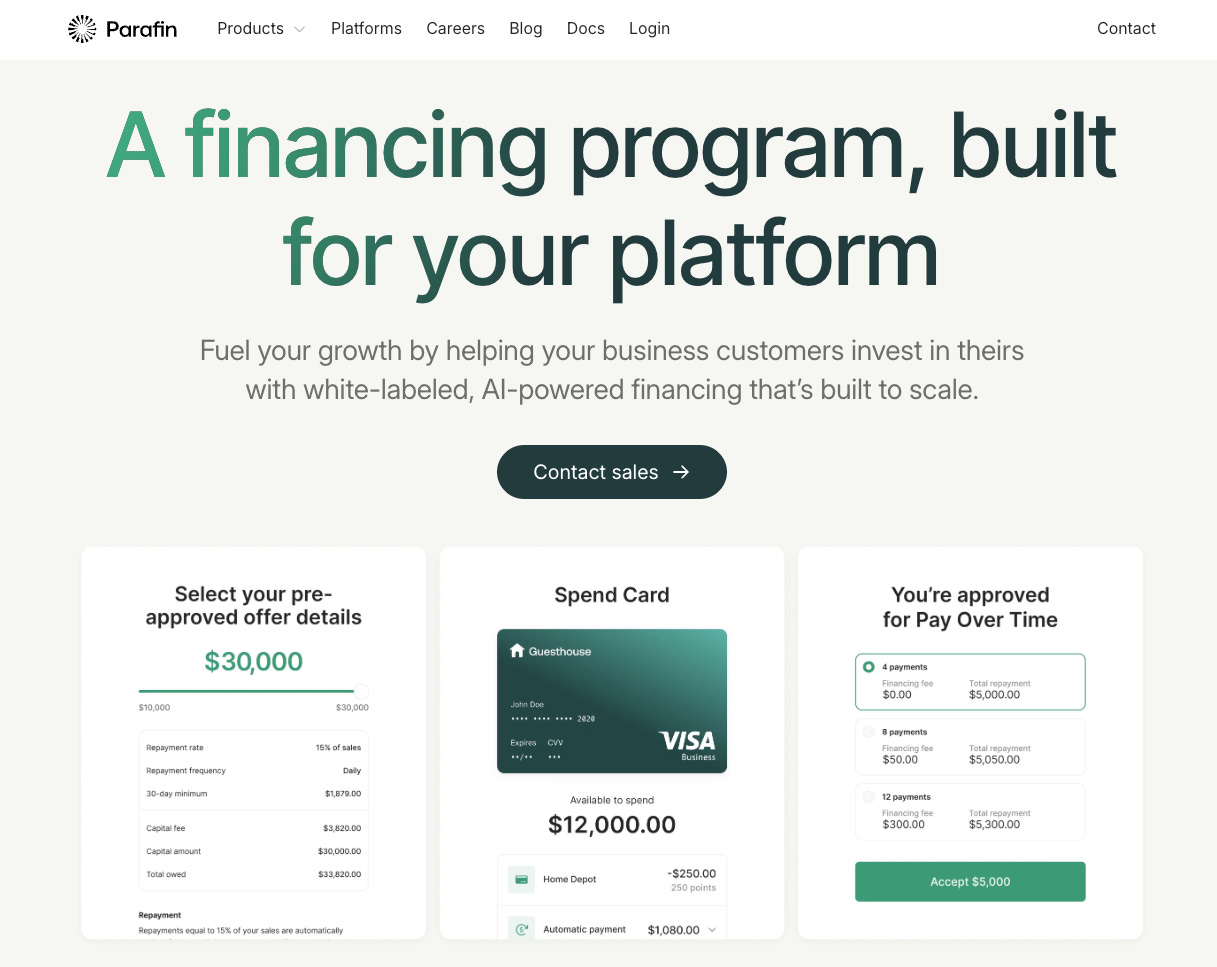

If you’re building vertical software or marketplaces, you should know Parafin. They power embedded capital and financial infrastructure directly inside vertical platforms like we ones we interview & analyze on this show. Learn how Parafin can turbocharge your vertical revenue and retention here.

I) Vertical Market Pulse

SoftBank’s capital rotation into vertical AI infrastructure

SoftBank’s ~$6B Nvidia Sell-Off | downloadvestr @ X

The headline was simple: SoftBank dumped a ~$5.8B Nvidia stake. We don’t think this is a bearish development. More a “capital rotation” to increase more exposure to the full stack (compute → chips → data centers → robotics), with the bet that specialized infrastructure will be the bottleneck as AI gets deployed into real vertical workflows.

Founder implication: your application-layer product likely depends on reliable inference in a certain price band. It’s always worth considering where that price needs to go or stay to make your model work. Dollars pouring into power, GPUs, and capacity in AI land is net helpful keeping costs low. But there’s also no guaranteeing market sentiment, macro stability, or timing on investors’ willingness to subsidize growth.

The odds of making it to $25M ARR are <20%

The Odds of Making It | Kyle Poyar @ Growth Unhinged

Kyle Poyar put real numbers behind the the real-world difficulty of achieving meaningful startup scale. Most companies get to $1M ARR, eventually. But the number that get to $10M or $25M ARR are more in line with the acceptance rates at elite US universities. Probably the best takeaway from this worthwhile piece is that early ARR milestones are often a bad proxy for the long-run outcome. Especially in vertical markets, there are plenty of examples of businesses that saw their growth spike 2, 3, even 5 years in. After all, venture-scale company-building is a long game.

Founder implication: if venture-scale is your bet, $1-2M ARR doesn’t tell you much. Design for compounding while keeping tabs on your staying power—especially in a world of uncertain AI wedge retention.

Mercor’s $10B valuation and the “AI services” gold rush

Mercor 4x’s Valuation to $10B with $350M Series C | Ram Iyer @ TechCrunch

Mercor is a great case study in where vertical AI supply chains are forming: domain experts, labeling, RL infrastructure, and the messy human inputs required to get models from “general” to “useful in production.” The debate (and it’s a real one) is whether this is software, services, or a tech-enabled labor marketplace—and how durable the moat is when everyone has access to similar models. In any case, Felicis sees it working, leading this round just 8 months after it led a $100M Series B for the business at a $2B EV.

Founder implication: if you’re building a services-heavy wedge, be honest about defensibility. Services can be the fastest path into the workflow. As Mercor and others can show—paired with the right market and timing—services can scale incredibly quickly. Just remember, however, the long-term win is owning the system, not just reselling labor (even if that labor is AI powered, it’s the customer lock-in that matters). Hopefully easy in doesn’t mean easy out.

II) Vertical Titan

Dan Friedman — Founder @ Moxie

(and Partner @ Boulton & Watt)

The backstory

Dan began his career as a Thiel Fellow, before co-founding Thinkful, an online education business built around one-on-one mentorship. After scaling it into the online bootcamp wave, he sold Thinkful to Chegg in 2019.

Post-acquisition, Dan realized his favorite part of the journey was less the years of growth-scale management and more so years 1–3: chaos, rapid learning, and trajectory-changing decisions. That informed the philosophy behind Boulton & Watt. His idea was to start one company at a time, pour time into those early years getting to tangible scale, and then hire the right leader for the business. “Replace ourselves,” as Dan put it, and repeat.

Boulton & Watt is unique as a venture-funding entities go. Most incubators use a complex holdco / fund structure that can create misalignment, overhead, and incentives mixed across share classes. Dan deliberately avoided this, opting for a radically simple model: a small entity with minimal overhead, common-only ownership, and direct SAFE investments at predefined terms. All aligned with Dan’s view on keeping his focus on those critical first years of company-building.

Their first breakout was Moxie, a business-in-a-box platform helping aesthetic clinicians (e.g. medspas) launch, run, and grow compliant businesses across a fragmented, state-regulated landscape. With 115 employees and >$25M raised to date from VCs like SignalFire and Lachy Groom, it’s off to an incredible start. His next, Meadow Memorials is attacking end-of-life care, a similarly under-looked, and certainly under-innovated space. Throughout our episode, we stay mostly focused on Moxie: namely, Dan’s learnings around the vertical business-in-a-box model.

The hardest part

Picking what not to do early (real estate was a huge “maybe,” and they deliberately tried to win without owning it).

Operating across 50 different regulatory frameworks — then learning the hard way that state-by-state differences are not a rounding error.

Starting as a services + off-the-shelf stack (e.g., stitched tools) without overcommitting to building “the suite” too early.

Surviving the natural churn of micro-SMB new businesses while building toward a product/service bundle that becomes painful to leave.

Moving upmarket without resetting customer expectations faster than the product and services can keep up.

Memorable lines from Dan

On starting early in the medspa lifecycle: “[We wanted to] build the Stripe Atlas for medspas.”

On ROI: “Build something people want [and value]… Anytime the value math isn’t true, it’s a five-alarm fire.”

“A company is defined as much by what it chooses not to do.”

The wedge: start the business, then become the operating system

The simplest version of Moxie is also the most powerful: they didn’t try to win by selling a better scheduler to existing medspas. They went after the deeper unsolved pain — people who already wanted to start a medspa, but couldn’t navigate the complexity, cost, and compliance.

That “launch” wedge earned them the right to expand into “run” (systems + operations) and “grow” (repeatable playbooks and services that move the revenue needle).

Don’t be afraid to say no (leave some parts to the customers)

Early on, real estate looked like an obvious blocker to business creation. All new owners had to deal with it—you can’t do a Botox injection over zoom, after all. But it’s also a notoriously tricky and bespoke challenge. So Dan’s team inverted: assume it will make everything harder, and see if the customer can solve it without you.

In practice, many founders launched in salon suites or found creative arrangements. They’d often thought of their approach to RE well in advance. Which let Moxie focus on the parts that were uniquely painful (compliance, setup, integrated operations) instead of becoming a real estate company by accident.

Earning the right to a revenue share

Instead of seat-based SaaS, Moxie aligned pricing to outcomes with a percent-of-revenue model (starting at 9%, with tiering as customers scale). They explored percent-of-profit, but rejected it as too gameable.

The key operating mechanic: a value calculator (internal and customer-facing) that answers one question — “What would it cost you to self-assemble everything you get from us?” Their goal is that self-assembly costs ~2x more. If that stops being true for a segment, they treat it as an emergency.

From early churn to world-class retention

Dan was candid that early retention wasn’t magical — new micro-SMB businesses naturally churn, and early product/service gaps show up fast.

Over time, they expanded what they offered, improved what was “only okay,” and built toward a bundle that makes switching meaningfully painful. The result: gross retention approaching the mid-90s, with net retention driven by customer growth (they grow as customers grow because the pricing is tied to revenue).

GTM: inbound first, then field

For years, Moxie ran an almost entirely inbound motion because the ICP (new starters) is hard to find predictably via outbound. They proved demand with a landing page and basic ads, then built an inbound machine around the moment someone decides: “I’m going to start a medspa.”

As the company expanded into existing medspas doing multi-vendor swaps, they began leaning into more traditional outbound, events, and field sales — because the buyer is no longer “in the moment” of starting from scratch.

Dan’s three-part filter for business-in-a-box markets

Dan laid out a clean framework for when he thinks this model works:

Latent entrepreneurship desire already exists (you’re not convincing people to become founders—meaning a growing market and lots of folks going solo).

Unit economics succeed often enough (the average new business can actually win).

Scale economies compound (ROI to customers grows the more you have onboard).

III) Vertical Playbook

Vertical Business-in-a-Box

Why it works

Vertical markets often don’t adopt “better software” on your timeline… especially when compliance, regulation, and fragmented workflows make switching risky.

A “launch” wedge—partnering with entrepreneurs when they incorporate—may be harder to time, but completely flips the switching cost consideration. You meet the customer at the exact moment of maximum urgency, help them cross the activation threshold, and then expand into everything adjacent because you’ve already earned trust. Perhaps the safest place to stand in a volatile moment of AI transformation is deep in a specific workflow with proprietary operational context and high switching costs.

How to run it (Moxie-inspired blueprint)

Start with a single high-intent moment (e.g., “I want to start X business”).

Stitch together the stack with off-the-shelf tools at first; don’t confuse “owning code” with “owning the workflow.”

Build services where the pain is highest, even if margins aren’t perfect early.

Replace components only when the customer experience demands it.

Price to value capture (revenue share, transaction, workflow ownership), not seats.

Build an ROI/value calculator that both your team and the customer can reference at any time.

Expand personas and segments slowly, because each step upmarket resets expectations.

Founder litmus tests

How hard is it actually for people to do the thing your wedge is enabling?

Is the compliance/regulatory pain real, recurring, and persistent (e.g. due to state-by-state fragmentation or reporting requirements)?

Can you become cheaper than self-assembly while offering a better outcome?

What economies of scale can you drive on demand aggregation (software, procurement, embedded services, better playbooks, better data)?

How profitable are your ICP normally? What is a reasonable share of revenue (or profit, though this is dangerous as it can be gamed with accounting tricks) is reasonable? Can you see a path to offsetting this take with growth lift for your customers?

Is your opportunity constrained to net-new operators? Or do you have the opportunity to pull in small existing operators as well? If not, is the market growing fast enough for the TAM numbers to pencil?

What we debated on-air

We went straight at the “services moat” question in an AI world:

The pro-services view: if you “become the department,” you embed so deeply that churn becomes structurally hard — and you can automate more over time.

The skeptical view: services can become a knife fight if the work is fungible and everyone has the same models — you wake up as a low-defensibility services firm with tech dressing.

The synthesis: services are a great wedge if they pull you toward workflow ownership, proprietary operating data, and expansion across the customer’s P&L — not if they leave you stuck selling labor.

We also discussed whether empowering business creation yields enough TAM in most cases. In most markets, the number of net-new businesses each year is a small fraction of the total existing (and even of the existing SMBs). Medspas are seeing incredible growth, making Moxie perhaps uniquely positioned to be able to rely on business formation—other markets likely require the ability to capture some share of existing in the nearer-term.

Next week on Verticals

Tune in next week to cover a big topic—Vertical Fintech—with the formidable Rahul Hampole of ServiceTitan.