What's My Stage Again?

Why seed is obsolete — and the age of Inception capital

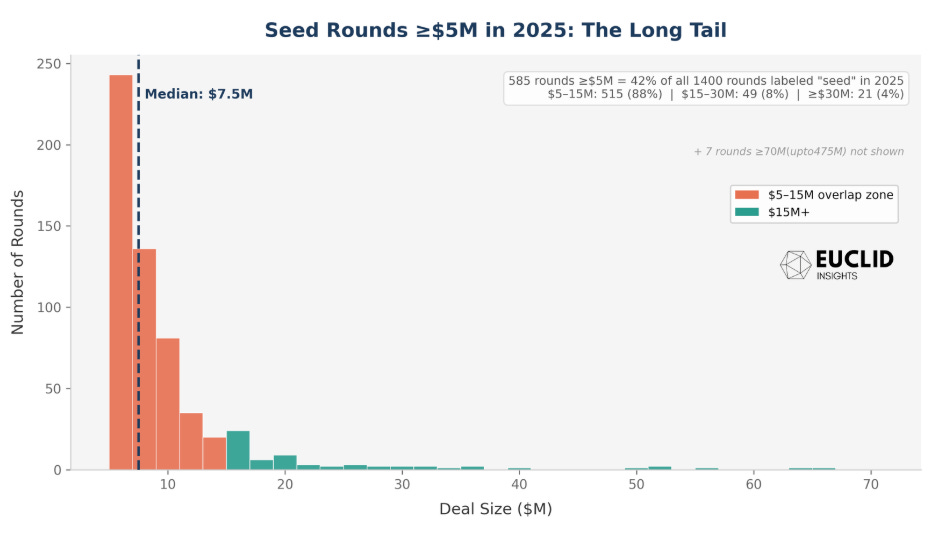

It’s increasingly hard to figure out what “seed” means. Carta’s 2025 annual State of Pre-Seed report found that 95th percentile seed valuations reached $80.5M, nearly 3x higher than the 95th percentile just 6 years ago. Meanwhile, 42% of seed rounds last year were >$5M raises. Thinking Machines Lab raised a $2B “seed.” Unconventional AI did $475M, Periodic Labs $300M, Merge Labs $252M, and so on. According to Crunchbase, 2025 set records for seed rounds of $100M+, totaling over $10B in capital.

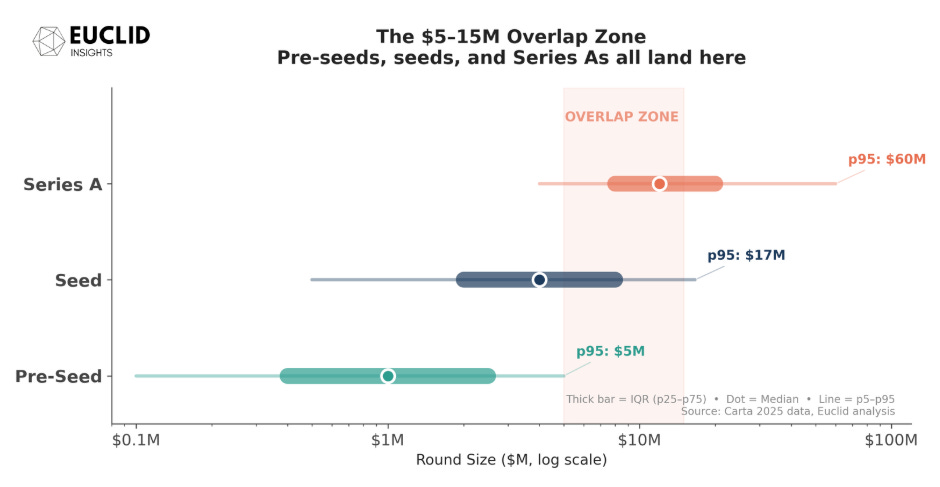

Look at the $5–15M range in the chart above—in any given month, there are pre-seeds, seeds, and Series As all landing in that band. The word “seed” is being applied to $500k SAFEs and $15M equity rounds. It spans pre-product, pre-revenue teams and companies with millions of ARR. Functionally, the term is now useless.

What actually determines stage nomenclature? It’s honestly hard to say.

Confusion by Design

VC round sizing is — and has always been — more vibes-based than deterministic.

1. Round order (“your first round is a pre-seed, your second is a seed”) never made much sense. Extensions, rolling closes, and opportunistic follow-on slugs throw off the sequence—especially in large datasets.

2. Traction sounds right in theory, but anyone crunching numbers either doesn’t have access to the full data set (e.g., managers analyzing portfolio data) or doesn’t have access to fundamental performance data (e.g., analysts like Carta). Proxies like headcount are too imperfect to be helpful, though Carta’s data does show Series A teams now average just 16.8 employees—down from 25.9 in 2021—reflecting the AI efficiency thesis in real time.

3. Self-reporting is what most structured datasets ultimately rely on, drawing from press or share names in filings. There’s always been a founder (and VC) incentive to report the “youngest” round possible—to seem more precocious. We’ve known founders who did three consecutive “seeds” even though they were hot commodities, purely for positioning. There’s nothing wrong with that—in fact, sometimes it’s the smart move to improve the chances that the right funds will think of you on first glance (though it won’t fool anyone sophisticated at the end of the day). Self-reporting is as inaccurate as it sounds.

4. Round size was historically the most reliable heuristic. Rounds of $1M, $3M, $10M, $30M, and $80M mapped cleanly to pre-seeds, seeds, Series As, Bs, and growth. It was never perfect, and some share of rounds were always way out of band. But in today’s market, that mapping has almost completely collapsed. In the last 12 months, we estimate pre-seeds have grown by 50%. $10M seeds are de rigueur. While perhaps eye-catching in their own ways, neither the $6M Series As nor the $600M Series As are abnormal.

There’s no good single heuristic and we’re not arguing it should be otherwise. But these stage names do play a role in high-level sorting and self-selection in our ecosystem. Founders use the terms to signal to the market the sort of round they intend to raise. VCs use them to signal to founders the sort of investments they like to make (and to LPs, where in the capital stack they play).

Our argument is that we have reached a moment where the terms need to shift, in line with market realities already baked in… even if they haven’t yet permeated the vernacular. But before getting to our prescription, let’s touch on the pathology; how did seed get where it is today?

The Origins of Modern Seed

Round sizes — and hence round names — are ultimately set by VCs, who allocate based on deal flow and AUM. Investment amounts are informed by the same fundamental factors behind all investor decisions: fear and greed. Both are manifesting in new ways that have steadily warped the seed market since 2021.

On the fear side: there’s too much capital in certain bands of early-stage VC. Multi-$100M+ “seed” funds have too much AUM to do $1–2M pre-seeds, but rarely have the brand to compete with platform funds for true Series As. They’re squeezed—so they take the deals they’re good at and expand them. At the same time, AI has inflated what “great” looks like: per Bessemer’s State of AI 2025 report, a “Shooting Star” must eclipse $100M in ARR in 4 years. In that environment, some investors have chosen to gravitate earlier: avoiding scrutiny against rising milestones by backing pre-revenue companies that could be 10x growers rather than ones already demonstrating a solid 3x. Especially as AI has driven a wave of capital efficiency — in ability to grow on fewer dollars and achieve profitably, if not in overall dollars raised — that have the potential to diminish reliance on mid-early-stage funders. This raises a tentative fear of a rise in inception-to-Series-A stories that could make traditional seed even less valuable.

On the greed side: mega funds are absurdly large—so large that returns targets traditionally associated with early-stage venture capital are hard to imagine at their AUM. But they still have the brand to convince founders they’re valuable partners at any stage. That said, the VC brand league tables are ever-shifting. We wrote about this in The Seed-Stage Reckoning and The Mind-Virus of Big Venture. While it seems like the same names have been dominant forever, that’s simply not true outside of a handful — it just especially seems that way as capital has concentrated into fewer, larger funds, following the 2022 downturn. Historically, it’s not uncommon for these perception shifts to occur as a result of drastic changes in AUM that move incentives, competencies, and (eventually) brand association out the stages at which that firm originally built its success.

The combined effect: round sizes have inflated across the board, and the relationship between capital raised and company stage has broken down. A $3M raise and a $30M raise can both describe pre-product companies with zero revenue. The amount of capital has become a significantly less reliable proxy for stage, traction, or quality.

This is the backdrop for our central argument: what VC calls “seed” is no longer a coherent stage. It’s a catch-all for everything from formation to Series A. We need a new perspective — most especially at the earliest stages, where institutional capital has only begun to play.

The Case for a Stage Shift

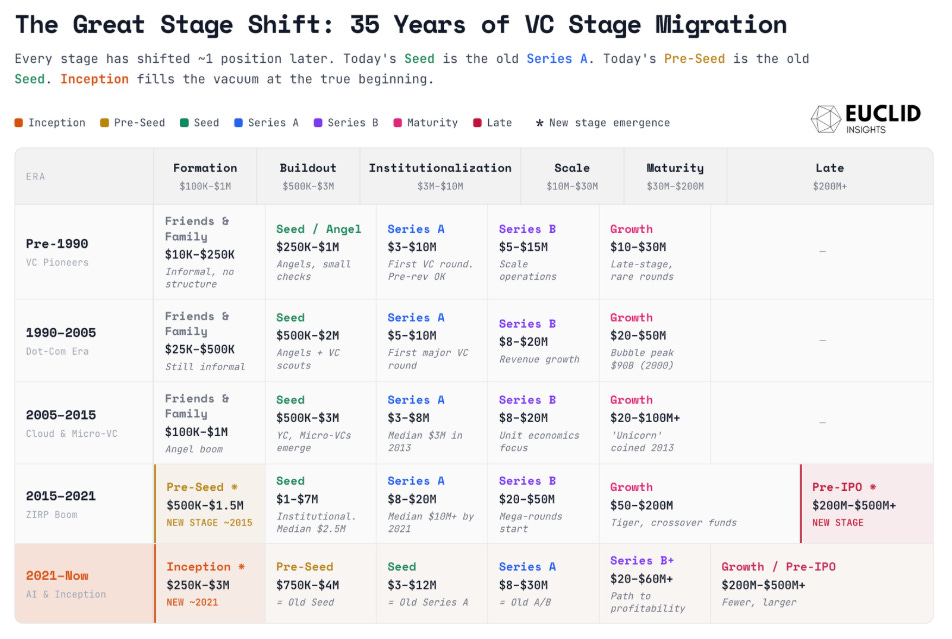

Periodic shifts in stage nomenclature are nothing new in the startup and venture capital ecosystem. Implicitly, they are happening continuously — explicitly, consensus seems to update every 3-10 years.

Before 1990, the landscape was simpler: friends-and-family money gave way to seed (more often “angel” rounds then), followed by Series A, B, and growth. Once coined, “Seed” meant what it sounded like—a small check to get started. From 1990 to 2005, through the dot-com boom and bust, the basic architecture held, but the scale of growth-stage capital ballooned. The bubble peaked at ~$90B deployed in 2000, a figure that wouldn’t be matched for two decades.

The first real structural shift came in 2005–2015, when Y Combinator, micro-VCs, and the SAFE note collectively redefined what “first round” investing looked like. Seed became institutional. It moved from angel territory — individuals writing $25–100K checks on a handshake — to a category with dedicated funds, standard terms, and follow-on expectations. Aileen Lee coined the term “unicorn” in 2013, and the implicit benchmark for what a seed company should become began to rise.

By 2015–2021, the ecosystem responded with two new stages. Pre-seed emerged around 2015 to describe $500K–$1.5M rounds for the earliest companies — the stage that seed used to occupy before it moved up. At the other end, pre-IPO rounds appeared as historically non-VC entrants moved in and companies stayed private longer, creating unique class of big-check capital that has since shifted to fewer, bigger, mostly foundational AI companies. Every existing stage shifted roughly one position later: what had been seed-stage companies were now raising Series As. What had been Series A companies were raising Bs.

This brings us to the present. Since 2021, the same rightward drift has continued—and accelerated. Today’s seed ($3–12M, institutional, often requiring traction) is functionally the old Series A. Today’s pre-seed ($750K-$4M, increasingly institutionalized) is the old seed. And that leaves a vacuum at the very beginning: the true formation stage, where a founder has conviction and a thesis but minimal product, minimal if any non-founding team, and little-to-no traction beyond design partnerships.

The stage for which the seed was invented no longer has a name.

Enter Inception

Inception is not a rebranding exercise. It describes something structurally new: for the first time, institutional funds—not accelerators, not angels, not friends and family—are providing genuine 1-on-1 partnership at true formation stages. Inception investing typically contemplates a $500K–$3M check, written pre-traction, pre-product, often pre-deck, and sometimes before a team is fully assembled. The investor’s value at this stage must go beyond the check: it’s operational co-building during the months when the company’s direction is still being set, iterating at high velocity, and arming the business with high-quality resources and guidance.

This stage is distinct from what pre-seed has become over the last decade. Pre-seed was supposed to fill this gap, but it has followed the same path as seed before it: it got institutionalized, bloated, and crowded. The median pre-seed round has roughly doubled since 2020. Funds that call themselves “pre-seed” now write $1–4M+ checks into companies that — often, if not always — have a product and early users. The label drifted from its original meaning, just as the seed did.

Many funds are talking about this vacuum and laying claim to inception. Few are actually dedicated to it, and even fewer are built for it. The gap between rhetoric and reality is revealing. If they’re unwilling to write a check before traction — or their fund model doesn’t support the time, concentration, and hands-on engagement that true formation-stage investing demands — they aren’t inception investors, at least as we see it. It’s also important to distinguish that, while accelerators nor incubators do check the box in terms of stage appetite, what we are talking about here is a net-new stage of institutional venture capital: the desire to build an active GP-founder relationship, bringing what once was only available to startups reaching Series A to true formation.

We believe an inception fund fundamentally differs from a pre-seed or seed fund. Deal sourcing requires novel origination. The portfolio must be concentrated enough to allow high-levels of support post-investment. The GP’s time per company is measured in days per month, not hours per quarter. The failure modes we often see at this stage are over-funding a company, which cascades into overspending by the startup before it is ready for scale. Another is writing a check and disappearing. This is the stage where VC-founder alignment matters most, because the investor’s behavior in the first six months shapes the company’s trajectory more than any follow-on round will.

Inception is the frontier of innovation in the venture capital industry — and to do it well at an institutional level requires not only the right risk appetite, but differentiated approaches to sourcing, winning, and supporting founders designed for a stage where top-of-funnel is not a deal, but people.

What Founders Should Ask VCs

If “seed” is a useless label and every stage has shifted, the first question for any founder raising capital is more basic than it sounds: where are you, really? Not what round number you’re on, not what your last investor called it, but what stage of company-building are you actually in—and what kind of investor is built for that stage?

Once you’ve identified where you actually are—not where you aspire to be in a year or two—three questions can help you cut through the noise with prospective investors:

1. What does success look like for your fund?

After a VC invests, what does success look like for them on both a fund level and portfolio-company level? A several-$100M seed fund writing $5M checks needs multi-billion-dollar outcomes at double-digit ownership for a single deal to matter. A mega-fund writing early checks needs decacorn outcomes for that first investment to represent more than an option. This is the crux of what we explored in The Quiet Death of VC-Founder Alignment—fund economics shape investor behavior far more than any outward positioning will reveal.

2. What would the ideal next step for us be?

For our company, what do you think an optimal next round would look like? What are some examples of that step for companies in your portfolio? How many companies in their last fund achieved that, and what did the typical trajectory look like along the way? Of course, if 70% of a S1 portfolio doesn’t make it to S2, that’s a meaningful signal about the kind of bets they’re making and their ability to help support their success. If they start talking about leading your Series As, that should raise a flag (what if they don’t?); if they expect you to skip straight to Series A, raising $20M+ or bust next, what does that mean for your optionality? A VC’s answer will speak volumes.

3. Are you valuable for my stage, or the next?

Every fund is optimized for a specific phase of company-building, and its value is typically sharpest in that phase. A fund set up to accelerate companies with a few million in revenue will excel at scaling out teams, optimizing go-to-market, and prepping for the maturity required of a business looking to launch into it’s scale-out phase. That's genuinely useful—if you're at that stage. But if you're a month out from formation, you need something entirely different: help iterating on the idea itself, perhaps making a founding engineering hire, warm introductions to seed (and potentially Series A GPs) for the next round, and bringing on your first advisors. Moreover, signal matters. And yes, usually that means brand and network. But consider that a big brand on your cap table at inception, that doesn’t participate in the next round, is a glaring red flag.

Make sure the investor you're choosing is valuable for where you are — and has the fund model to deliver that value — whether it’s tactical, tangible, or signal-based. You will, in all likelihood, bring further investors onto your cap table down the road: take care to partner with funds when and where they are most impactful.

Inception is the Frontier of VC Innovation

In just the last two decades, total VC AUM has expanded by an order of magnitude. The naming conventions we’re clinging to—pre-seed, seed, A, B—are artifacts of a time when the entire US VC industry deployed less in a year than a single mega-fund now manages. Every decade, the ecosystem has added a stage to account for what the previous terms no longer describe. We’re at that inflection point again.

Our case for inception isn’t simply about a label; it’s an argument about what the earliest stage of venture investing should look like. Not accelerators running cohorts of 200. Not angels writing checks on a napkin. Not pre-seed funds & seed funds masquerading as the same “product.” Inception is an institutional commitment to 1-on-1 partnership at the moment a company is being born—when the investor’s judgment, time, and operational engagement matter more than their capital.

With the exception of small partnerships that truly operate as a unit (rare above a few hundred million AUM) and programmatic funds like YC, VC is more of an individual sport than most realize. The GP on your board, answering your calls, by your side for a decade — that’s what matters. As we argued in Software Is Dead—Long Live Software, AI is reshaping not just which companies get funded but the entire business model landscape VCs invest in. The firms that adapt — by building their funds for the inception stage, not just talking about it — will earn the right to partner with the next generation of breakout founders from day zero.

Round names won’t ossify, nor ever be perfect. The age of Inception has just begun and deserves its own distinct consideration as a stage — but will eventually evolve too. Certainly, the capital efficiency enabled by modern AI is changing definitions faster than anyone can write. One piece of advice, however, is timeless: founders and allocators who continually interrogate the strategies and incentives beneath the nomenclature and find the right match for their goals will navigate this market with far more clarity than those who think one size still fits all.

Thanks for reading Euclid Insights! Additional sources here.1

Euclid is an inception-stage VC built for Vertical AI founders. If anyone in your network is working on a new startup in this space, we’d love to help. Just drop us a line via DM or in the comments below.

Carta (2025). State of Pre-Seed: 2025 in Review, State of Seed: Winter 2025, State of Private Markets Q3 2025. Carta.

Crunchbase (2025). Seed Funding In 2025 Broke Records Around Big Rounds And AI; A Growing Share of Seed and Series A Funding Is Going to Giant Rounds. Crunchbase.

PitchBook (2025). Startup Investor Ranks Have Fallen Another 25%; Active VC Firms Shrink Amid Zombie Fund Rise. PitchBook.

Institutional Investor (2025). Seed Funding Isn’t Small Anymore: AI Start-Ups Push Rounds to Historic Highs. II.com.